Setting the Stage for Stability and Progress in Southeast Europe*

|

|

|

- Martha Wilkerson

- 5 years ago

- Views:

Transcription

1 CENTRE FOR ECONOMIC REFORM AND TRANSFORMATION School of Management and Languages, Heriot-Watt University, Edinburgh, EH14 4AS Tel: /3485 Fax: World-Wide Web: Setting the Stage for Stability and Progress in Southeast Europe* by Paul G. Hare Revised November 2003 Discussion Paper 2003/04 * This paper was written for the Kreditanstalt für Wiederaufbau (KfW) Southeast Europe Financial Sector Symposium that took place in Berlin, November 13 th - 14 th Contact Information Director of Research School of Management and Languages Heriot-Watt University Riccarton Edinburgh EH14 4AS Tel: +44(0) p.g.hare@hw.ac.uk

2 2003 KfW Southeast Europe Financial Sector Development Symposium Berlin, November 13-14, 2003 Session I. Setting the Stage for Stability and Progress in Southeast Europe (Professor Paul Hare, Heriot-Watt University, Edinburgh) Abstract: Politically, the eight Southeast European countries have been less stable than those countries in Central Europe and the Baltics which are on track for EU Accession in The former countries have achieved generally poorer economic performance since 1990, and their economic reforms have also progressed more slowly. With this background, this paper notes that economic development is fundamentally about raising living standards, and that this most often occurs through job creation, accompanied by social policy measures to alleviate the most extreme poverty. In the longer term, of course, investment - both in basic infrastructure and in directly productive assets (buildings, equipment and the like) - is vital for sustained growth. Since investment is often supported by a sound financial system, we also discuss the region s nascent banking systems and financial markets. All countries belonging to the SEE region have to be considered small, open economies. Their future prosperity will be found through integration with the wider world economy, including especially their immediate neighbours and the EU. Hence the trading environment in which the SEE countries operate is a critical feature of their economic progress - with both political and economic dimensions. We also refer to other international flows such as aid and FDI, sketching the factors likely to influence these. Why have reforms in the SEE region not proceeded faster than they have, and what constraints does the reform process face? These are very difficult questions, but I shall attempt to pinpoint the most important constraints, before concluding the paper by outlining possible ways forward. The last part also highlights a few issues of a more general nature that currently impede the region s economic progress, focusing on: investment and growth, trade, micro-level institutional reforms, and financial market development. JEL Classification: O52, P31 Keywords: Southeast Europe, transition, financial markets, economic growth, institutional reforms 2

3 Session I. Setting the Stage for Stability and Progress in Southeast Europe (Professor Paul Hare, Heriot-Watt University, Edinburgh) Five Propositions This paper reviews political developments, economic reforms and the requirements for longer term economic success in South Eastern Europe in order to support the following propositions about the region: P1. Recent weak economic performance is partly the result of political conflict and the subsequent fragmentation of the region into small states with poor inter-regional links; and partly a consequence of subsequent slow or badly designed economic reforms; P2. Sustained growth in the region requires substantial increases in investment both from domestic sources and via FDI, considerable job creation including through a massive scale of SME formation, as well as highly open trade; P3. To achieve the conditions for such growth to occur, wide-ranging institutional reforms will be needed, including very important reforms in banking systems and the financial sectors of each country. A badly designed or poorly functioning banking sector can seriously impede growth, while a well designed one can make a valuable contribution in some cases. P4. Small, poor countries that are not on track to join the EU within a reasonable time period cannot be advised to adopt the acquis communautaire wholesale. The acquis is a complex and costly economic mechanism, better suited to more prosperous states such as most of those transition economics expecting to accede to the EU in May Hence the SEE countries should only be encouraged to adopt those parts of the acquis that are likely to prove helpful at their present stage of development. P5. An important condition for economic success across the SEE region will be the willingness of the countries concerned to undertake cooperative and coordinated economic policies in many key areas. Up to the present, such willingness has been disappointingly limited, despite the establishment of many groups seeking to promote cooperation in many important areas. 1. Introduction Southeast Europe (SEE) means different things to different organisations and in various contexts 1, so it is necessary to start with a definition. For the present paper, accordingly, Southeast Europe refers to the following list of states: Albania, Bulgaria, Romania; from the former Yugoslavia: Bosnia and Herzegovina, Croatia, the former Yugoslav Republic of Macedonia (often referred to as FYR Macedonia, or FYROM), and the federation of Serbia and Montenegro; and Moldova. These states have experienced extremely diverse histories since the fall of communism, including the most severe ethnic conflict seen in Europe since the second world war, various degrees of economic collapse and recovery, and rather mixed fortunes in terms of building stable and effective states. Given this background, the international 3

4 community, together with these eight countries, has established a Stability Pact to foster a longterm conflict prevention strategy in the region 2. For brevity, the background political conditions in the region are summarised in Table 1. Table 2 presents a summary set of recent macroeconomic statistics for each country. [Tables 1 and 2 about here] Though currently growing rather faster than the CEB countries (Central Europe and the Baltics) expecting to join the EU in May 2004, the political strife and economic policy failures of the 1990s are clearly visible in the column of Table 2 showing real GDP in 2002 as a percentage of that in To a significant extent, current high growth might simply reflect recovery from the initial post-communist economic collapse (and subsequent crises). It is debatable how sustainable it is unless accompanied by large increases in new investment. There is evidently much catching up to be done, with the exception of Albania which bounced back very rapidly from its mid-1990s economic and political crisis. On most of the other economic indicators shown in Table 2, other than the general government balance, the SEE countries are generally in a far less favourable position than the CEB countries. It is important to bear these very significant differences in performance in mind in the subsequent discussion. Fundamental to any attempt to achieve sustainable growth is the achievement and maintenance of macroeconomic stabilisation. This means, above all, getting inflation down to manageable, and fairly stable levels; keeping the external accounts in good shape, using whatever exchange rate policy is judged most appropriate, and keeping firm control over the government s own spending and revenue plans. The 1990s witnessed some very bad mistakes in these policy areas in some countries, with some painful lessons being learnt. However, a detailed account is well beyond the limited scope of this paper, so suffice to say that for the most part, the SEE countries have by now established the conditions for macroeconomic stabilisation. They have done so much more slowly than the CEB countries, partly due to the pressures brought about by armed conflict, partly due to the power of economic/political ideologies that prevented political leaders from understanding fully the links between their decisions and the macroeconomic disasters that followed. Likewise, it is evident from the selected transition indicators shown in Table 3 that there is at present a qualitative difference between the reform progress achieved by the eight Accession States (CEB) as compared to that of the SEE countries. In some respects, including its progress with banking reforms, Croatia is closer to the CEB countries; also, Bulgaria has made notable progress with large-scale privatization in recent years. In most other respects, though, the SEE region has a lot of ground to recover. Moreover, these differences in reform progress, according to a great deal of empirical evidence assembled during the 1990s and more recently (see Hare, 2001), translate into marked differences in economic performance. Liberal trade and well protected property rights are systematically linked with stronger economic growth in many countries. For the SEE region, institutional reforms to strengthen the business environment will both encourage more new firm start-ups in the official economy (rather than in the informal or black economy) and create the conditions necessary to encourage far more foreign direct investment. More favourable international trading conditions would support both these aspects of development. 4

