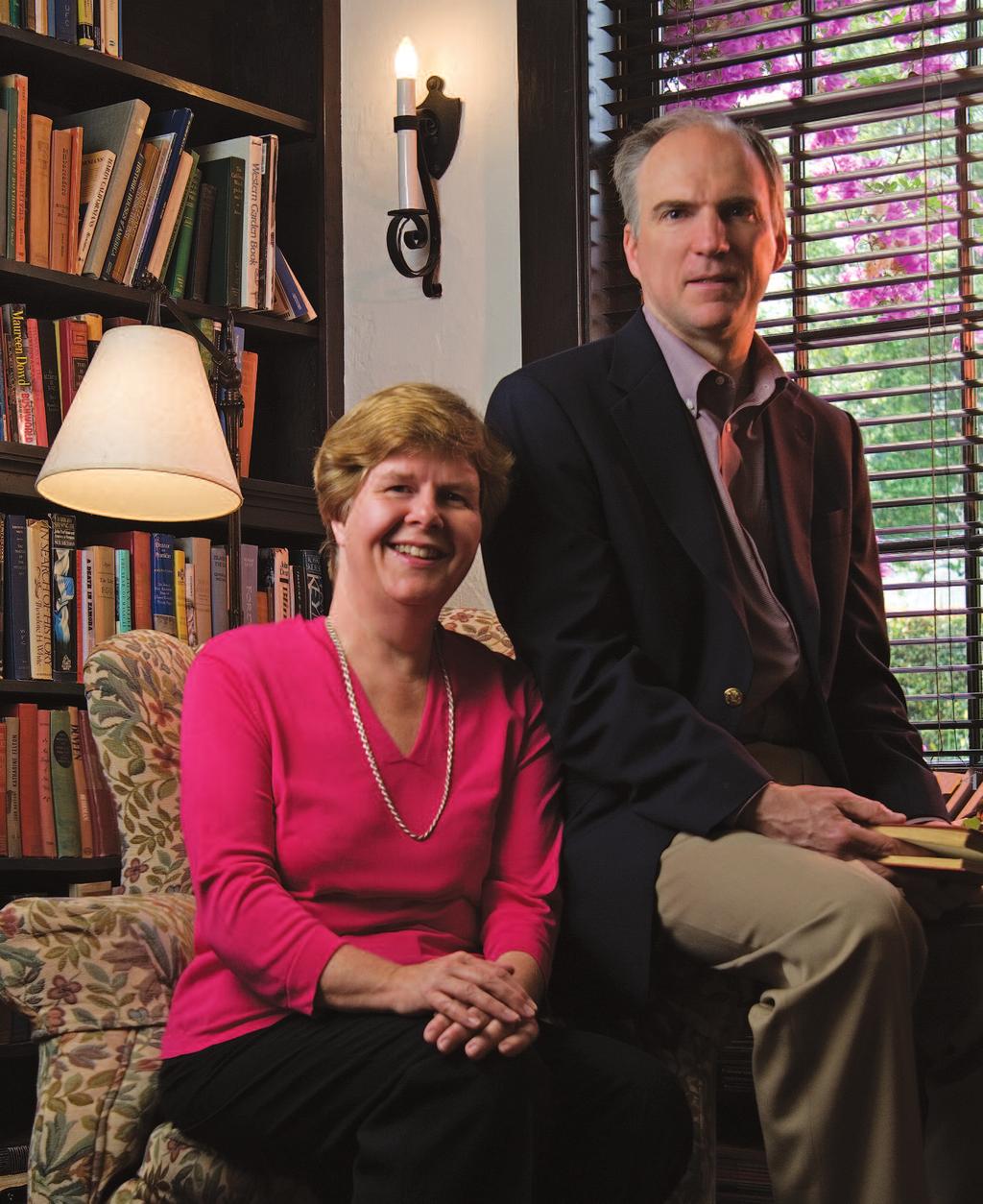

Christina and David Romer

|

|

|

- Clifton Grant

- 5 years ago

- Views:

Transcription

1

2 Christina and David Romer In times of financial turmoil, it is comforting or at a minimum, illuminating to receive counsel from those with long-term perspective. Tempered with the lessons of history, their views extract true trend from distracting noise. Guided by precedent, shaped by narrative, checked against data, the conclusions of economic historians are formed slowly and carefully. In the realm of U.S. monetary history, few economists are as qualified to provide such counsel as Christina Romer and David Romer of the University of California, Berkeley. Since 1985, when both received their doctorates from the Massachusetts Institute of Technology, the two have co-authored some of the field s central analyses of Federal Reserve policymaking, based on thorough scrutiny of Fed documents and painstaking empirical investigation. They ve made fundamental contributions to the literature on fiscal policy as well. Individually, Christina is well known for her research on the Great Depression and David for his work on microeconomic foundations of Keynesian economics. While their topics and methods are orthodox, their conclusions are often unsettling. Attempts by members of the Federal Open Market Committee to add information to Fed staff forecasts may lead to misguided actions, the Romers wrote recently. Monetary policymaking has improved since World War II but not steadily, they ve concluded; policymakers have gone astray when they deviated from sound economic theory. Contrary to conventional wisdom, the Romers have found, government spending is not reined in by tax cuts. And, according to a celebrated, if offbeat, analysis by David, football coaches should be much more aggressive on fourth down. The following conversation with the Romers covers this research as well as their work as co-directors of the monetary economics program of the National Bureau of Economic Research, their thoughts on asset prices as a focus of monetary policy, the benefits of research collaboration with one s spouse and, indeed, their perspective on current U.S. economic turmoil. Photography by Peter Tenzer 13

3 TAXES AND SPENDING Region: You recently wrote a very intriguing paper about the interplay between tax changes and government spending. Would you give us a brief description? David Romer: Well, a major motivation that people have put forward for cutting taxes is their concern that government is too large. They think that the direct approach of going through the political process to cut spending is very difficult, and so the best strategy is to cut taxes. The idea is that this will reduce the revenues that Congress has available, and over time that will force spending down. This is something that Ronald Reagan was very explicit about. It was one of the motivations for his tax cuts, and it goes under the name of the starve-the-beast hypothesis. The beast is government and its food is the revenues. Despite its importance, there s been very little empirical work on this, and most of that work boils down to looking at correlations: When revenues go up or down, do we later see spending move in the same direction? But a theme that runs through a lot of our work is that simply looking at correlation is often very misleading for getting at causation. In the context of the starve-the-beast theory, my favorite example of the issue of correlation versus causation is the fiscal history of the Korean War. The North invaded the South at the end of June A month later Truman took a few minutes out from planning the military response and wrote to Congress to say that we needed a massive tax increase because we were going to have to ramp up military spending. A big tax increase was passed and put into effect three months after the invasion. We really hadn t succeeded in increasing military spending at all at that point. So if you look just at the data, you see that taxes went up and spending went up afterwards. If you look at correlation, it looks like a great example of tax changes causing spending to change in We find no evidence for starve-thebeast. There s no systematic tendency for spending to fall after tax cuts relative to what it otherwise would have been. David Romer In postwar U.S. history what actually gives is the tax cut itself. A substantial fraction of a tax cut is typically undone in the subsequent five years. Christina Romer the same direction. But if you listen to the history I just described, it s clear that, in fact, causation went from the decision to raise spending to the decision to raise taxes. What we try to do in a lot of our work is bring in additional information from history to try to get at causation. In the paper on the starve-the-beast hypothesis, we go through the history of tax changes and take out the ones that are motivated by decisions that had already been made to increase spending, take out ones that are coming not from policy at all but from developments in the economy, and the like. We try to isolate changes in taxes that seem truly legitimate for testing the starve-the-beast hypothesis. And what we find is no evidence for starve-the-beast. There s no systematic tendency for spending to fall after tax cuts relative to what it otherwise would have been. Region: I was quite surprised by that. Christina Romer: We didn t know what we were going to find. One of the stressful things about the type of narrative research we do is that it involves a huge amount of work before the first regression can be run. But in this case, we thought the results would be interesting whichever way they came out. Region: But you did find that tax cuts were followed by something else. CR: Right. Tax cuts led, eventually, to tax increases. Basically, something has to give; there is a government budget constraint. What we thought gave when you cut taxes was spending, but we seem to find that in postwar U.S. history what actually gives is the tax cut itself. A substantial fraction of a tax cut is typically undone in the subsequent five years. FORECASTING AND THE FOMC Region: Let me jump now to monetary policy. Another provocative recent paper was your analysis of Federal Open Market Committee versus Fed staff forecasting ability, in which you basically found that the FOMC doesn t add much value. Is that an accurate summary? CR: It is, or at least it s accurate as far as we ve gone. This is our first pass at this topic. There s a limited amount of data on the FOMC forecast and the staff forecast that comes out of the Monetary Policy Reports that are done twice a year. We ve been trying to get the actual data on the forecasts of each member of the FOMC so that we can do more thorough tests. We have an ongoing discussion with the Fed trying to get those data. But the first pass at this certainly found that the FOMC has very little value added when it comes to forecasting: Once you know the staff forecast, 14

