2017 EU Gulf Cooperation Council Investment Report

|

|

|

- Lynne Garrett

- 5 years ago

- Views:

Transcription

1 SERVICE FOR FOREIGN POLICY INSTRUMENTS/POLICY SUPPORT FACILITY FWC FPI/PSF/ LOT 4: MARKET ACCESS AND TRADE & INVESTMENT AGREEMENT NEGOTIATION & IMPLEMENTATION- Multiple FWC CRIS number 2016/ SERVICE FOR FOREIGN POLICY INSTRUMENTS/POLICY SUPPORT FACILITY 2017 EU Gulf Cooperation Council Investment Report A project implemented by Eurosupport Consortium - AESA i

2 Multiple Framework Contract FWC FPI PSF 2015 Lot 4: Market Access and Trade & Investment Agreement Negotiation & Implementation Request for Service 2016/ Version 1 July 2017 This report was prepared with financial assistance from the European Commission. The views expressed are those of the consultant and do not necessarily represent any official view of the Commission or the Government of this Country ii

3 Executive Summary This report aims to inform companies situated in the European Union (EU) that may be considering Foreign Direct Investment (FDI) in one of the six Gulf Cooperation Council (GCC) countries. The report provides a survey of the current FDI landscape and assesses the possible impact of the recent reform agendas on the regulatory framework for FDI. It finally draws conclusions which could inform further investment related policies in the GCC countries and their cooperation with the EU. A key conclusion resulting from the survey and the assessment of the regulatory frameworks is that the GCC countries long-term visions and development plans are crucial in attracting inward FDI. These plans accordingly meet a core priority of the EU companies interviewed, namely to increase the GCC region s overall economic growth rate and market size. Diversification of the region s economic structure is instrumental in this respect. However, attaining the strategies individual goals is often seen as a protracted process. This is, among else, the result of a lengthy decision-making process, ad hoc implementation and, not least, of reversing reforms. The stakeholders interviewed for this report argued that there is a gap between the announcement of reforms and their actual implementation, resulting in a barrier to FDI. Similarly, significant alterations of the content of the announced reforms will have a slowing effect on FDI. The respondents believe that reforms have been formulated primarily in response to the falling oil price. Hence, they fear that if the fiscal crisis is averted, the reform agenda will risk losing momentum. This report points to four areas that are of the biggest concern to existing investors. 1) The ability to collect payments and repatriate capital; 2) The regulatory framework/permit system; 3) The effectiveness of the government bureaucracy; 4) The availability of skilled labour. These currently constitute the principal barriers to inward FDI in the GCC countries. The survey section explains the concerns of EU companies and the conclusions offer specific recommendations on how these could be addressed. In addition, this report recommends closer inclusion of the private sector in the development and implementation of FDI reforms. A feature that could be achieved by establishing a consultative mechanism that would allow policy makers to capture and incorporate the companies concerns and suggestions during the reform process. A regular and structured process for following up on issues identified during and after implementation 1

4 would equally increase the impact of the reforms and allow companies to make longer-term investments. As far as intergovernmental investment protection is concerned, the existence of bilateral investment treaties (BITs) does not appear to have been decisive to the EU companies investment decisions. This feedback, in combination with a review of the academic literature on the topic, suggests that increased cooperation on codified investment protection, based on the current type of BITs, is not a key priority for investors. This report therefore recommends prioritising the factors mentioned in the survey by the investors or changing the approach to BITs. The main sources for this study are official FDI data, official documents regarding the regulatory frameworks, national development visions/reform plans and a survey of 50 EU companies operating in the GCC countries. These sources are complemented by analyst reports and interviews with regional and local experts as well as officials from the EU Commission and Member States Qatar Diplomatic Crisis In June 2017, the Kingdom of Saudi Arabia (KSA) and the United Arab Emirates (UAE) together with several other nations including Bahrain, cut all diplomatic ties with Qatar. The measures included closing all borders and halting land, air, and sea traffic with the country. These events unfolded as the present study was being concluded and an evaluation of the impact was not undertaken. 2

5 Table of Contents Executive Summary... 1 Acronyms... 4 Data Collection Methodology... 5 Survey approach... 7 Introduction... 8 GCC economic outlook... 9 FDI inflows in the GCC region, Section 1: Company Survey Background information on the companies surveyed EU origin country overview Company types / Size of turnover GCC Country of Activity Size of investment made in the GCC region Assessment of the ease of starting a business in the GCC region Starting a business Fair and equal treatment Restrictions on foreign ownership Real estate rules which provide fair and equal treatment for foreign and domestic companies Local courts Assessment of factors influencing investment decisions in the GCC region Individual elements most often mentioned as negatively or positively affecting investment decisions Insights on individual factors Section 2: Regional Analysis Comparison of FDI-related legislation across GCC countries, including EU companies views Foreign ownership Business structures Customs duty Labour Real estate Anti-bribery and corruption Cross-cutting findings on the regulatory framework in the GCC region for EU FDI. 40 1