5 [Table 3 about here] The remainder of this paper is structured as follows. Section 2 starts from the position that economic development is fundamentally about raising living standards, and that this most often occurs through job creation, accompanied by social policy measures to alleviate the most extreme poverty. SEE progress in these respects, as compared to the CEB countries, is summarised. In the longer term, of course, investment - both in basic infrastructure and in directly productive assets (buildings, equipment and the like) - is vital for sustained growth, as we discuss in Section 3. The same section also sketches the region s nascent banking systems and financial markets, in part as a lead in to later sessions of the Symposium, in part due to their potential role in facilitating efficient investment and trade. All countries belonging to the SEE region have to be considered small, open economies. Their future prosperity will be found through integration with the wider world economy, including especially their immediate neighbours and the EU. Hence the trading environment in which the SEE countries operate is a critical feature of their economic progress - with both political and economic dimensions - and it forms the core of Section 4. In the same section, it is also useful to refer to other international flows such as aid and FDI, sketching the factors likely to influence these. Why have reforms in the SEE region not proceeded faster than they have, and what constraints does the reform process face? These are very difficult questions, but in Section 5 I shall attempt to pinpoint the most important constraints, before concluding in Section 6 by outlining possible ways forward. Section 6 also highlights a few issues of a more general nature that currently impede the region s economic progress. 2. Labour Markets and Poverty Alleviation In most countries, including those in the SEE region, creating jobs is the most effective way of reducing poverty and improving general living standards. But the dislocation and disruption of the old economic structures that relied on regional markets, together with further shifts in economic structures during the 1990s, have resulted in very high rates of unemployment in the SEE region, as shown in Table 4. While the more successful CEB countries already have unemployment rates below 10% of the labour force, with these rates in any case generally falling, countries such as Poland (large share of agriculture in total employment, undergoing restructuring) have unemployment rates closer to 20% of the labour force, as does Slovakia. Hence from Table 4 the SEE countries that really stand out in terms of unemployment are Bosnia and Herzegovina, FYR Macedonia, and Serbia and Montenegro. The relatively good unemployment rates for Albania and Moldova mask a great deal of underemployment and poverty in these countries still largely unreformed agricultural sectors. [Table 4 about here] Most of the CEB countries have economic structures with higher shares of industry than the average across the SEE region, and lower shares of agriculture, as one would expect for a set of economies on average significantly more developed than the SEE countries (again, Croatia doesn t quite fit the SEE pattern in this regard). 5

6 What this structural difference means, though, is that getting unemployment rates substantially down in the SEE region will be even more challenging than it has proved to be in the more developed CEB countries. For enough jobs will be needed not only to employ those currently unemployed, but also to provide alternative income streams for those likely to move out of agriculture as it restructures (in several SEE countries, existing farming patterns cannot support higher incomes without restructuring), and to provide jobs for those displaced from existing medium and large scale industry as it, too, is finally privatised and restructured. In this context, it is no surprise to find that migration to seek work, including substantial international migration, has proved an attractive option to many workers in some SEE countries. Many people have also opted to move in preference to remaining in countries that were recently conflict zones, and where inter-ethnic conflict remains an everyday experience despite the efforts of the international community to promote harmony and peaceful reconstruction. The counterpart to such migration, of course, has been massive flows of remittances back to a few SEE countries, notably Albania and to some extent the successor states of the former Yugoslavia; more modest flows have benefited Bulgaria, Romania and Moldova. Most remittance flows appear to contribute towards household consumption - in other words maintaining or improving current living standards - rather than investment. While migration thus provides a useful alternative route to employment and raises incomes back home through the resulting remittances, there is a downside. Except under the most extreme political conditions, when entire populations are forcibly shifted from one area to another (as after a war, when country boundaries are changed), migration is essentially voluntary, and it is widely perceived as a high-risk and probably costly option for those who move. This helps to explain its selective character, with most migrants being relatively young, predominantly male, and often better educated than those who stay behind. In some cases, populations can lose so many of those with energy, initiative and drive that fostering economic development in the home country faces considerable difficulties. Aside from this voluntary migration, the ethnic conflicts afflicting the region since 1991 have left South Eastern Europe with about 1.7 million internally displaced persons (IDPs, or refugees; see World Bank, 2000), a potent source of possible further conflict. While steps are being taken to make it safe for people to return to their former homes, and many thousands of people have done so in the last few years, many cannot do so and are faced with the prospect of building new lives in new places, usually with little or no compensation to help them. In such circumstances it is only to be expected that feelings still run high, and that cooperation across the new, harder ethnic boundaries should prove so difficult to achieve. Under conditions where both agriculture and the existing industry (mostly still in relatively large firms, often not yet privatised, and only just starting to restructure) are shedding jobs, boosting employment depends on achieving rapid rates of new firm formation. This can take place in two ways: new large and medium businesses formed as a result of FDI (see next two sections); SME development: new small and medium businesses started up, mostly using domestic capital or lines of credit set up by development banks and the like 6

7 (though there remain serious constraints on this process, ranging from the inexperience of the banks in assessing borrowers, to problems of finding acceptable collateral). Since FDI is discussed later in the paper, here we focus on SME development. Without exception, all SEE countries claim that they offer a favourable business environment, supportive to SMEs. Evidence from the Business Environment and Enterprise Performance Surveys (BEEPS), carried out jointly by the World Bank and EBRD in 1999 and 2002, shows solid improvement in the business climate across the SEE countries, with marked catching up on the CEB countries (which also improved but at a slower rate). Since the BEEPS surveys look at the business environment in a broad, multi-dimensional way (covering macroeconomic management, taxation, business regulation, corruption, crime, the judiciary, finance and infrastructure), this is very encouraging news. However, what is really critical, of course, is how quickly such improvements will translate into faster rates of business formation, and how quickly the SEE area will continue to improve the conditions for doing business. Interestingly, IMF (2003d, pp.5-6) indicates that at least in FYR Macedonia, business turnover in recent years has been healthily high: about 60% of the firms that existed in 1994 had ceased trading by 2000, while two-thirds of the firms operating in 2000 did not exist in While new businesses are being established, it is naturally important to have in place suitable social policies to alleviate poverty in the meantime. In any case, regardless of job creation efforts, some form of income support is needed for those parts of the population not economically active, such as the retired, those unable to work (e.g. due to disability), adults undertaking training and education, and so on. The reality, however, is that especially in relatively poor countries there is a delicate trade off between the rates of benefit that can be paid, and the tax rates that must then be levied on business activity in order to finance them. The higher the benefits the higher the resulting tax rates will be, and these in turn translate into slower rates of new business formation, as Blanchard (1998) analysed very neatly. The resulting dilemma can be avoided to some extent either by targeting benefits very strictly to those in direst need (accepting that this can be administratively quite tricky), by paying benefits at extremely low rates, or by taking steps to slow down restructuring, so that fewer new entrants join the labour market. The last of these options is often rather tempting politically, though it can be costly itself (requiring some mix of protection and/or subsidies to keep ailing firms alive, also preserving the very damaging soft budget constraints 3 ), and by limiting competition can also contribute to an already poor business environment by discouraging the entry of new firms. 3. Investment and the Financial Markets To sustain growth, investment rates in most of the SEE area need to be higher than they have been in recent years. While FDI can make an important contribution (as we discuss further in the next section) it has not hitherto done so due to the poor investment environment and unstable political conditions that investors would have faced, together with the small and fragmented markets that characterise the region. In the meantime, much of what capital investment takes place must be funded either by aid donors or, more plausibly, from the usual domestic sources - retained earnings by firms and savings by households. It is commonly claimed that people are too poor to save, and that therefore most investment must be funded from outside. But this is simply wrong except for very short periods. As the economic situation stabilises and improves, enabling people to see clear benefits from saving in terms of the real returns they can achieve, 7

8 they will indeed start to save more. Part of the process of making savings more effective is the development of financial institutions such as banks and non-bank financial intermediaries both to mobilise savings and to ensure that they are allocated where they can be used most productively. Table 5 starts this discussion by reviewing savings and investment in the SEE countries, and then comparing these with the comparable situation in CEB countries. The comparison makes clear that in the CEB countries, with the exceptions of Poland and to a lesser extent, Lithuania, investment ratios are high (generally over 25% of GDP), and domestic savings ratios are also high, mostly above 20% of GDP (again, with the same two exceptions). This means that relatively small fractions of the needed savings are typically contributed from abroad, leaving one fairly confident that the observed growth is likely to prove sustainable. [Table 5 about here] The situation is not yet so satisfactory among the SEE countries, with the exception of Croatia. Investment rates are mostly below those in the CEB countries, domestic savings rates are a lot lower, with the result that these countries rely heavily on foreign savings, mostly in the form of remittances and foreign aid rather than FDI. Much aid in recent years has been directed towards the post-conflict restoration of physical infrastructure, and when this inflow declines, aggregate investment could well fall considerably in some of the SEE countries. To improve longer term growth prospects, and the sustainability of their respective development paths, domestic savings ratios need to rise and the resulting investment must then be allocated efficiently. One normally expects the banks and financial markets to play a significant part in achieving such goals. There is a good deal of evidence from around the world, as noted by Mehl and Winkler (2004), of a long-term causal link running from financial development to economic growth. However, the SEE countries, at least until very recently, had weak and fragile banks operating in a poor institutional environment, hence there was more reason to expect the banks to impede growth rather than to assist it. Some policies to help change this situation are suggested later. I would not necessarily expect faster economic growth to follow hard on the heels of strengthened financial sectors in this region; and in the more successful transition economies on track to join the EU next year (2004), there is no noticeable correlation between their observed performance and the diverse paths of financial sector development they each chose to follow. As Berglof and Bolton (2002) point out, the financial sector has contributed rather little to the industrial restructuring that has occurred even in the more successful countries, and they argue instead that the key to economic success is: the ability of governments of transition countries to enforce contracts and to achieve fiscal and monetary responsibility, together with a commitment to refrain from excessively bailing out failing banks or loss-making enterprises... (p.78). We return to this important observation later in the paper. Meanwhile, to complete this section let me sketch the basic shape of the existing financial structures across the SEE region. The entire region has, of course, progressed beyond the traditional mono-bank system that prevailed under socialism, so two-tier banking is universal, with a central bank overseeing a diverse sector of commercial banks. Several of the countries have stock markets, while most have few or at best very weak non-bank financial institutions such as insurance companies, pension funds and the like. In terms of marketable financial assets, 8