4 you can pretty much throw away the FOMC forecast. Region: And you also found that divergences between the two led to policy shocks. CR: Yes, though that part of the paper is more suggestive than conclusive. We looked at whether times when the FOMC s forecast is quite a bit different from the staff s seem to be correlated with the FOMC doing something unusual on the policy side. We find that it does seem to be. DR: If you think about how the Fed works, the forecasting results make a lot of sense. First of all, there is a huge number of staff economists, and they re very well-trained at forecasting. They devote enormous, enormous effort to it. So it really does seem like that s the staff s comparative advantage, and it would be surprising if the FOMC had a lot of value to add to that. But what we really take from this is that the role the FOMC should focus on, their comparative advantage, is making judgments. Their role shouldn t be to engage in economic forecasting or to say what the effects of different policies are likely to be, but rather to make the value judgments about outcomes. If we choose this policy, here s what the staff tells us the likely outcome is, they might say. And we could make this choice and go down this path. This is the point estimate and the uncertainty. Now, as representatives who ve been appointed through the democratic process, which path do we think is better for society? That clearly is not something that should be delegated to the staff; it s absolutely something that the FOMC should be doing. Region: So it s a deliberative role, not an analytical function. CR: I think it s somewhat deliberative, but it s more a value judgment. You re confronted with a supply shock. Do you The first pass at this certainly found that the FOMC has very little value added when it comes to forecasting: Once you know the staff forecast, you can pretty much throw away the FOMC forecast. (CR) The role the FOMC should focus on, their comparative advantage, is making judgments. Their role shouldn t be to engage in economic forecasting but rather to make the value judgments about outcomes. (DR) take it on inflation? Do you take it on output? There s a trade-off there. Someone s got to make the judgment call, which path do we want to take? There s not one that s necessarily objectively right, that every economist would say, Of course, this is what you should do. It s going to be a value judgment that should be made by people who have been appointed and confirmed through the democratic process. PRIVATE INFORMATION Region: Let me ask a question about private information in relation to forecasting. I think it was in 2000 that you wrote a paper looking at the Fed s ability to forecast inflation and output versus private forecasters ability and found that Fed forecasts were better. That indicated that the Fed had some private information. My impression is that most economists don t think the Fed has a lot of private information. Are they wrong about that, or is it that the amount of private information has diminished given greater policy transparency since the period you analyzed? DR: I think the label private information is potentially confusing, and actually the published version of the paper just refers to Federal Reserve information. We don t think the Fed is making better forecasts because some people there are collecting the industrial production data or because they have contacts on Wall Street who are giving them special information. We think that the sense in which the Fed has better information is that they take the mass of publicly available data ranging from published government series to anecdotes about what s happening at Macy s this week and do a much better job of turning those data into a forecast. CR: What David is describing is closely related to what we said about the FOMC versus the staff. No private forecaster, just like no member of the FOMC, puts the resources into forecasting that the Fed does. It has hundreds of Ph.D. economists, not to mention all the people at the regional banks. So we think that it s a processing advantage, not getting the data sooner or having secret contacts or whatever. On the issue of whether this is a common view, I think the question of No private forecaster, just like no member of the FOMC, puts the resources into forecasting that the Fed does. It has hundreds of Ph.D. economists, not to mention all the people at the regional banks. Our empirical evidence says that they have some information relative to private forecasters. (CR) 15

5 whether the Fed has useful information is an empirical one. It s not one we should try to answer from the seat of our pants. And, we certainly think that our empirical evidence says that they have some information relative to private forecasters. I think it s been confirmed, hasn t it? DR: I think so. [Princeton economist] Chris Sims has a paper on this [ /bppolicy.pdf]. He came to the same conclusion. There are a lot of statistical results out there of the Is the t-statistic 1.8 or 2.2? variety. But the results about Fed information aren t in that category. This is something that statistically is overwhelming. If you know a high-profile commercial forecast of inflation and someone handed you the Fed Greenbook, the evidence is very strong that you would want to put almost complete weight on the Greenbook. CR: I do think that there is a question of whether the Fed s advantage may have changed over time. There certainly have been big increases in Fed transparency. To the degree that there s more signaling now of here s what we re thinking and here s where we re going, the Fed s informational advantage may have lessened over time. EVOLUTION OF UNDERSTANDING Region: At the Kansas City Fed s 2002 Jackson Hole symposium, you spoke about the Evolution of Economic Understanding and Postwar Stabilization Policy. You identified three distinct phases in that evolution, ending in the 1990s with a sophisticated model that seemed sensible. And you said this suggests both a note of optimism and a note of caution about the future of stabilization policy. Would you describe those phases and elaborate on those notes? CR: I ll start with the phases. There s a desire to think that we gradually learn things over time, and so we get gradually better and better policy. But, what we found was a more complicated evolution. We found that in the 1950s, policymakers didn t have a sophisticated model of the economy, but in its basics, it was actually pretty good. They had a sense that inflation was bad. They had a sense that there was a kind of capacity constraint to the economy, and that if you tried to push the economy too far, eventually you wouldn t get any benefits in terms of lower unemployment; all you d get is inflation. It was a sort of proto-natural-rate kind of view. As a result, policy was also pretty good. It wasn t perfect they were certainly doing the sort of stepping on the gas, stepping on the brakes that Milton Friedman always criticized but overall, the basics were pretty good. Inflation was kept in check and recessions were brief. Then what we see is deterioration in the 1960s and 70s. In the process of trying to add better analytics, policymakers in fact took a giant wrong turn in understanding how the economy operates. They first had the idea that there was a permanent trade-off between inflation and unemployment, so if we were just willing to have more inflation, then we could permanently lower unemployment. That view disappeared pretty fast, but then policymakers replaced it with a natural rate of unemployment view where they thought the sustainable level of unemployment was, maybe, 3 percent. Then we see Arthur Burns in the early 1970s struggling with the fact that that didn t seem to be right. So he added the idea that maybe monetary policy just can t do anything that inflation doesn t respond to slack. So another twist and turn, but a wrong turn. Policy in this period reflected these views it was wildly overly expansionary most of the time, with a few half-hearted monetary contractions aimed at controlling inflation thrown in. Not until the Volcker, Greenspan and now Bernanke era do you get a basically pretty sensible model the view that inflation is bad, the sustainable rate of unemployment is moderate and inflation will respond to slack. I think we re both pretty strongly of the view that the Great Moderation the excellent performance of the U.S. macroeconomy over the last quarter century is not just luck. A big part of it is improvements in the conduct of monetary policy related to improvements in economic understanding. (DR) Region: You call it sensible and sophisticated. CR: This is in contrast with the 1950s, which was sensible but clearly crude. The modern framework has a lot of sophisticated features that policymakers in the 1950s didn t have. The important thing is that these sensible views have led, by and large, to moderate, well-tempered policy. The result has been low inflation and remarkably steady growth over the past 25 years. Region: And your notes of caution and optimism? DR: The optimism is to say that we ve now had monetary policy run on a very sound basis for 25 years. I think we re both pretty strongly of the view that the Great Moderation the excellent performance of the U.S. macroeconomy over the last quarter century is not just luck. A big part of it is improvements in the conduct of monetary policy related 16

6 to improvements in economic understanding. That s the optimistic note, that maybe good ideas and good policy can continue. The note of caution is that we haven t had a monolithic march toward better and better knowledge. So if people get complacent and start appointing people who have misguided ideas to the Federal Reserve, we can have a backsliding. CR: Another wrong turn. DR: Yes, another wrong turn in how policy is conducted. And so that s something we have to be vigilant about. We have to think about ways to ensure that monetary policy is consistently run on the basis of the best available ideas about how the economy works. THEORETICAL PROGRESS Region: From my reading of the symposium proceedings, it seemed there was a fair amount of criticism from the discussant [NYU economist Thomas Sargent] and others, saying among other things and I m from Minnesota so I have to bring this up that your analysis left out major theoretical advances, such as rational expectations and the time inconsistency problem, among others. Is it your view that these theoretical advances don t have much of a role in improved policy? CR: I think our view is that to understand what went on in U.S. macro history, these things aren t crucial. Issues of credibility and rational expectations surely can matter and surely are something that any good monetary policymaker should be thinking about. But in terms of explaining why policy went so astray in the early 1970s, it wasn t time inconsistency, it wasn t failing to take credibility into account. It was Arthur Burns saying things like, Monetary policy can t do anything. So in terms of the source of the big policy mistakes, we think that s not the best place to look. Issues of credibility and rational expectations surely can matter and surely are something that any good monetary policymaker should be thinking about. But in terms of explaining why policy went so astray in the early 1970s we think that s not the best place to look. (CR) The paper I d cite that I think is very supportive of this comes very much from a rational expectations learning tradition. It s by [Northwestern University economist] Giorgio Primiceri in the 2006 Quarterly Journal of Economics. It uses a sophisticated Sargent-esque learning model, but finds that learning about just a few variables the estimates of the natural rate and the sensitivity of inflation to deviations from the natural rate can explain the evolution of policy and outcomes incredibly well. So again, I think it s an empirical issue, not a theoretical or methodological issue. DR: The other example I would add besides the one of what went wrong in the 1970s is what finally went right when Volcker came in. The crucial thing was that Volcker had a much more sensible view of how the economy operated, and he took actions consistent with those views. He said, in effect, Okay, look, we have to get inflation down. Monetary policy is capable of doing that. The natural rate of unemployment is pretty substantial, so to reduce inflation we re going to have very tight policy and the unemployment rate is going to have to go quite high. As things turned out, it was actually less costly to bring inflation down than most economists had expected, and a likely reason is that at some point people started to realize that the Fed was really serious. The Fed gained some credibility, and so you didn t have purely mechanical backward-looking expectations. You got kind of a credibility or rational expectations kick. So if you want to describe the very big picture of what happened, rational expectations isn t central. But if you want to get into a quantitative account and match the numbers, then that becomes something to consider. So, it s on the list, but it s not one of the top ones for the period we were looking at. A FOURTH PHASE? Region: It s too early to write our history about the current period, of course, but people are again talking about stagflation, and I guess it comes to a question of, What have we learned after all? Is the Great Moderation over? Have we entered a fourth phase? CR: The key question is what happens from here. For the Great Moderation, we believe that good policy was a crucial part. But another thing that a lot of the studies have found is that during the Great Moderation, we didn t have big shocks. For example, we didn t have a lot of oil price shocks. Ben Bernanke has been dealt just a rotten hand; there are awful shocks hitting the U.S. macroeconomy. The issue is going to be, What do we do from here? There s no way, confronted with some of these things, that you can have low inflation and 4 percent real growth every year. (CR) 17