6 Future trends and opportunities for the FDI reform process Section 3: GCC Country Profiles Bahrain A brief introduction to the economy of Bahrain Economic Vision National Development Strategy FDI inflows to Bahrain Reform of FDI laws and identification of key players Brief assessment Bilateral Investment Treaties Kuwait A brief introduction to the economy of Kuwait New Kuwait 2035 plan Development Plan FDI inflows to Kuwait Reform of FDI-related laws and identification of key players Brief assessment Bilateral Investment Treaties Oman A brief introduction to the economy of Oman Oman s Vision th Five-Year Development Plan FDI inflows to Oman Reform of FDI laws and identification of key players Brief assessment Bilateral Investment Treaties Qatar A brief introduction to the economy of Qatar Qatar National Vision National Development Strategy FDI inflows to Qatar Reform of FDI laws and identification of key players Brief assessment Saudi Arabia A brief introduction to the economy of Saudi Arabia Saudi Arabia Vision

7 Transformation Programme FDI inflows to Saudi Arabia Reform of FDI laws and identification of key players Brief assessment Bilateral Investment Treaties United Arab Emirates A brief introduction to the economy of the United Arab Emirates Vision The National Agenda FDI inflows to UAE Reform of FDI laws and identification of key players Brief assessment Section 4: EU - GCC Investment Protection Cooperation State of play on the bilateral investment protection agreements of EU Member States with the GCC countries Brief introduction to BITs State of play of BITs in the GCC Assessment of key benefits Assessment of potential impact of further investment protection cooperation with individual GCC partners Do BITs promote FDI? Impact of further investment protection Section 5: Conclusion and Main Recommendations Bibliography

8 Acronyms BIC BIT BLEU CBB CBK EDB EEN EU FDI FTA GCC GCC-STAT GDP GRE GSO ICT ICSID IIA IMF ISC ISDS KDIPA KSA LNG OECD OPEC SAGIA SAMA SME SPE UAE UN UNCTAD VAT Bahrain Investors Center Bilateral Investment Treaty Belgium - Luxembourg Economic Union Central Bank of Bahrain Central Bank of Kuwait Economic Development Board Enterprise Europe Network European Union Foreign Direct Investment Free Trade Agreement Gulf Cooperation Council GCC Statistical Center Gross Domestic Product Government Related Entities GCC Standardization Organization Information and Communication Technology International Centre for Settlement of Investment Disputes International Investment Agreements International Monetary Fund Investment Services Center (Saudi Arabia) Investor-state dispute settlement Kuwait Direct Investment Promotion Authority Kingdom of Saudi Arabia Liquefied Natural Gas Organization for Economic Co-operation and Development Organization of the Petroleum Exporting Countries Saudi Arabian General Investment Authority Saudi Arabia Monetary Agency Small and Medium-sized Enterprises Special Purpose Entities United Arab Emirates United Nations United Nations Conference on Trade and Development Value Added Tax 4

9 Data Collection Methodology FDI Definition This report s point of departure is the United Nations Conference on Trade and Development s (UNCTAD) definition of FDI as an investment involving a long-term relationship and reflecting a lasting interest and control by a resident entity in one economy (foreign direct investor or parent enterprise) in an enterprise resident in an economy other than that of the foreign direct investor (FDI enterprise or affiliate enterprise or foreign affiliate). 1 Therefore, FDI implies that the investor exerts a significant degree of influence on the management of the enterprise residing in another economy. The investor's interest is usually considered to be lasting when the investor owns at least 10% of the company s voting power. 2 A general challenge analysing FDI in the GCC countries is represented by the lack of consistent, up-to-date and comparable statistical data that allows for in-depth analysis, trend description and cross-sectional comparison. To achieve consistency and reliability, this report uses data drawn mainly from UNCTAD s international datasets and statistics, namely UNCTAD STAT and UNCTAD FDI Statistics. UNCTAD regularly collects official, published and unpublished FDI data flows, directly from central banks, statistical offices or national authorities on an aggregated and disaggregated basis for its FDI/MNE database. These data sets constitute the main source for the reported FDI data. 3 For the total inflow of FDI into each country, UNCTAD STAT was the primary database. For the breakdown of FDI flows by investor country to each GCC country, data from UNCTAD FDI Statistics (FDI/MNC Database) was the primary source. UNCTAD s Investment Trends and Data Section was contacted for the most recent data on such bilateral FDI flows, but for most countries UNCTAD FDI Statistics only contains data up to 2012, and in some cases only up to In the case of Oman, Qatar, the KSA and the UAE, the data is based on information provided by national authorities such as central banks and investment agencies. As for Bahrain and Kuwait, data from UNCTAD FDI Statistics is based on official information reported by the 1 UNCTAD notes that This general definition of FDI is based on OECD, Detailed Benchmark Definition of Foreign Direct Investment, third edition (OECD 1996) and International Monetary Fund, Balance of Payments Manual, fifth edition (IMF 1993) and Balance of Payments and International Investment Position Manual, sixth edition (IMF 2009). 2 FDI involves both the initial transaction between the two entities and all subsequent transactions between them and among foreign affiliates. It covers equity capital, reinvested earnings and intracompany loans. 3 This decision was made after comparing UNCTAD s FDI data with other sources, including other international organisations and national statistics in the individual GCC countries. These examinations confirmed that UNCTAD s datasets cover the most countries in the GCC over the longest period of time and therefore allow for the most relevant comparisons. Yet, this study also draws on other economic data, estimates and analysis published by the International Monetary Fund (IMF), the World Bank and the Organization for Economic Co-operation and Development (OECD), among others, as indicated in the respective footnotes throughout. 5