9 government paper is the principal type, mostly very short term. There are a few corporate bonds, and some equity shares (mostly resulting from privatisation operations) traded on local stock markets, but volumes are low and the markets are everywhere quite thin. Thus in practice, financial systems are predominantly bank-based, the more successful ones being those with a significant foreign ownership stake in the banks. In the countries that have not reached this point, significant further restructuring of the banking systems is needed to improve liquidity, deal with accumulated non-performing debt, and so on. Most bank lending is to governments (and to a smaller extent, to households) rather than to firms, the latter funding most of their investment through retained profits and FDI inflows. Outstanding issues for the financial sector include (see also the relevant columns of Table 3): how independent the central bank should be (or what degree of independence would be politically acceptable and credible); who should have responsibility for banking sector regulation (the central bank itself or a separate agency); what model of regulation should be used (e.g. a model based on EU and BIS rules, or something different); how rapidly the banking sector should be privatised and on what model (in particular, what role might be expected for foreign participation); what degree of depositor protection should be offered; and the arrangements that should be in place to deal with bad debt, including the underlying bankruptcy laws. A final issue - often a joint responsibility of the central bank and the relevant ministry of finance - concerns the exchange rate policy and regime that a given country should pursue. These are all difficult and often controversial issues, especially for small countries with little experience of modern commercial banking. Note, however, that none of items in the list referred to other parts of the financial sector, including the stock market, essentially because I do not expect these other markets to assume great importance for most of the SEE countries in the near future. 4. Trade, FDI and Aid Only one of the SEE countries has a population in excess of ten million, namely Romania with over 20 million, all the others being much smaller, mostly with fewer than 5 million inhabitants (Table 2). Such small, low-income countries cannot hope to achieve high living standards unless they adopt strongly export-oriented economic policies and take the fullest possible advantage of the opportunities offered by the international division of labour. This is easier said than done, however, since the region faces some awkward constraints, some of which it could overcome through actions taken within the region, some of which require the cooperation of other countries. The constraints and circumstances that I have in mind are the following: There is a complex network of mostly bilateral free trade agreements across the region (encouraged by the Stability Pact), but what this means in practice is that firms wishing to export to one of the neighbouring countries have to be aware of numerous separate conditions and restrictions, as well as the standards rules and customs procedures of each country, which have not yet been harmonised. It is very important to extend the network of bilateral agreements into a single multi-lateral free trade agreement across the region, with as few exceptions to free trade as possible - but the SEE countries have resisted such a multi-lateral initiative. The EU has Partnership and Cooperation Agreements (PCAs) or Stabilization and Association Agreements with most of the SEE countries. These provide for a good deal 9

10 of very welcome trade liberalisation but also incorporate quotas and other restrictions on so called sensitive sectors, these restrictions being somewhat different for different regional partners. Moreover, the local content rules (rules of origin) in these agreements are often unnecessarily restrictive, as they were until the late 1990s for the first wave of Accession States. As Michalopoulos (2003) points out, these agreement can tend to create a hub and spokes structure under which the hub (i.e. the EU) tends to accrue most of the benefits. The CIS countries notionally form a free trade area that includes Moldova, but in practice this is not an operational reality and Moldova faces great difficulties in exporting through Ukraine and on to Russia where it used to have large markets (e.g. for wine). The other seven SEE countries do not receive special access to CIS markets, though those that join the EU later in the decade will benefit from the PCAs already in place between the EU and Russia, and the EU and Ukraine. Six of the eight SEE countries already belong to the World Trade Organization (WTO), though four of the accessions are very recent (Albania, Sept. 2000; Croatia, Nov. 2000; FYR Macedonia, Apr. 2003; and Moldova, Jul. 2001). Bosnia and Herzegovina, and Serbia and Montenegro have both applied to join the WTO, but their applications are still at an early stage, the relevant Working Parties not having convened yet. Hence the region does not yet enjoy the full benefits and protections of universal WTO membership, such as automatic MFN treatment by other WTO members, and access to the WTO s dispute resolution procedures. The physical infrastructure needed to support trade in the SEE region is patchy at best, with roads, rail links, telecommunications, and the electricity system needing substantial investment. This is an area towards which much of the aid effort in the region is being directed. The institutional infrastructure is also poor, both in terms of government services and private sector provision. As regards the former, I refer to border controls and customs formalities, frequently seriously corrupt and inefficient to an extent that causes both delays in transit of goods, and significant increases in transactions costs (due to bribes). I also refer to the design of tariffs, and other regulations governing trade, all often needlessly complex and therefore virtually impossible to administer effectively (without further corruption). Concerning the private sector, I have in mind the banking services needed to support trade (export credits, and efficient means for effecting international financial transfers, for instance), plus insurance and freight services. Joint public-private services would include export promotion activities like trade fairs, as well as export credit guarantee schemes. These services are weak or non-existent in several of the SEE countries. To help understand the scale of the problem we are referring to here, it is worth presenting some basic statistics on the major trade flows and average tariff rates (not trade weighted) of the SEE countries. This is done in Table 6. [Table 6 about here] 10