7 We re now in a nasty period. Ben Bernanke has been dealt just a rotten hand; there are awful shocks hitting the U.S. macroeconomy. The issue is going to be, What do we do from here? There s no way, confronted with some of these things, that you can have low inflation and 4 percent real growth every year. What we don t have to do is what they did in the 1970s, which is to compound bad shocks with bad policy. The Fed ran massively expansionary monetary policy at a time when conditions didn t warrant it. The result was very high inflation, followed by massively high unemployment to get it down. So I think the real question is going to be, What s the line we walk from here? Think about the action we saw just today [June 25], where the FOMC didn t keep lowering the federal funds rate. It said, We re probably through the worst in the financial markets; we had to fight that fire, but now we re going to look at what s happening to inflation. There are benefits to low inflation, and so we re going to have to think about how much we stimulate the real economy and how much we re concerned about inflation. The fact that the FOMC is thinking this way suggests that even if they don t do everything exactly right, they re not going to make the sorts of huge mistakes policymakers made in the 1970s. ASSET PRICES Region: It s long been Fed doctrine that we really don t have the ability to identify asset price bubbles with great accuracy, nor address them with alacrity. But given the housing market, the dotcom bust given much of this past decade, I guess some policymakers are reconsidering whether asset prices should be a focus of Fed policy. What is your view? DR: I ve always been of the view that it s very hard to identify an asset price bubble, and I don t think the Fed should be in the business of trying to determine what fundamental values are. A nice It might be best to think not in terms of trying to manage asset prices or identify fundamental values, but rather that rapid increases in asset prices are another indicator of potential overheating. (DR) concrete example of this is that when Alan Greenspan gave his famous irrational exuberance speech, the Dow- Jones average was at something like 6,000; it eventually fell, but it had risen a great deal more before it fell. So in retrospect it looks like 6,000 was not too high for the Dow at that time. I think the bigger issues are that rapid run-ups in asset prices, first of all, tend to stimulate the economy a lot, and secondly, can be followed by declines. So it might be best to think not in terms of trying to manage asset prices or identify fundamental values, but rather that rapid increases in asset prices are another indicator of potential overheating that the Fed might want to consider in how it conducts policy. To me that makes sense. I think it s really framing the issue in a confusing way to try to focus on the question of the Fed directly managing asset prices or trying to have its own view of what fundamentals should be. I think that s not where the Fed should be. But I think they should still be thinking pretty hard about asset markets. CR: I like David s point about big rises in asset prices as an indicator that maybe the economy is too hot, or that they re one of the things that you should look at. In thinking about the Greenspan era, there s a tendency for people like [former Fed Governor] Larry Meyer to say, Oh, Alan Greenspan was so much smarter than I was because he realized that the unemployment rate could go down to an incredibly low level. I m not sure that s right. In some sense maybe we were taking things too far. Being aggressive in seeing just how good we can make things in the short run might be setting up these kinds of bubbles. I think we might want to take rapid asset price increases as one indication that we should be following a more moderate policy. CHOOSING A CHAIR Region: In 2004, you wrote a paper with lessons about selecting a Fed chair. You suggested that the best way to predict what a chair would do was simply to read what they d written. About two years later, Ben Bernanke was sworn in as chair. He s been there for about two and a half years. Have your lessons held up? In other words, do you feel that Bernanke s writings and his testimony were an accurate predictor of what he s done, of the policy he s pursued? CR: Yes, I think they were very much so. We argued that what you are looking for in the record is the potential chair s framework about the economy. What we learned from preparing the Evolution of Economic Understanding paper is that policy tends to go astray when people have wacky views about how the economy works. When you read G. William Miller, for example, you can just tell that he doesn t have a sensible framework. It s a framework that would lead you to an overly expansionary policy. When you read Ben Bernanke s statements and papers, you see a very sensible framework and a 18

8 reasonable view of what the Federal Reserve can and cannot accomplish. I think the actions he has taken are consistent with the views he expressed before becoming chair. So, we d view Chairman Bernanke as a triumph for our paper. In fact, if you were to read our paper and ask who would be the perfect person, it probably would have been either Stan Fischer or Ben Bernanke that s what came out of our analysis. And again, Bernanke has been dealt a horrible hand the meltdown in financial markets, the collapse of housing prices, huge oil price shocks and I think the Fed has done a good job of trying to navigate us through this. Region: One of the steps the Fed has taken is creating vehicles to open up the credit window more broadly. How important are these recent innovations in terms of Fed policy history? DR: I m not enough of an expert on this to know, but I think this is not really the big issue in the context of policy. The big issue is that, faced with problems in financial markets, the Fed responded aggressively, after a little bit of a delay, with easing. That seemed extremely appropriate. I start from a fairly traditionalist view, that the right thing for the Fed to do if the economy is in trouble, rather than trying to identify particular problem areas in financial markets that need intervention, is to provide lots of liquidity and keep interest rates low. I haven t studied the case for these more innovative steps enough to have a firm When you read Ben Bernanke s statements and papers, you see a very sensible framework and a reasonable view of what the Federal Reserve can and cannot accomplish. I think the actions he has taken are consistent with the views he expressed before becoming chair. (CR) view about whether they were wise or not. But I don t think they re the big picture of what the Fed has been doing. CR: I agree. Why was the Fed created? The Fed was created because we d gone through several devastating financial panics in the late 1800s and early 1900s. So, faced with what could have turned into a panic in 2008, the Fed responded aggressively. It s exactly the textbook description of what they should have done. Now the innovative things, such as lending to investment banks, raise big regulatory issues that I think someone needs to be thinking about a lot making sure they re dealing with them correctly. But again the big picture was, don t let the New York financial market go under because it would have devastating real economic consequences. That was exactly the right focus for policy. NBER AND MONETARY ECONOMICS Region: In a couple of weeks, you ll head to Boston to lead the monetary economics workshop of the National Bureau of Economic Research. It runs five straight afternoon sessions, 14 papers, I think. I was struck by the diversity of presentations, from a Larry Summers discussion on recent developments in financial markets to a paper by two young Harvard economists on frequency of price changes and exchange rate pass-through. How long have you run this group? CR: I have to think. Is it four years? DR: That s what I was going to say. CR: On the content, we deliberately take a very inclusive role of what counts as monetary economics. The unofficial definition of monetary economics that we inherited, going back to Greg Mankiw and Ben Bernanke, who ran this program before us, is that it s anything monetary policymakers should be interested in. I do worry that monetary economics may be narrowing we may be losing the empirical side. To the degree we re trying to do any social engineering, it s to try to encourage the breadth of empirical studies. (CR) So if you think of it that way, it s a lot of things. It obviously includes a wide range of macro topics, but it may also get into the microeconomics of price setting and financial market regulation. Anything that gets you information on how the macroeconomy operates we think is fair game. Subject to that constraint, we just look for the best papers and try to be pretty aggressive in getting what we think is good and exciting research, so people come and it s an interesting meeting. DR: I think we are very committed to the diversity of approaches to empirical work. So you ll see some very high-tech, Bayesian time-varying parameter VAR sorts of papers; you ll see things in economic history; you ll see researchers who ve gone out and talked to people at firms about how they went about changing the prices for a line of products. People who attend the workshop seem to appreciate that whole range of approaches. Region: Four years as co-chairs may not be a long enough perspective to answer 19