10 countries sending FDI to Bahrain and Kuwait. For these reasons, data from UNCTAD FDI Statistics may differ from UNCTAD STAT s data. UNCTAD FDI Statistics is solely used for indicating if FDI was made by an investor from an EU Member State after a BIT s entry into force. UNCTAD methodology Following UNCTAD s methodology on data gathering and analysis, two important factors must be taken into consideration about the data used in this study: First, this study mainly relies on data on a directional basis as opposed to data on an asset/liability basis. The former refers to FDI flows organised according to the direction of the investment in the reporting economy either inward or outward. Data based on the directional principle allows this study to analyse FDI in the context of parent-affiliate methodology. In other words, data on a directional basis can indicate the flows of FDI specifically originated from EU countries entering the GCC economies. However, UNCTAD STAT s data on the flows of FDI to Oman since 2000 are only available on the asset/liability basis. Second, when possible, UNCTAD removes investment flows originated by resident special purpose entities (SPEs) that have little or no employment or operations or physical presence in the jurisdiction of the GCC countries. Such SPEs are often used as vehicles to raise capital or to hold assets and liabilities and usually do not undertake significant production. This approach provides a more meaningful measure of an economies FDI by removing FDI that involves funds passing through an SPE on their way to another destination (outward FDI) and those coming to the country through other economies SPE (inward FDI). Therefore, the data presented in this study may differ from data in different datasets. For data on GDP annual growth, UNCTAD STAT is the main source. Data on government budget and government debt as a percentage of GDP is from the Trading Economics website. Trading Economics data is based on official sources and fiscal information published by the economic authorities from each GCC country. Trading Economics data on government debt as a percentage of GDP was chosen over the World Bank data since it covers the entire historical series for almost all GCC countries. The exception is Oman, for which the 2016 data on the government debt as a percentage of GDP and government budget is missing. For the state of play of BITs between EU Member States and GCC countries, UNCTAD Policy Hub was the main source. To avoid double counting, terminated agreements were not counted, especially since such agreements were, at times, replaced with the signature of a new BIT that is currently in force. The information on the status of signed BITs was last updated in August 2017 and therefore will not cover BITs that enter into force after this date. 6

11 Finally, data for the summary statistics in the country profiles (population, population density, surface area, etc.) comes from the UN data website. Data from the GCC Statistical Center (GCC-STAT) was occasionally used for comparative purposes. Certain GCC countries such as UAE have not had a census in the past several years, thus numbers are estimates and can vary significantly by source. For that reason, a single source was used in all country profiles to maintain a consistent methodology. Survey approach The survey is an update of the survey among EU companies from the 2013 EU-GCC Investment Report. The survey investigates the ease of starting and operating a business in the region as well as the incentives and barriers to FDI. The 50 companies interviewed are all based in the EU and currently investing in or strongly considering investing in the GCC region. The interviews were conducted between early March and mid-june They were performed over the phone in English, Danish, Arabic and French and lasted on average minutes. All interviews were guided by a questionnaire with predefined questions to ensure a proper sequencing of issues raised. The interviewees were selected using purposeful sampling to give more weight to EU countries with large FDI stocks in the GCC (i.e. Germany, France and the UK) and to GCC countries with the largest FDI stocks overall (i.e. the KSA and the UAE). 4 In addition, per the EU Commission's recommendation, the following sectors were targeted: energy, transport, construction, pharmaceuticals, food and agricultural products. The questionnaire contained 51 questions divided into three main sections. The first section collected general information about the EU companies and their GCC activity; the second assessed each company s opinion on the ease of starting a business and operating in the GCC region; the third investigated the respondents future investments in the region with a focus on the relevance of the different factors influencing investment decisions. There were some limitations in the answers of the survey. Respondents had the option to skip any non-relevant questions, abstaining for example from sharing financial information about the company and focusing mainly on issues related to their area of expertise. In section two, the skipped questions were counted as I don t know answers. The same was not possible for section three, due to the absence of an I don t know option - instead the participants could indicate that a factor had no impact on their investment decisions. 4 A perfect representation was however not achieved, see Section 1: Company Survey 7