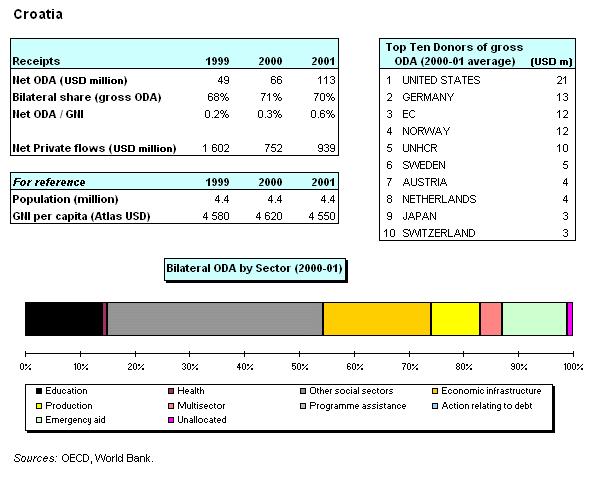

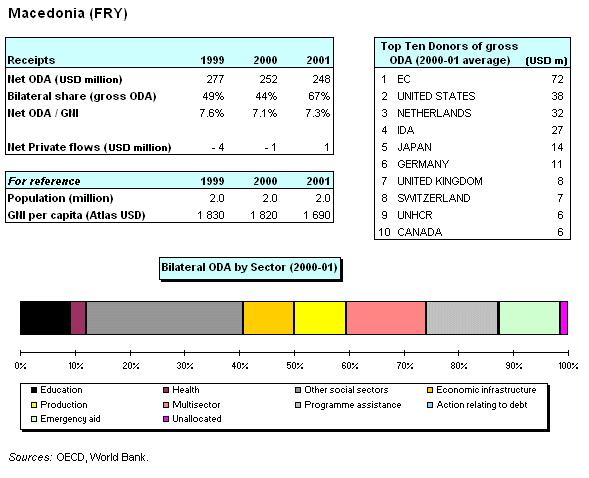

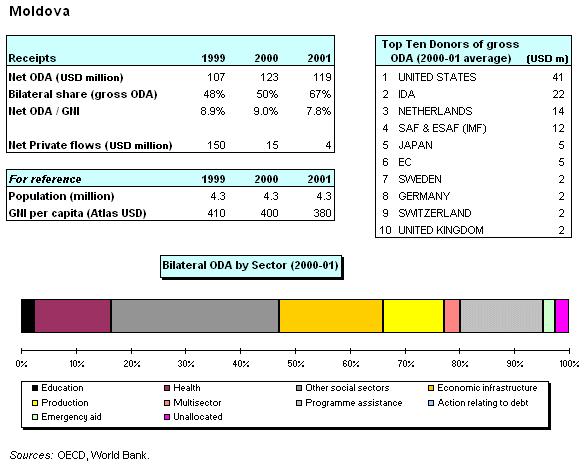

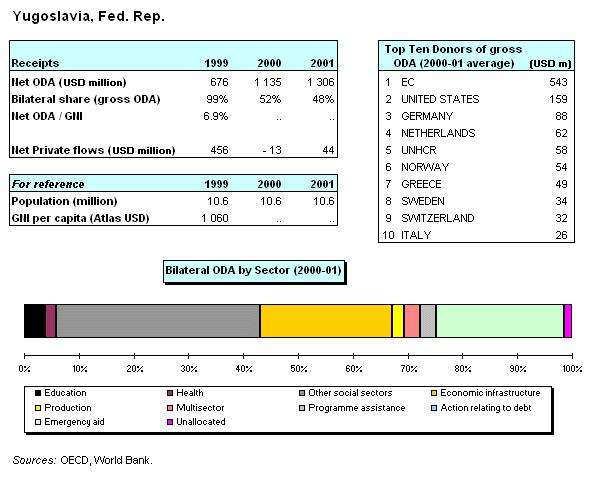

11 What is evident from the table is that for such small, potentially highly open economies, trade volumes in relation to GDP are very much on the low side. They are well below the ratios that can be found in the smaller CEB countries, and especially low as far as exports are concerned (and hence only sustainable on the basis of continuing inflows of external financing). Thus for several of the countries of the SEE region, policy-makers and advisers need to be devising ways of boosting exports not merely by a few per cent here and there, but by factors of three or four at least. This present a serious challenge, of course, but it is vital both for job creation within the countries (and the associated contribution to reducing poverty), and for the promotion of regional economic integration. Average tariff rates are not terribly high for most countries in the region, and the diversity of rates is also not too bad except for Croatia. However, as noted above a free trade zone across the SEE region would certainly contribute to more efficient, and simply to more trade. In addition, numerous non-tariff barriers currently affecting trade also need to be lifted - but more on that tricky issue later. In recent years, the SEE countries have not attracted a great deal of foreign direct investment (FDI) and some of the countries have serious debt problems. Table 7 summarises the situation across the region. [Table 7 about here] It can be seen that cumulative FDI inflows have been low everywhere except Croatia, all the other countries having per capita FDI inflows well under half the levels typical for the CEB countries, and in most instances much smaller than that. The flows in 2002 reveal a somewhat better picture in that, as a percentage of GDP, the flows are not much below the current rates observable in the Accession States. Nevertheless, the sums involved remain low. The low levels of FDI, in my view, partly reflect the slow pace (and sometimes the unsatisfactory forms) of privatisation in the SEE countries, and partly reflect continuing deficiencies in the business environment in each country. Moreover, the small size of most of the countries means that foreign investors will mostly expect to engage in trade in addition to supplying domestic markets, so that one would expect foreign investors to be especially influenced by the regional trading environment. As we have already observed, this is far from being as open and flexible as one would like to see. Last, we turn to aid flows to the SEE countries. For each country, the charts and tables presented under the general heading of Table 8 show net Overseas Development Assistance (ODA) receipts in 1999, 2000 and 2001, both as a total and as a percentage of Gross National Income (GNI); then the top ten donors of ODA; and last the composition of bilateral ODA by broad sector. [Table 8 about here] As regards aid, the SEE countries fall into two groups. First there are Bulgaria, Romania and Croatia, states that are either currently on track for EU entry later this decade or hope soon to join that group; aid flows as a percentage of GNI are low, in all cases below 3% of GNI. For the remaining five countries, aid flows as a percentage of GNI are at least double those of the first group, that is they typically exceed 6% of GNI, and in the case of Bosnia and Herzegovina they 11

12 exceeded 12% of GNI for all three years reported in the table. For all the countries, Germany was among the top ten donors and for several (Romania, Bosnia and Herzegovina, Croatia, Serbia and Montenegro) it was in second or third position. Most of the larger aid flows can be explained as post-conflict reconstruction and recovery aid, in which case one can expect the flows to be declining before long. In any case, some of the aid literature draws attention to issues of absorptive capacity and aid dependence when flows remain large for long. This factor, too, might lead to an expectation of declines in aid flows to the region fairly soon. Consequently, governments in the region need to approach aid from two points of view: (a) how to make best use of the aid flows that are in place; and (b) how to adapt their economies so that they can manage with less aid in the future. These are both difficult challenges Constraints on Reforms: Internal and External Conditions Summing up key points from the foregoing discussion, to achieve sustainable economic growth at reasonable rates (say at least 4% per annum, ideally in the range 5-7% per annum), the countries of South Eastern Europe need: (a) more investment, especially financed from domestic sources; (b) a much improved business environment to encourage both new business formation and FDI; (c) a more liberal trading environment including substantial measures towards regional cooperation (both with each other and with major partners such as the EU); (d) further reforms in and consolidation of financial systems, notably the banks in each country; and (e) commitment to the whole range of institutional reforms associated with the transition process, including most importantly the effective implementation of new laws and practices. It is, of course, all too easy to put forward a list such as this. More useful, I think, is to identify the constraints that stand in the way of their immediate adoption throughout the region, since that is a crucial precondition for understanding why progress has not hitherto been faster than it has, and for formulating new policies to promote faster development in the future. We also attempt to make clear the respects in which these conditions facing the SEE countries differ from those faced by the more developed CEB countries. Accordingly, let us now list what appear to be the more severe of the constraints facing the SEE region, distinguishing between internal and external conditions. Internal Conditions I1. Continuing ethnic and religious divisions, suspicion and mistrust, and the associated political instability. I2. Political fears slowed down many reforms, especially those that might have generated high unemployment through the closure of the larger, loss-making state-owned enterprises. Privatisation was delayed, as was a great deal of enterprise restructuring, including in the banking sector. I3. Lack of understanding among elites of the requirements for a well functioning market economy, especially in terms of the need for a strict separation between state and economy, the importance of macroeconomic stabilisation, the need to promote 12

13 competition, the need for economic rules of the game to apply uniformly to all rather than be subject to negotiation, lobbying, bargaining, corrupt deals and the like. External Conditions E1. Links with neighbours in the SEE region - regional cooperation. E2. Links with the EU - trade and investment, and the impact of EU enlargement. E3. Links with other trading partners, such as countries belonging to the CIS. E4. Links with the EU - whether to adopt the acquis. E5. The role of the international community In my view, condition I1 remains overwhelmingly the most important for several of our countries - no longer for Croatia, since that country must now be judged on track for EU entry before too long and appears politically stable, but certainly for Moldova, Serbia and Montenegro, FYR Macedonia, and Bosnia and Herzegovina. All these countries have experienced international conflict, civil war, or at least serious internal disputes between ethnic groups, requiring international intervention by NATO, the EU, the OSCE or the UN. All are still under international supervision (with Kosovo effectively a UN protectorate, Bosnia and Herzegovina having a governmental structure overseen by a High Representative appointed following the Dayton Peace Accords). In contrast, no such international intervention has been called for in any of the Accession States, all of which have proved to be politically stable and increasingly committed to democratic practices (incl., sometimes as result of EU pressure, proper respect for significant minority groups). The reality is that while the international community can sometimes intervene to stop bloody conflict, it cannot compel the erstwhile warring parties to like each other or to cooperate seriously over matters of economic policy and reforms. To this extent, therefore, the role of the international community is necessarily rather limited (condition E5). Ultimately, the groups involved have to want to cooperate before more than token progress is achieved, and while they decline to cooperate, sustained growth and high rates of investment are unlikely to occur. This observation raises the question whether there might be some form of incentive that could be offered to such states to induce cooperation that would in turn benefit the entire region. A natural way forward in this regard might be through demonstration effects, in the sense that the visible economic success of some countries (e.g. Croatia in our present group) might finally encourage elites and governments in less successful states to support reforms in order to emulate their success. A similar sort of demonstration effect could arise if one part of a state, such as Montenegro within Serbia and Montenegro, started to grow rapidly and attract lots of investment; again, that success might then be emulated by the rest of that state. While an appealing idea, however, there is plenty of evidence from around the world to suggest that if this approach works at all, it is extremely slow, often because the brightest and best people choose to move out rather than wait endlessly for promises of political stability to be delivered (e.g. Northern Ireland within the UK - it has been by far the poorest UK region for generations, and is still racked by religious divisions). 13