9 this next question, but you ve certainly been attending the workshop for longer. Given where we are now with monetary policy, do you feel that monetary economists at the NBER, and overall, have been investigating the right questions, have they had the right research focuses? CR: Oh, that s a good question. I think yes and no. The nice thing about the way research is done is, it s a thousand flowers blooming. People are just trying lots of different things. Some of them have proved to be very exciting and useful, and some of them have been less so. I do worry that monetary economics may be narrowing. For some economists using a standard DSGE [dynamic stochastic general equilibrium] model, it s becoming let s change this equation, let s change that one. I worry that we may be losing the empirical side. I worry that we ve gone too far into let s just calibrate this, let s check this covariance. I sure hope people will keep thinking along the lines of, Is there an innovative way of testing this? Is there a variable we haven t thought of? Is there a natural experiment? To the degree we re trying to do any social engineering, it s to try to encourage the breadth of empirical studies, so we don t narrow too much. Do you agree? DR: I do. COLLABORATION Region: I ve long been interested in the process of collaboration among scholars how topics are chosen, labor divided, disputes resolved but I ve never considered how marriage might play into that. You ve co-authored many papers, run the monetary economics workshop for four years and made a wide range of employment decisions together. How would you describe your working relationship? DR: My sense is that the collaboration is David: My sense is that the collaboration is closer than it is in many co-authorship relationships, in a couple of ways. First, I think we do more steps of the research together. The other way the collaboration is closer is, I think, we re Christina: We can be brutally frank. David: Exactly. closer than it is in many co-authorship relationships, in a couple of ways. First, I think we do more steps of the research together. We spend a lot of time together in front of the computer or flipping through documents. Someone recently asked which of us had done the classification of the tax changes by motivation for our work on fiscal policy. And we both sat in awkward silence because the question made no sense to us. Finally, we said, We did it together. One of us might take the first pass at reading the documents for a particular episode, and if it was straightforward, that was the end of the matter. But if there was any subtlety or disagreement, room for ambiguity, then we d both study the record, and we d make the case back and forth until we resolved things. The other way the collaboration is closer is, I think, we re CR: We can be brutally frank. DR: Exactly. We can be more frank in our criticism because there s plenty of time to iron out the differences. If one of us isn t happy with the way someone has organized a section, we re not shy about expressing that. For one of our papers, I have a stack of outlines. On the bottom is #1, on top of that is outline #2, and then outlines #3 and #4. We went back and forth just trying to organize it. CR: We often say that the professional collaboration solved all the bargaining issues in the marriage. Normally it s, Who does the laundry? or Who washes the dishes? Well, for us it s, I ll wash the dishes, I ll play with the kids, you go write the computer program. Given that there s lots of work to do, it certainly makes it easy to negotiate over who does what. SEPARATE PIECES Region: Of course, you ve also published papers separately, and I d be remiss if I didn t ask David about football. Can you tell me about your famous 2006 Journal of Political Economy paper, Do Firms Maximize? DR: [Laughs.] That was a completely offbeat paper. The initial motivation really was just the narrow question of whether football coaches are getting a particular decision what to do on fourth down right. I found it intriguing, and at some point I found I had the tools to address it. And I got a bunch of undergraduates to help me gather the data. It was in some sense a paper that wrote itself. The number of undergraduates who responded to the of Would you like to work on a project about football? was just astronomical. I find it interesting in various ways. The way that s emphasized in the published version is that it s a way of testing something that s very difficult to test normally. We can test whether individuals make maximizing choices, but it s much harder for firms because the decisions are more complicated, and the 20

10 More About Christina Romer More About David Romer Current Positions Class of 1957 Professor of Economics, University of California, Berkeley, since Joined Berkeley faculty in 1988; promoted to full professor in 1993 Co-director, Program in Monetary Economics, National Bureau of Economic Research, since 2003; Business Cycle Dating Committee since 2003; Research Associate since 1990 Previous Position Assistant Professor of Economics and Public Affairs, Woodrow Wilson School, Princeton University, Professional Activities Vice President, American Economic Association, 2006; various committees since 2001 Various committees, Economic History Association, since 1995 Editorial board, American Economic Journal: Macroeconomics, since 2007; Review of Economics and Statistics, ; Journal of Economic History, Training Seminar on the Great Depression, International Monetary Fund, 2002, 2003, 2005 Honors and Awards Fellow, American Academy of Arts and Sciences, since 2004 John Simon Guggenheim Memorial Foundation Fellowship, Distinguished Teaching Award, University of California, Berkeley, 1994 National Science Foundation Presidential Young Investigator Award, Alfred P. Sloan Research Fellowship, National Bureau of Economic Research Olin Fellowship, Publications Co-editor, with David H. Romer, Reducing Inflation: Motivation and Strategy, University of Chicago Press for NBER, 1997 Author of numerous journal articles, with research focused on the effects and determinants of monetary policy, economic fluctuations over the 20th century, the causes of the Great Depression, the history and effects of fiscal policy, and historical macroeconomic data Education Massachusetts Institute of Technology, Ph.D., 1985 College of William and Mary, B.A., 1981 Current Positions Herman Royer Professor in Political Economy, University of California, Berkeley, since Joined Berkeley faculty in 1988; promoted to full professor in 1993 Co-director, Program in Monetary Economics, National Bureau of Economic Research, since 2003; Business Cycle Dating Committee since 2003; Research Associate since 1993 Previous Positions Assistant Professor, Princeton University, Visiting Professor, Stanford University, Fall 1995; Visiting Associate Professor, Spring 1993 Visiting Assistant Professor, Massachusetts Institute of Technology, 1988 Professional Activities Executive Committee, American Economic Association, Editorial board, American Economic Journal: Macroeconomics, since 2007; Journal of Money, Credit and Banking, since 1992; B.E. Journals in Macroeconomics, ; Economics Letters, ; American Economic Review, ; Quarterly Journal of Economics, Honors and Awards Fellow, American Academy of Arts and Sciences, since 2006 Adviser of the Year Award, University of California, Berkeley, Graduate Economic Association, 1999, 1993 Teacher of the Year Award, University of California, Berkeley, Graduate Economic Association, 1998 Alfred P. Sloan Research Fellowship, Valedictorian, Princeton University, 1980 Publications Author of Advanced Macroeconomics, McGraw-Hill. 1st ed., 1996; 2nd ed., 2001; 3rd ed., 2006 Co-editor, with Christina D. Romer, Reducing Inflation: Motivation and Strategy, University of Chicago Press for NBER, 1997 Author of numerous journal articles, with research focused on the effects and determinants of monetary policy, microeconomic foundations of Keynesian economics, empirical evidence on economic growth, the history and effects of fiscal policy, and stock market volatility Education Massachusetts Institute of Technology, Ph.D., 1985 Princeton University, A.B.,

11 data usually aren t available. Another thing I like about the paper is that it s an illustration of how analytical tools can be useful. I ve given seminars on this paper to undergraduates in the math department. I ve gone to a junior high school math class to say, Here s something interesting you can do with math that you wouldn t have expected. So it was an interesting diversion from other things that I ve done. Region: And you found that? DR: The bottom line is that if the goal is to win football games, teams should be dramatically more aggressive on fourth down. They should go for it much, much more often. I focused on situations early in the game with the score tied, so time and score aren t issues, and found that at fourth and short yardage pretty much anywhere on the field, you should go for it. If you re down close to the goal line, you should try for the touchdown. The main place the math comes in is in thinking through the whole chain of events after the fourth down play. In the example of fourth and goal near the goal line, if you go for the touchdown and you fail, then you ve lost the three points you would have gotten from a field goal, but you ve left the other team in really crummy field position, and that partially offsets the fact that you didn t get the three points. And what you find when you do the analysis is that that s a very big consideration. CR: The very sad and ironic thing is that now football teams are going for it less often on fourth down than before David wrote this paper! The armchair psychologist view of it is that they don t want to be doing what the academic egghead says they should. They want to be following their own route. Region: So, David shaped the game. CR: But in the wrong direction. The other side of it is, the fans love him. The bottom line is that if the goal is to win football games, teams should be dramatically more aggressive on fourth down. They should go for it much, much more often. (DR) They all say, I always knew they should be going for it on fourth, and now you ve shown it! Region: I doubt you ve gotten quite as much attention for your recent presentation to the Economic History Association on macro policy in the 1960s, but I found it equally interesting. Would you tell us about it? CR: That paper built on the work we did on the Evolution of Economic Understanding, but added some of what we were learning from our new work on fiscal policy. The EHA was having a session at the Lyndon Johnson Presidential Library in Views took an unfortunate turn in the 1960s and 70s. Policymakers started to believe that budget balance was not important even over an extended horizon. I think these are wrong turns that we haven t corrected yet as evidenced by our ever-worsening long-term fiscal outlook. (CR) Austin, Texas, and they wanted a talk about macro policy in the 1960s. The question I focused on was, What went wrong? And the answer is, Basically, bad ideas. There was a revolution in ideas, but it was a misguided revolution. We ve already talked about the change in ideas about short-run stabilization thinking we could buy ourselves lower unemployment by just accepting some inflation. The thing I added in this paper was the long-run fiscal side. We not only had a revolution in our views about how the macroeconomy works in the short run, but also a change in views about the importance of long-run budget balance. The paper looked at how that evolved. What s very striking is that we had a pretty sensible long-run fiscal view in the 1950s the budget should be balanced over the medium run, but not each and every year and not in exceptional circumstances. And, policy choices reflected that view the budget was balanced on average, but not in recessions and not during wars. But views took an unfortunate turn in the 1960s and 70s. Policymakers started to believe that budget balance was not important even over an extended horizon, and that tax cuts would pay for themselves. And views took another wrong turn in the 1980s, when policymakers added notions such as the starve-the-beast hypothesis that tax cuts would force spending cuts. I think these are wrong turns that we haven t corrected yet as evidenced by our ever-worsening long-term fiscal outlook. That s the big picture that came out of this study. Region: Thank you both very much. Douglas Clement June 25,