12 Introduction Over the past decade, the GCC economies have experienced large macroeconomic instability caused by the fluctuating oil price and the aftermath of the global financial crisis. These factors have especially impacted public finances and FDI inflows, which for all countries except UAE are at a lower level than a decade ago. In response, GCC governments have put forth a set of reforms to boost economic growth and attract FDI. The reforms seek to increase private sector participation in the GCC economies, reduce dependence on hydrocarbons and reduce the employment responsibility of the public sector. Indeed, several GCC countries have introduced amendments to investment laws and created investment promotion agencies to support incoming foreign companies. This report examines the impact of these reforms on EU companies and the extent to which they have influenced EU companies decisions vis-à-vis investing or expanding their businesses in the GCC countries. The report also looks at possible future reforms that could impact their investment decisions: Section 1 outlines the main findings of the survey conducted for this report of 50 EU companies investing or strongly considering investing in the GCC region. The survey examines which factors are the most important in shaping their investment decisions. Section 2 provides a comparison of FDI-related legislation across the GCC region, as well as an assessment of the FDI regulatory framework in the GCC. Section 3 explores the FDI environment on a country-by-country basis with a focus on the reforms of FDI laws, key players shaping the landscape and the signature of BITs with EU countries. Section 4 takes a consolidated view of the state of play of BITs with EU Member States and assesses their benefits to key stakeholders as well as the potential for further investment protection cooperation with GCC partners. Section 5 highlights the main conclusions of this study and provides recommendations for further engagement and dialogue between stakeholders. 8

13 GCC economic outlook The economic growth is expected to remain weak in the GCC region. Hence, fiscal and external balances continue to deteriorate 5. The IMF accordingly estimates that the GDP of the GCC economies grew by 1.7% in 2016 and forecasts an average 2.3% GDP growth in 2017, 6 far from the growth experienced in the past. 7 As a result, GCC governments have been cutting their spending, introducing taxation schemes, and releasing debt through bond issuances. Nevertheless, GCC policymakers will continue to face a challenging environment with sustained low oil prices, leading to fiscal deficits that are expected to remain substantial in both the short and medium term. This could threaten the fiscal sustainability of the GCC countries, yet debt levels remain relatively low from an international perspective and current oil prices are still above the GCC countries break-even points. GDP growth and aggregated debt GDP Growth (YoY %) GCC Aggregated Debt (% of GDP) Aggregated Debt GDP growth Source: UNCTAD STAT & Trading Economics (based on data from GCC governments) 5 IMF (2016). Economic Prospects and Policy Challenges for the GCC Countries. P.7. Available at: 6 The estimates were published before the Qatari crisis. 7 IMF (2016). Diversifying Government Revenue in the GCC: Next Steps. Available at: 9

14 FDI inflows in the GCC region, FDI inflows (million USD, current prices) * % Bahrain % Kuwait -6** ** Oman % Qatar % Saudi Arabia % United Arab Emirates % Total % Source: UNCTAD STAT database * Data is subjected to changes once the UNCTAD STAT database is updated ** No percentage change is calculated since the base year is negative (net FDI outflow) Source: UNCTAD STAT database FDI inflows to to GCC GCC countries, (USD Billion) From 2008 to 2016, FDI inflows to the GCC have decreased by 63% to just below USD 20 billion. As mentioned, the GCC countries have introduced several measures of fiscal consolidation and institutional reform to secure long-term economic sustainability while contributing to regional private sector development. Such measures aim to boost investor and market confidence in the GCC economies, leading to a virtuous cycle of higher investment, including FDI, and output growth in the near term. 8 These reforms will be analysed separately in the country profiles. 8 World Bank (2017). New Report Projects Modest Growth in GCC with Increased Activity in the Non- Oil Sector. Available at: 10