14 Another type of incentive is that provided by EU membership or the offer of such membership. Within the SEE region, Croatia, Bulgaria and Romania are clearly on track for such membership as noted above. To achieve it, they have to fulfil the general conditions of the Copenhagen criteria, as well as implement the detailed conditions of virtually all chapters of the acquis communautaire. These are demanding conditions, undoubtedly, but they are attractive for countries that want to lock in their reforms and belong to a club of highly developed market economies, especially as the EU is already their major trading partner. For the three countries mentioned, the prospect of EU membership reasonably soon (say, during this decade) provides a very strong incentive to push reforms across the board, and hence create good conditions for growth. For the other five SEE countries, however, all of which are significantly poorer than the first three and much less advanced in terms of market-oriented reforms, the prospect of eventual EU membership are included in most of the formal agreements between the EU and these states, but it must be said that there is no realistic likelihood of entry for at least a decade, and quite possibly for a lot longer than that. Hence EU entry cannot possibly provide much of an incentive to political elites and given that, it is quite surprising to find that PCAs and other agreements linking these states with the EU envisage an increasing harmonisation of regulatory conditions through, among other things, adopting more and more elements of the acquis. But what is the attraction for these states of adopting the acquis? (Condition E4). Personally, I find it very hard to see the attraction, especially as adoption of large chunks of the acquis would be unavoidably complex and costly - for poor, small states, it is far too complex an economic mechanism, beyond their likely implementation capacity. Even worse, I suspect that misguided attempts to implement parts of the mechanism, such as complex tax rules to do with VAT, might open up new opportunities for corruption in states that are already quite fragile. As far as trading links are concerned (Conditions E1, E2, E3) we have seen that the countries of the SEE region has displayed some willingness to conclude bilateral free trade agreements with various partners, but as noted above the diversity of limitations and restrictions in these separate agreements itself constitutes a trade barrier, and there is not yet an adequate multilateral agreement in place. Aside from the evident desirability of a region-wide free trade area (i.e. an area with zero tariffs on most inter-regional trade, and ideally on most trade with major partners like the EU; but not necessarily a common external tariff), however, the main impediment to trade is surely the plethora of non-tariff barriers. These range all the way from efforts by local administrations to protect their firms form competition, through problems over technical standards, restrictions on freight operators, inefficient border controls, to shortcomings in the financial institutions and instruments needed to support trade. All of these problems serve to raise the transactions costs associated with trade; conversely, therefore, one way of thinking about many institutional reforms is to regard them as means of reducing transactions costs. At this level, furthermore, many of the concrete problems might be regarded as largely technical in nature, and hence rather suitable for amelioration through various well focussed aid programmes, though one should not forget that in most instances a good deal of political will is still needed to overcome these problems. Comparison with the CEB countries heading towards EU entry in 2004 demonstrates the effectiveness of an early commitment to reform in terms of promoting industrial restructuring, promoting trade, and sooner or later, attracting foreign direct investment. The latter, of course, 14

15 was also contingent on credible agreements being in place regarding the treatment of accumulated external debt (incl. measures of debt forgiveness and rescheduling where appropriate), a factor that helps to explain the very low levels of FDI flowing into Poland until the mid-1990s. Moreover, far from generating intolerable unemployment, most of the CEB countries found that quick and sometimes tough reforms often paid off by fostering new business formation and faster growth - and quite soon, this started regional unemployment rates on a downward path, despite the initial, wholly understandable fears of many political leaders. The impact of EU enlargement (part of Condition E2) will also prove significant for parts of South Eastern Europe, since the harder frontier that will be established following enlargement in May 2004 will border several of our countries for the first time: Croatia, Serbia and Montenegro, and Romania. Albania, FYR Macedonia and Bulgaria already border Greece, of course. Daily cross border movements of people seeking work could become more difficult in places, and some trade flows might be subject to controls which, though more rules-based and less corrupt than is sometimes the case at present, could restrict some business. It is to be hoped, however, that in implementing its enlargement plans, the EU will strive not to disadvantage the small countries around the EU s South East frontiers. To illustrate the distinction between relatively bold and misguided or weak reforms, a few examples are probably more useful to the reader than a lengthy discussion. We start with some examples of bold policies: Estonia, early 1990s: abolished virtually all tariffs and introduced a currency board system, tying their currency to the DM, now to the Euro. Hungary, : introduced tough bankruptcy law and enforced it. Many outsiders criticised the country for being too tough, but Hungarian firms no longer expect state rescue and many perform very well internationally. Czech and Slovak Republics (or CSFR until end-1992), early 1990s: introduced imaginative model of voucher-based privatisation and, to the surprise of many observers, implemented it successfully. The contrast with some of the SEE countries is highly instructive, as the following examples of a more hesitant or poorly founded approach to reforms illustrate: Romania, 1990s: quick to establish the institutions to promote privatisation, but these were based on a very unsatisfactory model and were in any case poorly implemented, in part due to politicians fears of creating unemployment. Albania, early to mid-1990s. Pyramid financing scheme that attracted most of the population s savings, resulting in a serious financial crisis (the IMF had advised that the scheme was fraudulent and would end in tears, but the government at the time did not wish to take their advice). Bulgaria, mid- to late 1990s: failed to manage the government budget well and ran into a severe foreign exchange crisis. Eventually set up a currency board system to help stabilise the country s finances, with good results. 15

16 Serbia and Montenegro, mid- to late 1990s: unrealistic conceptions of privatisation (incl. the claim that so called socially-owned firms could already be regarded as private) helped to slow down reforms in general. Moldova, late-1990s: still maintained low electricity prices and then failed to enforce them, with non-payers rarely cut off and many payments taking the form of barter. Numerous other examples could be cited, but for space reasons I shall not continue. In any case, I think the flavour of the problem has been highlighted sufficiently clearly. In terms of the earlier lists of constraints, I would include all these examples under the headings of Conditions I2 or I3. To overcome them, therefore, political élites need to be persuaded to be less fearful and more bold in their reform efforts; and there is also an evident requirement for wider education about the nature of a market-type economy and its critical institutional underpinnings. 6. Conclusion: Critical Issues and Next Steps In this concluding section of the paper, I focus on just four issues. My selection has been influenced in part by what I judge to be most important for economic recovery and success in the SEE region, and partly by the theme of this symposium, namely financial sector development. Before proceeding to specific points, it is worth noting that in the past year or two a great deal of valuable material has been published summarising the first years of transition experience, and seeking to draw out practical lessons for the future. Thus Mitra and Stern (2003) review taxation structures in the transition economies 5, Estrin (2002) reports on corporate governance, Djankov and Murrell (2002) examine enterprise restructuring, Campos and Coricelli (2002) review what we know, or still do not know, about growth in transition, and Hare (2001) analysed institutional reforms. These papers provide a backdrop to what follows. In terms of concrete recommendations, the emphasis is very much on simple, practical steps that can yield tangible benefits relatively rapidly. (a) Investment and Growth Investment has been stressed at several points already. It is an area where the performance of the SEE countries (except Croatia) lags well behind that of the CEB region, the Accession States. High levels of domestic investment and a positive business environment strengthen business confidence at home while also encouraging much needed FDI. To encourage investment, financial market reforms will help (see (d), below), as will positive measures to improve the business climate (e.g. Paddy Ashdown s Bulldozer Initiative in Bosnia and Herzegovina, ) such as simplified tax rules, simpler registration requirements, elimination of most licensing obligations, limitations on business inspections (e.g. for alleged health and safety reasons, and numerous others), and so on. There is also a virtuous circle aspect to promoting investment, in that people are usually more willing to save when they perceive that their community is developing and living standards are visibly improving, since savings then feel worthwhile. This point explains why communities and countries sometimes find themselves locked into a low-level equilibrium, with low savings and 16