Systematic Policy and Forward Guidance

Systematic Policy and Forward Guidance Money Marketeers of New York University, Inc. Down Town Association New York, NY March 25, 2014 Charles I. Plosser President and CEO Federal Reserve Bank of Philadelphia

Systematic Policy and Forward Guidance Money Marketeers of New York University, Inc. Down Town Association New York, NY March 25, 2014 Charles I. Plosser President and CEO Federal Reserve Bank of Philadelphia

LECTURE 2 The Effects of Monetary Changes: Narrative Evidence and Natural Experiments. August 29, 2018

Economics 210c/236a Fall 2018 Christina Romer David Romer LECTURE 2 The Effects of Monetary Changes: Narrative Evidence and Natural Experiments August 29, 2018 I. INTRODUCTION AND THE ST. LOUIS EQUATION

Economics 210c/236a Fall 2018 Christina Romer David Romer LECTURE 2 The Effects of Monetary Changes: Narrative Evidence and Natural Experiments August 29, 2018 I. INTRODUCTION AND THE ST. LOUIS EQUATION

Monetary Theory and Central Banking By Allan H. Meltzer * Carnegie Mellon University and The American Enterprise Institute

Monetary Theory and Central Banking By Allan H. Meltzer * Carnegie Mellon University and The American Enterprise Institute It is a privilege to present these comments at a symposium that honors Otmar Issing.

Monetary Theory and Central Banking By Allan H. Meltzer * Carnegie Mellon University and The American Enterprise Institute It is a privilege to present these comments at a symposium that honors Otmar Issing.

Legislating a Rule for Monetary Policy John B. Taylor

Legislating a Rule for Monetary Policy John B. Taylor In these remarks I discuss a proposal to legislate a rule for monetary policy. The proposal modernizes laws first passed in the late 1970s, but largely

Legislating a Rule for Monetary Policy John B. Taylor In these remarks I discuss a proposal to legislate a rule for monetary policy. The proposal modernizes laws first passed in the late 1970s, but largely

Communicating a Systematic Monetary Policy

Communicating a Systematic Monetary Policy Society of American Business Editors and Writers Fall Conference City University of New York (CUNY) Graduate School of Journalism New York, NY October 10, 2014

Communicating a Systematic Monetary Policy Society of American Business Editors and Writers Fall Conference City University of New York (CUNY) Graduate School of Journalism New York, NY October 10, 2014

General Discussion: Cross-Border Macroeconomic Implications of Demographic Change

General Discussion: Cross-Border Macroeconomic Implications of Demographic Change Chair: Lawrence H. Summers Mr. Sinai: Not much attention has been paid so far to the demographics of immigration and its

General Discussion: Cross-Border Macroeconomic Implications of Demographic Change Chair: Lawrence H. Summers Mr. Sinai: Not much attention has been paid so far to the demographics of immigration and its

INTERVIEW. John B. Taylor

INTERVIEW John B. Taylor Stanford University economist John Taylor has straddled the worlds of academia and government service, with distinguished, complementary careers in each. His academic work has

INTERVIEW John B. Taylor Stanford University economist John Taylor has straddled the worlds of academia and government service, with distinguished, complementary careers in each. His academic work has

A Perspective on the Economy and Monetary Policy

A Perspective on the Economy and Monetary Policy Greater Philadelphia Chamber of Commerce Philadelphia, PA January 14, 2015 Charles I. Plosser President and CEO Federal Reserve Bank of Philadelphia The

A Perspective on the Economy and Monetary Policy Greater Philadelphia Chamber of Commerce Philadelphia, PA January 14, 2015 Charles I. Plosser President and CEO Federal Reserve Bank of Philadelphia The

Influencing Expectations in the Conduct of Monetary Policy

Influencing Expectations in the Conduct of Monetary Policy 2014 Bank of Japan Institute for Monetary and Economic Studies Conference: Monetary Policy in a Post-Financial Crisis Era Tokyo, Japan May 28,

Influencing Expectations in the Conduct of Monetary Policy 2014 Bank of Japan Institute for Monetary and Economic Studies Conference: Monetary Policy in a Post-Financial Crisis Era Tokyo, Japan May 28,

The Most Dangerous Idea in Federal Reserve History: Monetary Policy Doesn t Matter

The Most Dangerous Idea in Federal Reserve History: Monetary Policy Doesn t Matter By CHRISTINA D. ROMER AND DAVID H. ROMER* * C. Romer: University of California, Berkeley, Berkeley, CA 94720-3880 (email:

The Most Dangerous Idea in Federal Reserve History: Monetary Policy Doesn t Matter By CHRISTINA D. ROMER AND DAVID H. ROMER* * C. Romer: University of California, Berkeley, Berkeley, CA 94720-3880 (email:

Charles I Plosser: A progress report on our monetary policy framework

Charles I Plosser: A progress report on our monetary policy framework Speech by Mr Charles I Plosser, President and Chief Executive Officer of the Federal Reserve Bank of Philadelphia, at the Forecasters

Charles I Plosser: A progress report on our monetary policy framework Speech by Mr Charles I Plosser, President and Chief Executive Officer of the Federal Reserve Bank of Philadelphia, at the Forecasters

Is China a Currency Manipulator?

Peterson Perspectives Interviews on Current Topics Is China a Currency Manipulator? Morris Goldstein says Treasury Secretary Geithner was correct to label China a currency manipulator but argues for a

Peterson Perspectives Interviews on Current Topics Is China a Currency Manipulator? Morris Goldstein says Treasury Secretary Geithner was correct to label China a currency manipulator but argues for a

The Rationale for Independent Monetary Policy

The Rationale for Independent Monetary Policy Bennett T. McCallum Tepper School of Business, Carnegie Mellon University Shadow Open Market Committee March 26, 2010 1. Introduction Recently there has been

The Rationale for Independent Monetary Policy Bennett T. McCallum Tepper School of Business, Carnegie Mellon University Shadow Open Market Committee March 26, 2010 1. Introduction Recently there has been

To the Central Bank Governors Panel, Jackson Hole conference, Wyoming, USA. 27 August 2005

1 Speech given by Mervyn King, Governor of the Bank of England To the Central Bank Governors Panel, Jackson Hole conference, Wyoming, USA. 27 August 2005 All speeches are available online at www.bankofengland.co.uk/publications/pages/speeches/default.aspx

1 Speech given by Mervyn King, Governor of the Bank of England To the Central Bank Governors Panel, Jackson Hole conference, Wyoming, USA. 27 August 2005 All speeches are available online at www.bankofengland.co.uk/publications/pages/speeches/default.aspx

Why Monetary Freedom Matters Ron Paul

Why Monetary Freedom Matters Ron Paul I ve thought about and have written about the Federal Reserve for a long time. I became fascinated with the monetary issue in the 1960s, having come across the Austrian

Why Monetary Freedom Matters Ron Paul I ve thought about and have written about the Federal Reserve for a long time. I became fascinated with the monetary issue in the 1960s, having come across the Austrian

Rules Versus Discretion: Assessing the Debate Over the Conduct of Monetary Policy

Rules Versus Discretion: Assessing the Debate Over the Conduct of Monetary Policy John B. Taylor Federal Reserve Bank of Boston Conference on Are Rules Made to be Broken? Discretion and Monetary Policy

Rules Versus Discretion: Assessing the Debate Over the Conduct of Monetary Policy John B. Taylor Federal Reserve Bank of Boston Conference on Are Rules Made to be Broken? Discretion and Monetary Policy

Monetary Policy Strategies: A Central Bank Panel

Monetary Policy Strategies: A Central Bank Panel Mervyn A. King Speakers at Jackson Hole normally draw out the lessons of economic theory for a particular area of economic policy. But this year we are

Monetary Policy Strategies: A Central Bank Panel Mervyn A. King Speakers at Jackson Hole normally draw out the lessons of economic theory for a particular area of economic policy. But this year we are

THE ANDREW MARR SHOW 24 TH APRIL 2016 THERESA MAY. AM: Good morning to you, Home Secretary. TM: Good morning, Andrew.