15 Section 1: Company Survey Background information on the companies surveyed EU origin country overview The survey undertaken covered representatives from 15 EU Member States and emphasized the three biggest holders of FDI stock, namely Germany, France and the UK. As seen, Denmark is over-represented in the survey. This was due to the time limitation on collecting responses, the origin of the report authors and convenient access to the Danish investors and companies through pre-existing networks. More companies were contacted in order to achieve a representation that more closely reflected the composition of EU Members State FDI stocks in the GCC. However, due to time constraints and a lack of responses, it proved impossible to achieve a perfect representation. Nevertheless, the top four EU Member States, in terms of inward FDI to the GCC in recent years, are also in the top five for number of respondents in this survey. The authors found that the responses from the Danish companies were broadly in line with the responses from the larger FDI exporters in the EU. However, it is inevitable that the overall analysis will be skewed slightly toward the concerns of smaller FDI exporters. 11

16 Company types / Size of turnover GCC Country of Activity Most of the surveyed businesses were large corporations. This could indicate that undertaking FDI in the GCC region requires large financial muscle. However, it may also be a result of the fact that large corporations are easier to identify as investors in the GCC region and have more human resources to respond to surveys. Most of the companies were active in the two biggest GCC markets and destinations for FDI, namely the KSA and the UAE. Furthermore, almost half of the companies were active across the GCC region. This once again indicates that the sample is mainly comprised of large corporations having activities in multiple GCC countries. Size of investment made in the GCC region 12

17 Interestingly, the size of the companies investments in the GCC region is relatively modest compared to their global turnover. This reflects the fact that several of the companies surveyed have chosen to establish consulting or sales offices instead of production and/or distribution points. This choice of entry mode only requires a limited investment. Typically, this choice of entry mode is made because the market size does not justify a full-scale production set-up (see assessment of factors influencing investment decisions in the GCC region). Another possible cause of modest investments in the region could be the companies need of great liquidity and little dependence on the income in the GCC region due to delayed payments (or non-payments). A number of companies that have been active in the GCC region for many years formally work under the umbrella of a local partner - either in a joint venture or with a single salesperson. This explains the large share of investments under EUR 2 million that fall under the other category. A number of large engineering and construction companies have equally established their presence in the GCC region in the form of consulting offices, providing expertise on infrastructure projects in partnership with local companies. Most of these companies also have small field offices next to the construction sites which are also categorised as other. These offices do have some administrative functions but do not carry out typical functions such as formal representation and sales. 13

18 Assessment of the ease of starting a business in the GCC region Starting a business Please rate the ease of starting a business in the GCC country (ies) where your company operates A small majority of the interviewed companies that had an opinion on this question found the process of starting a business in the GCC region simple and transparent. The interviewees report that the creation of investment agencies and the possibility of doing most procedures online are important advancements that facilitate the process of setting up a business. However, almost half of the interviewed companies that had an opinion on this question stress that it is difficult and time-consuming to start a business in the GCC region. This group of respondents state that starting a business in the GCC without a local partner makes the process more difficult. This also applies in those instances where 100% foreign ownership is allowed. According to this group, having a local partner can help in overcoming bureaucratic procedures. They believe that cultural fit and good connections make a positive difference when applying for permits in most of the GCC countries. While the creation of investment promotion agencies and online services for incoming companies is considered a relevant advancement, the interviewees argue that conflicting or incomplete information remains a challenge. The ease of starting a business in the GCC countries varies by sector of activity. In general, service providers and companies in the construction sector find it more difficult and 14

19 time-consuming to start a business in the region, whereas companies in the clean energy, oil and gas sectors find it easier. Engineering companies opening consulting offices in the region report long delays obtaining permits and sometimes experience conflicting information concerning the documentation required. Companies operating in strategic sectors such as oil & gas, clean energy and in defence report that they receive substantial support from local authorities. Also, oil companies mostly operate in joint ventures with national oil companies that facilitate their start-up. Among companies operating in sectors categorised as others, those in Information and Communication Technology (ICT) and transport and logistics rate the process as difficult and time-consuming, while companies in the defence and pharma sectors mostly rate it as easy and transparent. 15

20 Fair and equal treatment When doing business in the GCC country (ies) where your company operates: is there equal treatment to foreign and domestic investors? The respondents are split down the middle as to whether they believe that there is equal treatment in the GCC region for foreign and domestic companies. As seen in the second chart, interviewees answers to this question differ by sector. Most of the companies that operate in the agriculture, manufacturing and service sectors believe that foreign and domestic companies are treated equally in the GCC countries where they operate. The companies operating in the construction and oil & gas sectors, on the contrary, believe that there is no equal treatment for foreign and domestic companies. Under the others category, the majority of the engineering and defence companies argue that there is no equal treatment for foreign and domestic companies. It is important to note that for companies in the sectors of engineering, oil & gas and defence, lack of equal treatment means that they are generally still treated better than foreign companies are in other sectors. As an example hereof, some highly specialised engineering 16