17 investment, slow growth, and generally negative attitudes - yet once growth starts and people become more confident that it is sustainable, so it proves to be; for the same community, with more positive, optimistic attitudes about the future, can then achieve a high-level equilibrium. The challenge for much of the SEE region concerns how to bring about the shift from a low-level to a high-level equilibrium development path. (b) Trade The easy part of trade policy is securing agreement on such structures as free trade areas and the like, where much progress has already been achieved in our area (though still not enough, as noted above). Much the harder part of making trade policy work well is in the area of the most micro-level regulation of trade. Here are a few ways of improving trade in the SEE region: (i) Look at border crossings by road and rail, as well as the major international waterways such as the Danube River. Carry out surveys to find out how long a typical shipment is held up at border points, other check points, customs offices, etc., and also find out what costs result from these delays, covering the legal tariffs, additional bribes paid to limit delays, etc. While doing this, it would be useful to find out about similar data for Hungary, Estonia, or elsewhere in the CEB countries for comparative purposes. Then once the right data are available, even roughly, set targets at border crossings to limit the time delays and cut the costs associated with normal trade. To be really effective, I would expect such measures to require a fairly high degree of international co-operation, since if Serbian exit controls are quick and cheap, the impact on trade is still pretty bad if the corresponding Bosnian entry controls are slow and expensive, for instance. (ii) Strengthen the financing of trade by offering export credit guarantees and trade-related finance on a more routine basis than currently occurs. Apart from requiring improvements in the region s financial institutions within each country (again, see (d)), there is again an evident need for international co-operation between banks to ensure that international credits are quickly and reliably honoured so that exporters from within the region (it is clearly not good enough if the banks will only deal with internationally known firms) get paid on time. (iii) Stop protecting local firms that supply poor quality products, often at relatively high cost. Politicians often think they are protecting local jobs, but in practice workers often vote with their feet and once they perceive a firm to be in poor shape they will seek jobs elsewhere. Many poorly performing firms in the region have very high rates of voluntary quits. What is often quite astonishing, though, is that despite performing badly they also take on lots of new workers, as a result of the political pressures that enable them to remain in business. This is actually seriously bad economics (and also bad politics except from a very short term standpoint). It limits competition in the domestic market and therefore discourages the entry of new firms that might well be able to perform better once they were established, and it also discourages interregional trade. (c) Micro-level Institutional Reforms Here the main problem is nearly always with effective implementation, since many of the SEE countries have much of the right legislation in place. Sometimes countries have chosen to adopt very complex models to regulate a given type of activity, and then prove unable to carry it through; sometimes the basic approach may be better, but it can still fail as a result of sectoral or regional political pressures to demand special treatment. A serious problem in this region 17

18 when thinking of micro-level policies is the smallness of the countries, and the fact that in many local markets there will be few agents on either side, most whom know each other. Hence the usual assumptions of competitive analysis - that markets are essentially impersonal institutions with no agents receiving special treatment or possessing special information - frequently fail. This makes the design of well functioning market institutions unusually difficult. For lack of space, I give three examples. (i) Electricity pricing. The key here is to ensure that electricity prices are high enough to cover production and distribution costs (incl. an allowance for capital costs when the system operates close to capacity), and that charges to different users reflect differential supply costs. In most developed countries, for example, per unit charges to households are much higher than those to firms, while the opposite has tended to be the case in many transition countries. Even worse, transition countries have frequently proved unwilling/unable to disconnect customers who fail to pay, and have tolerated non-monetary payments (as noted above for Moldova, though it was far from the only offender). While recent years have witnessed significant improvement in these matters, there is a long way to go. Moreover, poor pricing of electricity can distort the pricing of downstream products that use it as a major input, such as aluminium production (such poor pricing can in turn distort privatisation decisions). (ii) Bankruptcy provisions. When firms fail they should exit from the market to make way for new ones. This is a fundamental part of the market economy, and one of the principal mechanisms through which productivity improves and incomes rise. Hence efforts to impede the process are mostly self-defeating in the long run, and this is true both for small and large firms. For banks to function properly, they must have the right to call in loans that do not perform, even if this forces a firm into closing down. One can, of course, argue about exactly how a bankruptcy law should be written, how creditors should be ranked and what conditions must be fulfilled for a firm to cease operation, and there is much academic literature on this topic. For present purposes it is sufficient to insist that suitable legislation should be in place, and that it should be enforced through procedures which are, as far as possible, simple, quick and cheap. (iii) Property and collateral. Similar points apply to the use of immovable property and other assets as collateral, e.g. when a firm or an individual seeks a bank loan to develop a new business venture. Such provisions are ineffective if the bank concerned is prevented from realising the assets offered as collateral in the event of default. For instance, if people cannot be turned out of their houses by the courts, such property cannot be offered as collateral and this can prevent many potentially sound businesses from starting up. Also, if there is no market in agricultural land, such land cannot be offered as collateral. Hence to be effective, collateral requires the associated development of other property markets, such as the housing market, the market for agricultural land, and so on. In several of the SEE countries, these markets barely function properly, so there is scope for substantial assistance programmes to help develop these missing markets. (d) Financial Market Development Although some aspects have already been mentioned above, a few additional points are needed to establish the most urgent priorities. Since our region mostly comprises small, low-income 18

19 countries, it can be expected that where financial markets exist they will mostly be thin, fragile and unstable, with few assets to trade, few significant traders. That is the reality and will likely remain so for some time. Consequently, even where stock markets exist, they cannot possibly assume much importance unless some form of regional confederation or association of markets can be established. For political reasons as well as for a variety of local, technical reasons, such an association does not appear very probable. Hence the financial sector will be largely bank-based, and its effectiveness will depend above all on how well the banks operate, how well they are regulated. Experience in the CEB countries argues in favour of foreign ownership stakes in the banks, since that improves service standards and enhances competition in the sector. It also helps to cut or weaken some of the damaging links between banks and large, failing firms that have contributed to poor bank performance in some other transition economies. It then becomes more realistic to imagine that the new and inexperienced central banks in the region might be able to cope with the demands of banking sector regulation. It is important, also, that banking development and real sector development should move in step with each other, since if the real sector moves ahead, it could end up being held back by deficiencies in the banking sphere; and if the banks develop too fast, they could find that they have deposits but far too few sound borrowers. This balance is hard to get right. Again, experience from the CEB countries strongly suggests that government securities will remain the main traded assets, provided governments manage their finances very prudently. There will be a few corporate bonds, but initially not much else. The banks themselves will mostly lend to government, with lending to the household sector and to companies developing more slowly, and depending, as noted above, on the parallel development of other markets, together with enforced legal provisions to protect lenders. For the business sector, it is especially important that finance to support SMEs be developed further, though this is a field in which the international community has already made useful contributions (see, for instance, several chapters in Matthäus-Meier and von Pischke, 2004). On the other hand, one cannot expect to see the vigorous development of mortgage markets without strong legal title to property, adequate systems of surveying and valuing property for mortgage purposes, and legal provisions that allow lenders to repossess property in case of default. Otherwise the market will be perceived as too risky for lenders to enter. Similar remarks hold for pension funds. These will become more important over time, but at present few firms in the region require pension contributions in addition to existing state-determined payroll taxes, and there are not yet many reasonably secure long-term assets for funds to hold. Overall, as far as the financial sector is concerned, what the SEE region needs is a network of well run banks, preferably with significant foreign ownership stakes, able to finance the governments of the region as well as the region s trade and SMEs. That would indeed be a useful start. 19

20 Endnotes 1. For the EU, Southeastern Europe (SEE) consists of Albania, Bosnia and Herzegovina, Croatia, FYR Macedonia, Serbia and Montenegro. Bulgaria and Romania are not included as they are regarded as accession states, even though their entry to the EU is not expected before For the EBRD, SEE commonly excludes Croatia from this list but includes Bulgaria and Romania. However, in the context of discussions relating to the 1999 Stability Pact (and subsequent developments), SEE is defined as the eight Stability Pact countries, namely: Albania, Bulgaria, Romania, Bosnia and Herzegovina, Croatia, FYR Macedonia, Serbia and Montenegro, and Moldova. This is the definition adopted in this paper. 2. For fuller information about the Stability Pact and its activities, see the Pact website at the address: 3. The soft budget constraint (SBC) notion was first introduced by Kornai; see, for instance, Kornai (1980), Kornai (1992), and for a more recent theoretical exploration of various interpretations of the SBC, Kornai et al. (2002). What it refers to is the idea that firms in financial distress might be permitted to set artificially high prices, defer tax and social security payments (or not make them at all), defer payments to suppliers, fail to meet credit repayment obligations, and so on. In an environment of hard budget constraints, firms can only engage in these practices within quite strict limits. 4. Some interesting analysis and discussion of the political economy of aid, and practical experience with aid programmes, can be found in Easterly (2002) and Martens et al. (2002). We do not pursue these discussions in the present paper, for space reasons. 5. Although beyond the scope of this paper, Mitra and Stern argue that transition countries should aim for tax revenue to GDP ratios in the range 22-31% (depending on their level of development), comprising VAT (6-7%), excises (2-3%), income tax (6-9%), social security/payroll taxes (6-10%), other taxes, e.g. on trade and property (2%). All percentages here are percentages of GDP, not proposed tax rates, of course. 20