1 THE ANDREW MARR SHOW 24 TH APRIL 2016 THERESA MAY AM: Good morning to you, Home Secretary. TM: Good morning, Andrew. AM: If we stay in the EU will immigration go up or down? TM: Well, first of all nobody

1 THE ANDREW MARR SHOW 24 TH APRIL 2016 THERESA MAY AM: Good morning to you, Home Secretary. TM: Good morning, Andrew. AM: If we stay in the EU will immigration go up or down? TM: Well, first of all nobody

AN INMATES GUIDE TO. Habeas Corpus. Includes the 11 things you must know about the habeas system

AN INMATES GUIDE TO Habeas Corpus Includes the 11 things you must know about the habeas system by Walter M. Reaves, Jr. i DISCLAIMER This guide has been prepared as an aid to those who have an interest

AN INMATES GUIDE TO Habeas Corpus Includes the 11 things you must know about the habeas system by Walter M. Reaves, Jr. i DISCLAIMER This guide has been prepared as an aid to those who have an interest

From The Collected Works of Milton Friedman, compiled and edited by Robert Leeson and Charles G. Palm.

Interview. Tolerant of Nuts: Milton Friedman on His Chicago Days. Interviewed by Jason Hirschman. Whip at the University of Chicago, 20 October 1993, pp. 8-9. Used with permission of the Special Collections

Interview. Tolerant of Nuts: Milton Friedman on His Chicago Days. Interviewed by Jason Hirschman. Whip at the University of Chicago, 20 October 1993, pp. 8-9. Used with permission of the Special Collections

Celebrating 20 Years of the Bank of Mexico s Independence. Remarks by. Ben S. Bernanke. Chairman. Board of Governors of the Federal Reserve System

For release on delivery 9:00 p.m. EDT (8 p.m. local time) October 14, 2013 Celebrating 20 Years of the Bank of Mexico s Independence Remarks by Ben S. Bernanke Chairman Board of Governors of the Federal

For release on delivery 9:00 p.m. EDT (8 p.m. local time) October 14, 2013 Celebrating 20 Years of the Bank of Mexico s Independence Remarks by Ben S. Bernanke Chairman Board of Governors of the Federal

PLS 103 Lecture 3 1. Today we talk about the Missouri legislature. What we re doing in this section we

PLS 103 Lecture 3 1 Today we talk about the Missouri legislature. What we re doing in this section we finished the Constitution and now we re gonna talk about the three main branches of government today,

PLS 103 Lecture 3 1 Today we talk about the Missouri legislature. What we re doing in this section we finished the Constitution and now we re gonna talk about the three main branches of government today,

Hawks and Doves at the Federal Reserve. Michael D Bordo, Rutgers University and the Hoover Institution, Stanford University

Hawks and Doves at the Federal Reserve Michael D Bordo, Rutgers University and the Hoover Institution, Stanford University Shadow Open Market Committee Meeting Harvard Club, New York City, New York October

Hawks and Doves at the Federal Reserve Michael D Bordo, Rutgers University and the Hoover Institution, Stanford University Shadow Open Market Committee Meeting Harvard Club, New York City, New York October

Froth and Bubble: The Inconsistency of Paul Krugman s Macroeconomic Analysis

Froth and Bubble: The Inconsistency of Paul Krugman s Macroeconomic Analysis DON HARDING AND JAN LIBICH 1 Consistency is one of the touchstones used to evaluate not only arguments but also the people that

Froth and Bubble: The Inconsistency of Paul Krugman s Macroeconomic Analysis DON HARDING AND JAN LIBICH 1 Consistency is one of the touchstones used to evaluate not only arguments but also the people that

Robert Owen and His Legacy. Esther L. George President and Chief Executive Officer Federal Reserve Bank of Kansas City

Robert Owen and His Legacy Esther L. George President and Chief Executive Officer Federal Reserve Bank of Kansas City Oklahoma History Center Oklahoma City October 16, 2013 The views expressed by the author

Robert Owen and His Legacy Esther L. George President and Chief Executive Officer Federal Reserve Bank of Kansas City Oklahoma History Center Oklahoma City October 16, 2013 The views expressed by the author

John Maynard Keynes v. Friedrich Hayek Part I: The Battle of Ideas (Commanding Heights) 2. What economic concepts did John Maynard Keynes invent?

2. What economic concepts did John Maynard Keynes invent?") E&F/Raffel Chapter #4: John Maynard Keynes v. Friedrich Hayek Part I: The Battle of Ideas (Commanding Heights) 1. What impacts did Germany s hyperinflation have on the middle class? What lesson did Friedrich

E&F/Raffel Chapter #4: John Maynard Keynes v. Friedrich Hayek Part I: The Battle of Ideas (Commanding Heights) 1. What impacts did Germany s hyperinflation have on the middle class? What lesson did Friedrich

Federal Reserve Reform Proposals. John B. Taylor 1

Federal Reserve Reform Proposals John B. Taylor 1 Testimony before the Subcommittee on Monetary Policy and Trade Committee on Financial Services U.S. House of Representatives July 22, 2015 Chair Huizenga,

Federal Reserve Reform Proposals John B. Taylor 1 Testimony before the Subcommittee on Monetary Policy and Trade Committee on Financial Services U.S. House of Representatives July 22, 2015 Chair Huizenga,

HARRY JOHNSON. Corden on Harry s View of the Scientific Enterprise

HARRY JOHNSON Corden on Harry s View of the Scientific Enterprise Presentation at the History of Economics Society Conference, Vancouver, July 2000. Remembrance and Appreciation Session: Harry G. Johnson.

HARRY JOHNSON Corden on Harry s View of the Scientific Enterprise Presentation at the History of Economics Society Conference, Vancouver, July 2000. Remembrance and Appreciation Session: Harry G. Johnson.

Towards an Exit Strategy: Discretion or Rules? Discorso Bruno Leoni John B. Taylor Stanford University. Palazzo Clerici, Milano

Towards an Exit Strategy: Discretion or Rules? Discorso Bruno Leoni 2011 John B. Taylor Stanford University Palazzo Clerici, Milano February 7, 2011 I want to thank the Instituto Bruno Leoni for inviting

Towards an Exit Strategy: Discretion or Rules? Discorso Bruno Leoni 2011 John B. Taylor Stanford University Palazzo Clerici, Milano February 7, 2011 I want to thank the Instituto Bruno Leoni for inviting

PLS 103 Lecture 8 1. Today we re gonna talk about the initiative and referendum process in Missouri. We

PLS 103 Lecture 8 1 Today we re gonna talk about the initiative and referendum process in Missouri. We introduced the initiative and referendum process when we talked about the Constitution. We talked

PLS 103 Lecture 8 1 Today we re gonna talk about the initiative and referendum process in Missouri. We introduced the initiative and referendum process when we talked about the Constitution. We talked

2018 State Legislative Elections: Will History Prevail? Sept. 27, 2018 OAS Episode 44

The Our American States podcast produced by the National Conference of State Legislatures is where you hear compelling conversations that tell the story of America s state legislatures, the people in them,

The Our American States podcast produced by the National Conference of State Legislatures is where you hear compelling conversations that tell the story of America s state legislatures, the people in them,

Opening the Temple. An Essay by President and CEO John C. Williams FEDERAL RESERVE BANK OF SAN FRANCISCO 2011 ANNUAL REPORT

Opening the Temple An Essay by President and CEO John C. Williams FEDERAL RESERVE BANK OF SAN FRANCISCO 2011 ANNUAL REPORT Opening the Temple By President and CEO John C. Williams Twenty-five years ago,

Opening the Temple An Essay by President and CEO John C. Williams FEDERAL RESERVE BANK OF SAN FRANCISCO 2011 ANNUAL REPORT Opening the Temple By President and CEO John C. Williams Twenty-five years ago,

Obama Worse than Bush (translated from Polish by Irena Czernichowska)

") Obama Worse than Bush (translated from Polish by Irena Czernichowska) Is it a lack of government control over the economy that caused the catastrophe? No, it is government interventions that caused, prolonged,

Obama Worse than Bush (translated from Polish by Irena Czernichowska) Is it a lack of government control over the economy that caused the catastrophe? No, it is government interventions that caused, prolonged,

SCHOOLS OF ECONOMICS. Classical, Keynesian, & Monetary

SCHOOLS OF ECONOMICS Classical, Keynesian, & Monetary CLASSICAL THEORY Also known as Neo- Classical Supply Side Trickle Down Free Trade FIVE CLASSICAL ECONOMIC BASICS In the long run, competition forces

SCHOOLS OF ECONOMICS Classical, Keynesian, & Monetary CLASSICAL THEORY Also known as Neo- Classical Supply Side Trickle Down Free Trade FIVE CLASSICAL ECONOMIC BASICS In the long run, competition forces

10/7/2013 SCHOOLS OF ECONOMICS. Classical, Keynesian, & Monetary. as Neo- Classical Supply Side Trickle Down Free Trade CLASSICAL THEORY

SCHOOLS OF ECONOMICS Classical, Keynesian, & Monetary CLASSICAL THEORY Also known as Neo- Classical Supply Side Trickle Down Free Trade 1 FIVE CLASSICAL ECONOMIC BASICS In the long run, competition forces

SCHOOLS OF ECONOMICS Classical, Keynesian, & Monetary CLASSICAL THEORY Also known as Neo- Classical Supply Side Trickle Down Free Trade 1 FIVE CLASSICAL ECONOMIC BASICS In the long run, competition forces

Is the recession over in New York?