21 companies receive preferential treatment. The latter for instance translates into more flexible requirements with respect to the ratio of expat workers allowed in a given company. Nonetheless, companies in the construction sector point out that the likelihood of winning contracts in most GCC countries is very limited without a local partner. The preference for local companies is particularly noticeable when government procurement prioritises companies that have local content. At the same time, interviewees working for EU companies that rely on a local supply chain to drive up local content argue that this strategy increases their costs and lowers their competitiveness. The EU companies therefore must balance increasing local content without eroding their competitiveness. Restrictions on foreign ownership Are there restrictions to foreign ownership in your sector? The majority of the companies interviewed had the option to operate with 100% foreign ownership in their sector. Some of the interviewees, who answered No to this question, argue that challenges of operating without a local partner can be considered a barrier to foreign ownership. GCC countries are increasingly allowing 100% foreign ownership. However, a local partner is still considered a tactical advantage to mitigate the risk of having to navigate systems considered opaque and complex to obtain a permit. It can also result in a higher likelihood of winning tenders. Nevertheless, interviewees stress the risk of delays in the transfer of funds from the local joint venture partner. In light of this, several interviewees advise incoming companies to carefully consider the need for a local partner. Hence, in the case that the local partner solely contributes an ability to navigate the local bureaucracy, the foreign company is advised to seek the assistance of a consulting company. 17

22 Real estate rules which provide fair and equal treatment for foreign and domestic companies Are there clear real estate rules which provide fair and equal treatment for foreign and domestic companies? The large majority of the respondents are not aware whether the countries in which they operate have real estate rules that provide fair and equal treatment for foreign and domestic companies. Certain companies operating in the construction sector are aware of limits to acquire, develop and sell real estate in the UAE and the KSA. Yet, this is not seen as a barrier to investment. Local courts Do you find local courts supportive of arbitration proceedings and enforcement of arbitration awards? Most interviewees did not know the answer to this question or chose not to answer. Hence, taken literally, this assumes that most of the interviewed companies have never been engaged in legal court proceedings in the region. 18

23 Among those that answered, 54% find the process slow and cumbersome and the remaining 46% find it good and efficient. Given that several companies are operating in more than one GCC country, the results incorporate variation found across the region. Regarding the lack of trust in legal courts, some respondents have explained that the likelihood of a foreign company winning court cases against local governments or large companies owned by family groups or well-known family companies is very low. Companies operating in smaller GCC economies report that resorting to the court system would negatively affect their reputation in the country of operation. This would, in other words, make it very difficult for them to do business in those markets. Companies located in the UAE and Bahrain report that signing agreements designating international courts of arbitration is a common practice when doing business in those countries. Still, companies that won disputes in international courts experienced challenges claiming their compensation at the local level. Assessment of factors influencing investment decisions in the GCC region Prior to the interview, a list of factors influencing investment decisions in the GCC region was sent to the participants via . During the interview, participants were asked to rank the top five factors influencing their investment decisions in the GCC countries. In some cases, participants opted to rank less than five factors. Based on the respondents answer, the survey software generated a final rank of factors influencing investment decisions in the GCC region (cf. below). 19

24 For each factor, follow-up questions identified the most relevant elements. Based on respondents answers, the pre-defined elements were ranked as having one of the following influence levels on investment decisions: strongly positive ; positive ; no effect ; negative or strongly negative (cf. questionnaire in appendix). If the pre-defined elements were irrelevant to the participant s decision-making, interviewees were encouraged to comment on the other elements that played an important role in their investment decisions. This explains why some charts with fewer data entries rank higher on companies assessments and why elements under the same factor have different amounts of data entries. In such cases, the companies comments will indicate the actual concerns influencing their investment decisions vis-à-vis each factor. To avoid misinterpretation, the percentage comparisons in this section will compare the number of data entries for each element with the entire survey population. 20

25 Individual elements most often mentioned as negatively or positively affecting investment decisions The below figures show that the four most negative individual elements influencing interviewees decisions to invest in the GCC region are the late and/or non-payment of invoices; the time required to register a business; the amount of information available on bureaucratic procedures and; the obligation to employ a minimum quota of nationals. Late and/or non-payment of invoices 9 18 Time of registration procedure to start a business 10 7 Amount of information available on bureaucratic procedures 4 13 Obligation to employ a certain amount of domestic employees 6 9 Strongly adverse Adverse The late payment of invoices was the most adverse element found in this survey. However, the time of registration procedure to start a business was rated more negatively, graded as strongly adverse by 20% of all interview respondents. 21