21 References Berglof, Erik and Bolton, Patrick (2002), The Great Divide and Beyond: Financial Architecture in Transition, Journal of Economic Perspectives, vol.16(1), pp Blanchard, Olivier (1998), The Economics of Post-Communist Transition, Clarendon Lectures, Oxford: Oxford University Press Campos, Nauro F. and Coricelli, Fabrizio (2002), Growth in Transition: What We Know, What We Don t and What We Should, Journal of Economic Literature, vol.xl(3), pp Djankov, Simeon and Murrell, Peter (2002), Enterprise Restructuring in Transition: A Quantitative Survey, Journal of Economic Literature, vol.xl(3), pp Easterly, William (2002), The Elusive Quest for Growth, Cambridge, Mass.: MIT Press EBRD (various years), Transition Report and Transition Report Update, London: EBRD Hare, Paul G. (2001), Institutional Change and Economic Performance in the Transition Economies, chapter 3 (pp.77-99) in Economic Survey of Europe, 2001(2), Geneva: UN Economic Commission for Europe IMF (2003a), Albania: Second Review under the Three-Year Arrangement under the Poverty Reduction and Growth Facility - Staff Report, IMF Country Report 03/218, Washington, DC: IMF, July IMF (2003b), Bosnia and Herzegovina: Second and Third Reviews under the Stand-By Arrangement - Staff Report, IMF Country Report 03/204, Washington, DC: IMF, July IMF (2003c), Croatia: Request for Stand-By Arrangement - Staff Report, IMF Country Report 03/27, Washington, DC: IMF, February IMF (2003d), Former Yugoslav Republic of Macedonia: Selected Issues and Statistical Appendix, IMF Country Report 03/136, Washington, DC: IMF, May IMF (2003e), Bulgaria: Third Review under the Stand-By Arrangement and Request for Waiver of Performance Criteria - Staff Report, IMF Country Report 03/206, Washington, DC: IMF, July IMF (2003f), Romania: Third Review under the Stand-By Arrangement and Request for Waiver of Performance Criteria - Staff Report, IMF Country Report 03/123, Washington, DC: IMF, May IMF (2003g), Serbia and Montenegro: First Review under the Arrangement - Staff Report, IMF Country Report 03/151, Washington, DC: IMF, June 21

22 IMF (2003h), Republic of Slovenia: 2003 Article IV Consultation - Staff Report, IMF Country Report 03/108, Washington, DC: IMF, April IMF (2003i), Slovak Republic: 2003 Article IV Consultation - Staff Report, IMF Country Report 03/234, Washington, DC: IMF, August IMF (2003j), Republic of Poland: 2003 Article IV Consultation - Staff Report, IMF Country Reports 03/187, Washington, DC: IMF, June IMF (2003k), Hungary: 2003 Article IV Consultation - Staff Report, IMF Country Report 03/124, Washington, DC: May IMF (2003l), Republic of Lithuania: Third Review under the Stand-By Arrangement - Staff Report, IMF Country Report 03/55, Washington, DC: IMF, March IMF (2003m), Republic of Latvia: 2003 Article IV Consultation - Staff Report, IMF Country Report 03/113, Washington, DC: IMF, April IMF (2002a), Republic of Moldova: 2002 Article IV Consultation, First Review Under the Three-Year Arrangement Under the Poverty Reduction and Growth Facility and Request for Waiver of Performance Criteria--Staff Report, IMF Country Report 02/190, Washington, DC: IMF, August IMF (2002b), Republic of Estonia: 2002 Article IV Consultation - Staff Report, IMF Country Report 02/134, Washington, DC: IMF, July IMF (2002c), Czech Republic: 2002 Article IV Consultation - Staff Report, IMF Country Report 02/167, Washington, DC: IMF, August Kornai, János (1980), The Economics of Shortage, 2 vols, Amsterdam: North Holland Kornai, János (1992), The Socialist System: The Political Economy of Communism, Princeton: Princeton University Press Kornai, János, Maskin, Eric and Roland, Gérard (2002), Understanding the Soft Budget Constraint, Harvard University Working Paper Martens, Bertin, Mummett Uwe, Murrell Peter and Seabright, Paul (2002), The Institutional Economics of Foreign Aid, Cambridge: Cambridge University Press Matthäus-Maier, Ingrid and von Pischke, J D (eds) (2004), The Development of the Financial Sector in Southeast Europe: Innovative Approaches in Volatile Environments, Berlin: Springer-Verlag, forthcoming Mehl, Arnaud and Winkler, Adalbert, The Financial Sector and Economic Development: Evidence from Southeast Europe, chapter 2 (pp.11-41) of Matthäus-Maier and Von Pischke (2004), q.v. 22

23 Michalopoulos, Constantine (2003), The Western Balkans in World Trade, ch.3 of World Bank (2003), q.v. Mitra, Pradeep and Stern, Nicholas (2003), Tax Systems in Transition, World Bank Policy Research Paper 2947, Washington, DC: The World Bank, January World Bank (2000), The Road to Stability and Prosperity in South Eastern Europe: A Regional Strategy Paper, Washington, DC: The World Bank, March World Bank (2003), Trade Policies and Institutions in the Countries of South Eastern Europe in the EU Stabilization and Association Process, Report No , Europe and Central Asia Region, Washington, DC: The World Bank 23

24 Tables and Charts Table 1. Political Conditions in Southeast Europe: Brief Overview Country\Item Year(s) Comments Albania Mid-1990s Serious economic crisis due to large-scale pyramid selling of financial instruments. Albania appears not to be a candidate for EU accession in the near future (i.e. before 2010, say). Bulgaria Romania Bosnia and Herzegovina Mid-1990s Dec.1995 Candidate for EU accession in second wave, entry expected around Slow reforms in early 1990s, financial crisis led to introduction of currency board system. Candidate for EU accession in second wave, entry expected around Slow and inconsistent reforms until later 1990s Civil war and ethnic cleansing, fostered by involvement of the then Yugoslavia under its leader, Milosevic (now on trial at The Hague). Some military involvement by Croatia in W. Bosnia (e.g. around Mostar). Dayton Peace Accords under which B&H became a twostate federation. The Serbian part, capital Banja Luka, is called Republika Srpska. The rest (mostly Croat plus Bosnian Muslim) is the Federation, capital Sarajevo. Extensive use of the Euro in the Federation. Croatia Yugoslavia breaks up, Croatia gains independence after heavy fighting with what is now Serbia and Montenegro. Involvement in Bosnian wars; strong EU and US pressure to pursue more liberal, democratic policies. Could join the EU by the end of the decade (hence a probable exception to P4) FYR Macedonia Strains between Slav and Albanian groups in the population giving rise to political instability. Open ethnic conflict between Slavs and Albanians led to a NATO mission to disarm Albanian insurgents and promote stabilisation. From April 1 st 2003, this mission came under EU control. 24

25 Country\Item Year(s) Comments Serbia and Montenegro Late 1990s 2001 Attempts by Serbia to terrorise the Albanian majority population in Kosovo, large scale ethnic cleansing eventually giving rise to NATO bombing. Kosovo is now under UN administration. Some pressure for Montenegrin independence, but a high degree of autonomy within the Federation is the current position. Milosevic voted out of power and faltering moves towards democracy and more coherent economic reforms. Montenegro uses the Euro rather than the dinar as its currency. Moldova Moldova gains independence from Soviet Union, civil war as Russian enclave of Transnistria in the east of the country opposes the new state. Ceasefire supervised by OSCE, but Transnistria still refuses to accept the Moldovan government. Limited autonomy for southern region, the Gagauz Republic. Good start to reforms then slowed down badly. Sources: Various, including EBRD Transition Report, various years. 25