By James A. Parrott May 10, 2010 Job numbers are up, unemployment is down. Consumer confidence is up. Gross domestic product has increased for three quarters. It sounds like the is behind us and we re

By James A. Parrott May 10, 2010 Job numbers are up, unemployment is down. Consumer confidence is up. Gross domestic product has increased for three quarters. It sounds like the is behind us and we re

Voices of Immigrant and Muslim Young People

Voices of Immigrant and Muslim Young People I m a Mexican HS student who has been feeling really concerned and sad about the situation this country is currently going through. I m writing this letter because

Voices of Immigrant and Muslim Young People I m a Mexican HS student who has been feeling really concerned and sad about the situation this country is currently going through. I m writing this letter because

JB: And what a tribute to you and everybody who has been involved in it that the effort protects not one coast, but many coasts.

Transcript of Video Interview with Alan Sieroty, recorded 2005. This interview is part of Earth Alert s Heroes of the Coast video archive, featuring interviews with leading California coastal activists,

Transcript of Video Interview with Alan Sieroty, recorded 2005. This interview is part of Earth Alert s Heroes of the Coast video archive, featuring interviews with leading California coastal activists,

What are term limits and why were they started?

What are term limits and why were they started? The top government office of the United States is the presidency. You probably already know that we elect a president every four years. This four-year period

What are term limits and why were they started? The top government office of the United States is the presidency. You probably already know that we elect a president every four years. This four-year period

The Nobel Roundtable. MICHAEL MILKEN: Welcome. Let s start with a. paul bliese

The Nobel Roundtable It s become a tradition for Michael Milken to host a discussion with Nobel Prize winners in economics at the Institute s annual global conference. This year (on April 28) he was joined

The Nobel Roundtable It s become a tradition for Michael Milken to host a discussion with Nobel Prize winners in economics at the Institute s annual global conference. This year (on April 28) he was joined

PLS 103 Lecture 6 1. Today Missouri parties. Last lecture before the exam. We need to start with some

PLS 103 Lecture 6 1 Today Missouri parties. Last lecture before the exam. We need to start with some terms. In order to understand political parties in the United States, in order to understand political

PLS 103 Lecture 6 1 Today Missouri parties. Last lecture before the exam. We need to start with some terms. In order to understand political parties in the United States, in order to understand political

Allan Meltzer and the History of the Federal Reserve. Michael D. Bordo. Rutgers, NBER, and the Hoover Institution, Stanford University

Allan Meltzer and the History of the Federal Reserve Michael D. Bordo Rutgers, NBER, and the Hoover Institution, Stanford University Economics Working Paper 17107 HOOVER INSTITUTION 434 GALVEZ MALL STANFORD

Allan Meltzer and the History of the Federal Reserve Michael D. Bordo Rutgers, NBER, and the Hoover Institution, Stanford University Economics Working Paper 17107 HOOVER INSTITUTION 434 GALVEZ MALL STANFORD

Our American States An NCSL Podcast

Our American States An NCSL Podcast The Our American States podcast produced by the National Conference of State Legislatures is where you hear compelling conversations that tell the story of America s

Our American States An NCSL Podcast The Our American States podcast produced by the National Conference of State Legislatures is where you hear compelling conversations that tell the story of America s

BOSTON COLLEGE Department of Economics. UNCS 2245 Freshman Topic Seminar Fall 2015 Maloney 394

BOSTON COLLEGE Department of Economics UNCS 2245 Freshman Topic Seminar Bob Murphy Fall 2015 Maloney 394 Tuesday 3:00-4:15, Stokes Hall 145N Office Hours: T,Th 1:30-2:30 & by appt. http://www2.bc.edu/robert-murphy

BOSTON COLLEGE Department of Economics UNCS 2245 Freshman Topic Seminar Bob Murphy Fall 2015 Maloney 394 Tuesday 3:00-4:15, Stokes Hall 145N Office Hours: T,Th 1:30-2:30 & by appt. http://www2.bc.edu/robert-murphy

Rates and Inflationary Pressures, Real or Imagined: The Reality of Our Time Working Paper Sent to Chairman Greenspan in July 2000

Rates and Inflationary Pressures, Real or Imagined: The Reality of Our Time Working Paper Sent to Chairman Greenspan in July 2000 Emmanuel Ajuzie Between 1999 and June 2000, some of us watched the activities

Rates and Inflationary Pressures, Real or Imagined: The Reality of Our Time Working Paper Sent to Chairman Greenspan in July 2000 Emmanuel Ajuzie Between 1999 and June 2000, some of us watched the activities

Monetary Dialogue : Looking backward, looking forward

DIRECTORATE GENERAL FOR INTERNAL POLICIES POLICY DEPARTMENT A: ECONOMIC AND SCIENTIFIC POLICY Monetary Dialogue 2009-2014: Looking backward, looking forward NOTE Abstract When comparing the transparency

DIRECTORATE GENERAL FOR INTERNAL POLICIES POLICY DEPARTMENT A: ECONOMIC AND SCIENTIFIC POLICY Monetary Dialogue 2009-2014: Looking backward, looking forward NOTE Abstract When comparing the transparency

The Uneasy Case for Janet Yellen

The Uneasy Case for Janet Yellen John Feldmann August 13, 2013 Until the past couple weeks Janet Yellen has been widely considered the top contender to succeed Ben Bernanke as the Chairman of the Federal

The Uneasy Case for Janet Yellen John Feldmann August 13, 2013 Until the past couple weeks Janet Yellen has been widely considered the top contender to succeed Ben Bernanke as the Chairman of the Federal

Honors General Exam Part 1: Microeconomics (33 points) Harvard University

Harvard University") Honors General Exam Part 1: Microeconomics (33 points) Harvard University April 9, 2014 QUESTION 1. (6 points) The inverse demand function for apples is defined by the equation p = 214 5q, where q is the

Honors General Exam Part 1: Microeconomics (33 points) Harvard University April 9, 2014 QUESTION 1. (6 points) The inverse demand function for apples is defined by the equation p = 214 5q, where q is the

The State of State Legislatures OAS Episode 25 Jan. 10, 2018

The Our American States podcast produced by the National Conference of State Legislatures is where you hear compelling conversations that tell the story of America s state legislatures, the people in them,

The Our American States podcast produced by the National Conference of State Legislatures is where you hear compelling conversations that tell the story of America s state legislatures, the people in them,

The CPI, the Fed, and the Coming Election

The CPI, the Fed, and the Coming Election By Grant Noble June 16, 2004 Initially, the bond and foreign currency market dropped on the headline number of.6% inflation in the CPI. But then they saw the pathetically

The CPI, the Fed, and the Coming Election By Grant Noble June 16, 2004 Initially, the bond and foreign currency market dropped on the headline number of.6% inflation in the CPI. But then they saw the pathetically

APPRAISAL OF THE FAR EAST AND LATIN AMERICAN TEAM REPORTS IN THE WORLD FOREIGN TRADE SETTING

APPRAISAL OF THE FAR EAST AND LATIN AMERICAN TEAM REPORTS IN THE WORLD FOREIGN TRADE SETTING Harry G. Johnson, Professor of Economics University of Chicago Because of the important position of the United

APPRAISAL OF THE FAR EAST AND LATIN AMERICAN TEAM REPORTS IN THE WORLD FOREIGN TRADE SETTING Harry G. Johnson, Professor of Economics University of Chicago Because of the important position of the United

The Tale Behind the Triple Helix: An Interview with Professor Henry Etzkowitz

The Tale Behind the Triple Helix: An Interview with Professor Henry Etzkowitz Tara Iyer Stanford University Professor Henry Etzkowitz is a scholar of international reputation in innovation studies as the

The Tale Behind the Triple Helix: An Interview with Professor Henry Etzkowitz Tara Iyer Stanford University Professor Henry Etzkowitz is a scholar of international reputation in innovation studies as the

In class, we have framed poverty in four different ways: poverty in terms of

Sandra Yu In class, we have framed poverty in four different ways: poverty in terms of deviance, dependence, economic growth and capability, and political disenfranchisement. In this paper, I will focus

Sandra Yu In class, we have framed poverty in four different ways: poverty in terms of deviance, dependence, economic growth and capability, and political disenfranchisement. In this paper, I will focus

CHAPTER 6 REPUBLICAN HYPOCRITES

CHAPTER 6 REPUBLICAN HYPOCRITES Republicans usually go around saying they want less government. That kind of sounds like Libertarians, right? Would Republicans end the war on drugs, end mandatory Social