26 Market size and growth rate Efficient communication networks 2 13 The most positive individual elements influencing investment decisions in the GCC region are Accessible airports and ports 4 9 Market size and growth rate Access to neighbouring countries Efficient communication networks Accessible airports and ports 4 9 Access to neighbouring countries 8 7 Strongly positive Positive the size of the markets and growth rate; the infrastructure, e.g. communication networks, accessible airports and ports; and the access to neighbouring countries. Market size was mentioned by 64% and market growth was mentioned by 62% of the respondents. Strongly positive Positive Insights on individual factors Economic outlook The economic outlook of the GCC countries ranked as the most influential factor that affects the decision to invest in the region. The most relevant elements with respect to this factor are market size and growth rate; both have a positive or strongly positive effect on investment decisions. The existence of industry clusters and the presence of competitors were mostly ranked as less relevant. However, respondents mention industry clusters as a positive factor for certain companies operating in logistics, transportation, or highly specialised services. 22

27 Recent government investments in infrastructure, tourism, and communications positively impacted companies perceptions of the region s economic potential. However, the impact of fluctuating oil prices on government spending remains a concern. At the same time, EU companies in the GCC region identify an opportunity to fill the gaps that exist with respect to technical expertise in areas such as engineering and technology. Interviewees highlight that local contractor s trust and value European expertise in technical areas. This allows EU companies to operate with higher fees and in some cases employ a higher number of expats. Ability to collect payments and repatriate capital The late payment and non-payment of invoices represent the primary concern vis-à-vis this factor. The late payment of invoices was mentioned as having either strongly adverse or adverse influence on investment decisions by 50% of the interviewed participants. Similarly, the non-payment of invoices was indicated as having strongly adverse or adverse effects on investment decisions by 44% of all respondents. Although fewer interviewees have experienced non-payment of invoices, delays in payments is perceived as a common practice in the region. Several interviewees highlight that companies should not expect payments to occur unless these had been previously secured through advanced payments or letters of credit. Engineering companies report that government-procured projects must be completed despite payment delays: hence, it is necessary to have a strong financial base to operate in the region. However, companies in the defence industry or engineering companies working on strategic infrastructure projects report fewer and shorter delays on the payments of invoices. 23

28 Regulatory framework and permits system Among the factors related to the regulatory framework and permits system, only the requirement to a certain percentage of domestic content had a major influence on investment decisions. The requirement for a local partner was mentioned as either a strongly adverse or adverse factor by 20% of all interview participants. The companies responses indicate that governments low predictability and the fast pace of regulatory changes in the GCC region - as opposed to any specific law or requirement - are a major concern. The rapidly changing regulatory frameworks in the GCC countries make it difficult for businesses to adapt. EU companies argue that there is no inclusive dialogue on the regulatory reform agenda and local governments do not consult businesses before issuing new regulations nor do they give them proper time to adapt. This is a major challenge in the ICT sector, where the lack of information on changes in the regulatory framework leads to conflicts between sellers and end-users. For companies in the food and electronics industry, there is optimism surrounding the negotiations for a regional regulation on halal products, toy safety and low voltage electronic products. Still, respondents feel that it would be important for the GCC Standardization Organization (GSO) to develop a clearer mandate to avoid different interpretations of the regulatory framework between countries and to mitigate existing problems that companies face when dealing with local customs authorities. 24

29 Effectiveness of government bureaucracy The relatively long registration procedure required to open a business and the limited amount of information available on the bureaucratic procedures are the principal challenges facing EU companies starting and winding up operations in the GCC region. The time required to register a business and the lack of information available on bureaucratic procedures were mentioned as having a strongly adverse or adverse effect on investment decisions by 34% of all interviewed participants. However, the time required to register a business was more negatively rated, with 20% of all survey respondents declaring that it has a strongly negative impact on investment decisions. The creation of investment agencies has eased the access to information in most countries. However, most of the companies interviewed needed to hire local consulting firms or pair up with local players to facilitate the process. Small EU companies report greater challenges registering their businesses due to a lack of resources and access to information. Companies that have wound up operations in the region have experienced highly bureaucratic and time-consuming processes. In the KSA it is particularly complicated to wind up a business since the authorities have to make sure that all pending tax and bureaucratic issues are settled before operations can be terminated. In such cases, companies have hired representatives with local registration to mediate communication with local authorities until all bureaucratic matters are settled. 25

30 Labour supply Among the elements related to labour supply, the obligation to employ a certain percentage from the domestic workforce was mentioned by 30% of all survey respondents as having either a strongly negative or negative impact on investment decisions. Limitations on hiring women were mentioned as having an adverse influence on investment decisions by 10% of all survey respondents. Companies comments indicate that ensuring national content is not a challenge in itself but it may lead to lower productivity and an increase in operational costs. Several interviewees indicate a preference for hiring female workers to tackle challenges related to productivity, arguing that females tend to perform better and be more business driven. However, the lack of skilled labour in certain specialised sectors has proven to be especially challenging. This makes it difficult for EU companies to retain talent and will ultimately lead to salary inflation. A number of EU companies have developed graduate programmes in partnership with local universities to tackle the first part of the issue. These companies have in addition introduced programs to drive up loyalty by, among other initiatives, rotating employees between the EU and GCC. These programmes focus on recruiting students from vocational and technical schools into a skills development programme and into areas where finding talent is most difficult. Some of these programmes specifically target female students with the goal of attracting and training a large number of female employees. 26