26 Table 2. Southeast Europe: Basic Economic Statistics Country\I tem Population, 2002 (mn) Growth in real GDP (%) (forecast) Real GDP in 2002 (% of 1989) GDP per capita (2002, US$) Inflation (based on consumer price index, %) (forecast) General government balance (2002, % of GDP) Current account balance (2002, % of GDP) Cumulative FDI inflows per capita, (US$) Albania Bulgaria Romania Bosnia and Herzegovina a na 2.4 b na Croatia FYR Macedonia Serbia and Montenegro d e Moldova SEE c 7.0 c CEB Source: Transition Report 2002 and Transition Report Update, May 2003, London: EBRD; Fact Sheet Kosovo, UNMIK, May 2003 Notes: (a) Federation; (b) Republika Srpska; (c) excl. Bosnia and Herzegovina; (d) without Kosovo; (e) Kosovo. SEE is defined as for this paper; CEB is the EBRD definition without Croatia (i.e. it comprises the eight Accession States). 26

27 Table 3. Southeast Europe: Progress with Market Reforms Country\Item Private sector share of GDP, mid-2001, % Large-scale privatization Competition policy EBRD Transition Indicators Banking reforms Non-banking financial markets/services Infrastructure Albania Bulgaria Romania Bosnia and Herzegovina Croatia FYR Macedonia Serbia and Montenegro Moldova SEE CEB Source: Transition Report 2002 and Transition Report Update, May 2003, London: EBRD Note: Last two rows - author s calculation by simple averaging. 27

28 Table 4. Southeastern Europe: Unemployment and Economic Structure Country\Item Unemployment rate in 2001 (%) Share of industry in GDP (%) 1 Albania Bulgaria Romania Share of agriculture in GDP (%) 1 Bosnia and Herzegovina Croatia FYR Macedonia Serbia and Montenegro Moldova Source: Transition Report Update, May 2003, London: EBRD Note 1. Mostly for 2000; most recent earlier year when data for 2000 not available. 28

29 Table 5. Savings and Investment: SEE and CEB Comparisons Country\Item SEE Countries Domestic savings (% of GDP) Foreign savings (% of GDP) (Data for the year 2001 wherever possible) Investment (% of GDP) Albania Bulgaria Romania Bosnia and Herzegovina Croatia FYR Macedonia Serbia and Montenegro Moldova CEB Countries Estonia Latvia Lithuania Czech Republic Hungary Poland* Slovakia Slovenia Sources: IMF (2003a-m), IMF (2002a-c) Note: * denotes

30 Table 6. Trade Flows and Tariffs of the SEE Region Country\Item Exports of Goods and Services (% of GDP) Imports of Goods and Services (% of GDP) (X+M)/Y (%) Average Tariff (%) Tariff Bands SEE Countries (Data for the year 2000 wherever possible) Albania 6.9** 28.8** ,10,15 Bulgaria Romania Bosnia and Herzegovina 8.8** 31.4** ,5,10,15* Croatia rates FYR Macedonia Serbia and Montenegro ,5,10,15, 20,30 Kosovo 10 Uniform Montenegro 3 1,3,5,10,15 Moldova Sources: World Bank (2003); UNECE Country Statistics; EBRD Transition Report Update, May 2003 Note: * plus about 250 specific tariff duties for agricultural products; ** goods only. 30

31 Table 7. Foreign Direct Investment and External Debt in South Eastern Europe Country\Item Cumulative FDI ( ) Cumulative FDI/head ( ) FDI inflows in 2002 Debt Stock in 2002 Debt Service in 2002 SEE Countries $ millions $ % of GDP $ million % of exports Albania Bulgaria Romania Bosnia and Herzegovina Croatia FYR Macedonia Serbia and Montenegro Moldova Sources: EBRD Transition Report Update, May

32 Table 8. Aid to South Eastern Europe The following charts and tables are drawn from the website of the OECD s Development Assistance Committee (DAC). 32

33 33

34 34

35 35

Review* * Received: July 25, 2008

EUROPE S TROUBLED REGION: ECONOMIC DEVELOPMENT, INSTITUTIONAL REFORM AND SOCIAL WELFARE IN THE WESTERN BALKANS, William Bartlett, 2008, Routledge, London, 257 pp. Review* While most known for its political

EUROPE S TROUBLED REGION: ECONOMIC DEVELOPMENT, INSTITUTIONAL REFORM AND SOCIAL WELFARE IN THE WESTERN BALKANS, William Bartlett, 2008, Routledge, London, 257 pp. Review* While most known for its political

what are the challenges, stakes and prospects of the EU accession negotiation?

17/10/00 CENTRAL AND EASTERN EUROPE EUROPE : ECONOMIC ACHIEVEMENTS, EUROPEAN INTEGRATION PROSPECTS Roadshow EMEA Strategy Product London, October 17, and New York, October 25, 2000 The European Counsel

17/10/00 CENTRAL AND EASTERN EUROPE EUROPE : ECONOMIC ACHIEVEMENTS, EUROPEAN INTEGRATION PROSPECTS Roadshow EMEA Strategy Product London, October 17, and New York, October 25, 2000 The European Counsel

The Economies in Transition: The Recovery

Georgetown University From the SelectedWorks of Robert C. Shelburne October, 2011 The Economies in Transition: The Recovery Robert C. Shelburne, United Nations Economic Commission for Europe Available

Georgetown University From the SelectedWorks of Robert C. Shelburne October, 2011 The Economies in Transition: The Recovery Robert C. Shelburne, United Nations Economic Commission for Europe Available

Economic Growth, Foreign Investments and Economic Freedom: A Case of Transition Economy Kaja Lutsoja

Economic Growth, Foreign Investments and Economic Freedom: A Case of Transition Economy Kaja Lutsoja Tallinn School of Economics and Business Administration of Tallinn University of Technology The main

Economic Growth, Foreign Investments and Economic Freedom: A Case of Transition Economy Kaja Lutsoja Tallinn School of Economics and Business Administration of Tallinn University of Technology The main

"The European Union and its Expanding Economy"

"The European Union and its Expanding Economy" Bernhard Zepter Ambassador and Head of Delegation Speech 2005/06/04 2 Dear Ladies and Gentlemen, I am delighted to have the opportunity today to talk to you

"The European Union and its Expanding Economy" Bernhard Zepter Ambassador and Head of Delegation Speech 2005/06/04 2 Dear Ladies and Gentlemen, I am delighted to have the opportunity today to talk to you

The Economies in Transition: The Recovery Project LINK, New York 2011 Robert C. Shelburne Economic Commission for Europe

The Economies in Transition: The Recovery Project LINK, New York 2011 Robert C. Shelburne Economic Commission for Europe EiT growth was similar or above developing countries pre-crisis, but significantly

The Economies in Transition: The Recovery Project LINK, New York 2011 Robert C. Shelburne Economic Commission for Europe EiT growth was similar or above developing countries pre-crisis, but significantly

Trade and Economic relations with Western Balkans

P6_TA(2009)0005 Trade and Economic relations with Western Balkans European Parliament resolution of 13 January 2009 on Trade and Economic relations with Western Balkans (2008/2149(INI)) The European Parliament,

P6_TA(2009)0005 Trade and Economic relations with Western Balkans European Parliament resolution of 13 January 2009 on Trade and Economic relations with Western Balkans (2008/2149(INI)) The European Parliament,

Stuck in Transition? STUCK IN TRANSITION? TRANSITION REPORT Jeromin Zettelmeyer Deputy Chief Economist. Turkey country visit 3-6 December 2013

TRANSITION REPORT 2013 www.tr.ebrd.com STUCK IN TRANSITION? Stuck in Transition? Turkey country visit 3-6 December 2013 Jeromin Zettelmeyer Deputy Chief Economist Piroska M. Nagy Director for Country Strategy

TRANSITION REPORT 2013 www.tr.ebrd.com STUCK IN TRANSITION? Stuck in Transition? Turkey country visit 3-6 December 2013 Jeromin Zettelmeyer Deputy Chief Economist Piroska M. Nagy Director for Country Strategy

A2 Economics. Enlargement Countries and the Euro. tutor2u Supporting Teachers: Inspiring Students. Economics Revision Focus: 2004

Supporting Teachers: Inspiring Students Economics Revision Focus: 2004 A2 Economics tutor2u (www.tutor2u.net) is the leading free online resource for Economics, Business Studies, ICT and Politics. Don

Supporting Teachers: Inspiring Students Economics Revision Focus: 2004 A2 Economics tutor2u (www.tutor2u.net) is the leading free online resource for Economics, Business Studies, ICT and Politics. Don

Comparative Economic Geography