CHAPTER 6 REPUBLICAN HYPOCRITES Republicans usually go around saying they want less government. That kind of sounds like Libertarians, right? Would Republicans end the war on drugs, end mandatory Social

Interview: Zdeněk Tůma

CENTRAL BANKING PUBLICATIONS LTD Interview: Zdeněk Tůma Governor, Czech National Bank With Martina Horáková Central Banking Publications This article was originally published in: Central Banking Volume

CENTRAL BANKING PUBLICATIONS LTD Interview: Zdeněk Tůma Governor, Czech National Bank With Martina Horáková Central Banking Publications This article was originally published in: Central Banking Volume

TRUSTEESHIP OF COMMON WEALTH. Lecture by Peter Barnes Social Wealth Forum, University of Massachusetts, Amherst April 6, 2006

TRUSTEESHIP OF COMMON WEALTH Lecture by Peter Barnes Social Wealth Forum, University of Massachusetts, Amherst April 6, 2006 Let me start by putting out a formula that underlies my thinking: Corporations

TRUSTEESHIP OF COMMON WEALTH Lecture by Peter Barnes Social Wealth Forum, University of Massachusetts, Amherst April 6, 2006 Let me start by putting out a formula that underlies my thinking: Corporations

University of California, Berkeley ECONOMICS 210C / ECONOMICS 236A MONETARY HISTORY SYLLABUS PART I: THE EFFECTS OF POLICY

Fall 2006 University of California, Berkeley Christina Romer David Romer ECONOMICS 210C / ECONOMICS 236A MONETARY HISTORY SYLLABUS PART I: THE EFFECTS OF POLICY August 30 The Identification Problem in

Fall 2006 University of California, Berkeley Christina Romer David Romer ECONOMICS 210C / ECONOMICS 236A MONETARY HISTORY SYLLABUS PART I: THE EFFECTS OF POLICY August 30 The Identification Problem in

Our American States An NCSL Podcast

Our American States An NCSL Podcast The Our American States podcast produced by the National Conference of State Legislatures is where you hear compelling conversations that tell the story of America s

Our American States An NCSL Podcast The Our American States podcast produced by the National Conference of State Legislatures is where you hear compelling conversations that tell the story of America s

Speech to SOLACE National Elections Conference 16 January 2014 Peter Wardle

Opening remarks Thank you. Speech to SOLACE National Elections Conference 16 January 2014 Peter Wardle It s good to have the chance to speak to the SOLACE Elections Conference again. I will focus today

Opening remarks Thank you. Speech to SOLACE National Elections Conference 16 January 2014 Peter Wardle It s good to have the chance to speak to the SOLACE Elections Conference again. I will focus today

Oral History Program Series: Civil Service Interview no.: O5

An initiative of the National Academy of Public Administration, and the Woodrow Wilson School of Public and International Affairs and the Bobst Center for Peace and Justice, Princeton University Oral History

An initiative of the National Academy of Public Administration, and the Woodrow Wilson School of Public and International Affairs and the Bobst Center for Peace and Justice, Princeton University Oral History

The Benefits of Enhanced Transparency for the Effectiveness of Monetary and Financial Policies. Carl E. Walsh *

The Benefits of Enhanced Transparency for the Effectiveness of Monetary and Financial Policies Carl E. Walsh * The topic of this first panel is The benefits of enhanced transparency for the effectiveness

The Benefits of Enhanced Transparency for the Effectiveness of Monetary and Financial Policies Carl E. Walsh * The topic of this first panel is The benefits of enhanced transparency for the effectiveness

I would like to add my voice to the chorus in thanking President Fisher and the

Policymaker Roundtable Federal Reserve Bank of Dallas Conference: "John Taylor's Contributions to Monetary Theory and Policy" By Janet L. Yellen, President and CEO, Federal Reserve Bank of San Francisco

Policymaker Roundtable Federal Reserve Bank of Dallas Conference: "John Taylor's Contributions to Monetary Theory and Policy" By Janet L. Yellen, President and CEO, Federal Reserve Bank of San Francisco

THE WOODROW WILSON SCHOOL OF PUBLIC AND INTERNATIONAL AFFAIRS AND THE BOBST CENTER FOR PEACE AND JUSTICE

AN INITIATIVE OF THE WOODROW WILSON SCHOOL OF PUBLIC AND INTERNATIONAL AFFAIRS AND THE BOBST CENTER FOR PEACE AND JUSTICE Series: Interview no.: Civil Service S8 Interviewee: Interviewer: Fabien Majoro

AN INITIATIVE OF THE WOODROW WILSON SCHOOL OF PUBLIC AND INTERNATIONAL AFFAIRS AND THE BOBST CENTER FOR PEACE AND JUSTICE Series: Interview no.: Civil Service S8 Interviewee: Interviewer: Fabien Majoro

Presidents and The US Economy: An Econometric Exploration. Working Paper July 2014

Presidents and The US Economy: An Econometric Exploration Working Paper 20324 July 2014 Introduction An extensive and well-known body of scholarly research documents and explores the fact that macroeconomic

Presidents and The US Economy: An Econometric Exploration Working Paper 20324 July 2014 Introduction An extensive and well-known body of scholarly research documents and explores the fact that macroeconomic

Portland State University Department of Economics

Portland State University Department of Economics Syllabus 1 (Spring 2013) Course No.: EC 582 Course Title: Advanced Macroeconomics Credits: 4 Section No.: 001 Class Hours: MW 4:40-6:30 pm CRN: 60974 Instructor:

Portland State University Department of Economics Syllabus 1 (Spring 2013) Course No.: EC 582 Course Title: Advanced Macroeconomics Credits: 4 Section No.: 001 Class Hours: MW 4:40-6:30 pm CRN: 60974 Instructor:

The George Washington University Law School

The George Washington University Law School Access to the Media 1967 to 2007 and Beyond: A Symposium Honoring Jerome A. Barron s Path-Breaking Article Introductory Remarks by The Honorable Stephen G. Breyer

The George Washington University Law School Access to the Media 1967 to 2007 and Beyond: A Symposium Honoring Jerome A. Barron s Path-Breaking Article Introductory Remarks by The Honorable Stephen G. Breyer

Frances Kunreuther. To be clear about what I mean by this, I plan to cover four areas:

In preparation for the 2007 Minnesota Legislative Session, the Minnesota Council of Nonprofit s Policy Day brought together nonprofit leaders and advocates to understand actions that organizations can

In preparation for the 2007 Minnesota Legislative Session, the Minnesota Council of Nonprofit s Policy Day brought together nonprofit leaders and advocates to understand actions that organizations can

Elections and Obama's Foreign Policy

Page 1 of 5 Published on STRATFOR (http://www.stratfor.com) Home > Elections and Obama's Foreign Policy Choices Elections and Obama's Foreign Policy Choices Created Sep 14 2010-03:56 By George Friedman

Page 1 of 5 Published on STRATFOR (http://www.stratfor.com) Home > Elections and Obama's Foreign Policy Choices Elections and Obama's Foreign Policy Choices Created Sep 14 2010-03:56 By George Friedman

ALTERNATIVES TO ADJUDICATION. Toby Randle. 9 May 2005 THE SAVOY HOTEL, LONDON

ALTERNATIVES TO ADJUDICATION 11 TH ADJUDICATION UPDATE SEMINAR Toby Randle 9 May 2005 THE SAVOY HOTEL, LONDON Here I am, at the 11 th Fenwick Elliott adjudication seminar, in a room full of people closely

ALTERNATIVES TO ADJUDICATION 11 TH ADJUDICATION UPDATE SEMINAR Toby Randle 9 May 2005 THE SAVOY HOTEL, LONDON Here I am, at the 11 th Fenwick Elliott adjudication seminar, in a room full of people closely

[Slide 26 displays the text] Jurisdiction and Other Limits on Judicial Authority

![[Slide 26 displays the text] Jurisdiction and Other Limits on Judicial Authority](/thumbs/82/85841498.jpg "[Slide 26 displays the text] Jurisdiction and Other Limits on Judicial Authority") [Slide 26 displays the text] Jurisdiction and Other Limits on Judicial Authority [Narrator] Now in this part of module one, we ll be talking a little bit about the concept of jurisdiction, and also other

[Slide 26 displays the text] Jurisdiction and Other Limits on Judicial Authority [Narrator] Now in this part of module one, we ll be talking a little bit about the concept of jurisdiction, and also other

The best books on Globalization

FIVEBOOKS.COM 20 FEBBRAIO 2017 The best books on Globalization Intervista a Larry Summers - di Eve Gerber Globalization benefits mankind and we are learning how better to deal with the disruption it causes.

FIVEBOOKS.COM 20 FEBBRAIO 2017 The best books on Globalization Intervista a Larry Summers - di Eve Gerber Globalization benefits mankind and we are learning how better to deal with the disruption it causes.

Adam Smith and Government Intervention in the Economy Sima Siami-Namini Graduate Research Assistant and Ph.D. Student Texas Tech University