31 Stability of political environment As regards the political environment, the risk or occurrence of popular uprisings was mentioned by 28% of all interview participants as having a strongly negative or negative influence on investment decisions in the GCC region. Religious tension was mentioned by 14% of all respondents as having either a strongly adverse or adverse influence on investment decisions. Companies responses show that the main concern vis-à-vis this factor is the political stability of monarchies within the GCC zone and the government s ability to deliver on promises to increase private sector economic participation. Regime stability is perceived as a key enabler of long-term economic growth, protection of investments and security. Respondents first impressions are positive as governments are investing in infrastructure and important deals such as the partial privatization of the national Saudi oil and natural gas company ARAMCO. Additional comments from respondents point out that security threats are also considered relevant elements influencing investment decisions in the GCC region, despite the fact that, when compared to the broader MENA region, the companies perceive the GCC countries as more secure and politically stable. Various companies perceive the Gulf region as the safest destination when investing in warehouse facilities for products shipped to the Middle East. 27

32 Competitiveness of operating costs The competitiveness of operating costs positively influences the investment decisions of EU companies in the GCC region. It is the second most positive factor after the economic outlook. Real estate prices and energy prices are the most positive elements in this category. The cost of labour was ranked as having a strongly positive effect by 14% of all survey participants. This contradiction with previous results on Labour Supply can be explained by the respondent s sector of activity and the nature of the workforce. Companies that find labour costs attractive are predominantly operating in the construction sector and rely on the cheaper migrant workforce. During the interviews, these companies also report challenges in recruiting and retaining skilled local workers. Participating companies find operating costs in the GCC region reasonable when compared to other developing economies. However, companies remain concerned about the likely increase in labour costs, operating costs and living costs after the introduction of VAT. Despite the favourable real estate prices in the region, some companies express concern about the requirement to rent larger offices and to apply for expat visas - the two are coupled by certain governments. Few companies interviewed are considering investing in production facilities in the GCC region in the short and medium term, mostly due to the likely increase in operating costs in the years to come. 28

33 Government incentives Among the government incentives, free zones and low levels of taxation (both income and corporate tax) have the most positive effect on EU companies decisions to invest in the region. The existence of free zones was mentioned by 18% of all survey participants as having a strongly positive or positive effect on investment decisions, followed closely by the levels of corporate and income taxes by 16%. According to the survey participants, these factors make the GCC region the most business-friendly environment in the Middle East. However, companies report that recent GCC country government budgetary constraints have resulted in less funding opportunities in recent years. Governments in the GCC region are now preferring to engage in Public-Private Partnerships to share the cost of investments with the private sector. The increase in costs for government services and bureaucratic documents, in combination with the above comments on the operating costs, is mentioned by companies as signs of change in the region. Furthermore, the companies express their concern about the possible introduction in the future of higher levels of corporate and income tax, following the introduction of VAT in The introduction of such income taxes would certainly impact the decisions made by EU companies about doing business in the region, as it would represent a barrier to hiring expats and an increase in companies' operating costs. 29

34 Effectiveness of the legal system Regarding the effectiveness of the legal system in the GCC countries, the existence of BITs with a company s country of origin was mentioned by 8% of all survey participants as having either a strongly positive or positive effect on investment decisions. The strength of legal investment protection had the same amount of positive references, but was also rated as having an adverse effect by 6% of survey respondents. The investors mention that their companies must adapt to the local and religious laws and that it is sometimes challenging to integrate such regulations or to avoid using forbidden terms in contracts. For companies operating in the KSA, the lack of law codification and the absence of a specialised commercial court structure are major challenges, aggravated by the fact that local companies seldom accept international courts for mediation and litigation when signing contracts with foreign investors. 30

35 Geographical location and Infrastructure The geographical location and infrastructure of GCC countries has a positive influence on investment decisions in the region, even though it was the least important factor in the survey. According to 30% of all survey participants, access to neighbouring countries and efficient communication networks have a strongly positive or positive influence on investment decisions in the GCC countries. The accessible ports and airports and the ease of obtaining utility connections were mentioned by 26% of all survey participants as having either a strongly positive or positive effect on investment decisions. The proximity of GCC countries and the quality of transportation means are particularly relevant for companies operating in infrastructure, logistics and consumer goods. The accessibility to neighbouring countries and the good conditions of airports and ports allow companies to set a regional headquarter in one of the region s free zones and to easily expand operations within the GCC. 31

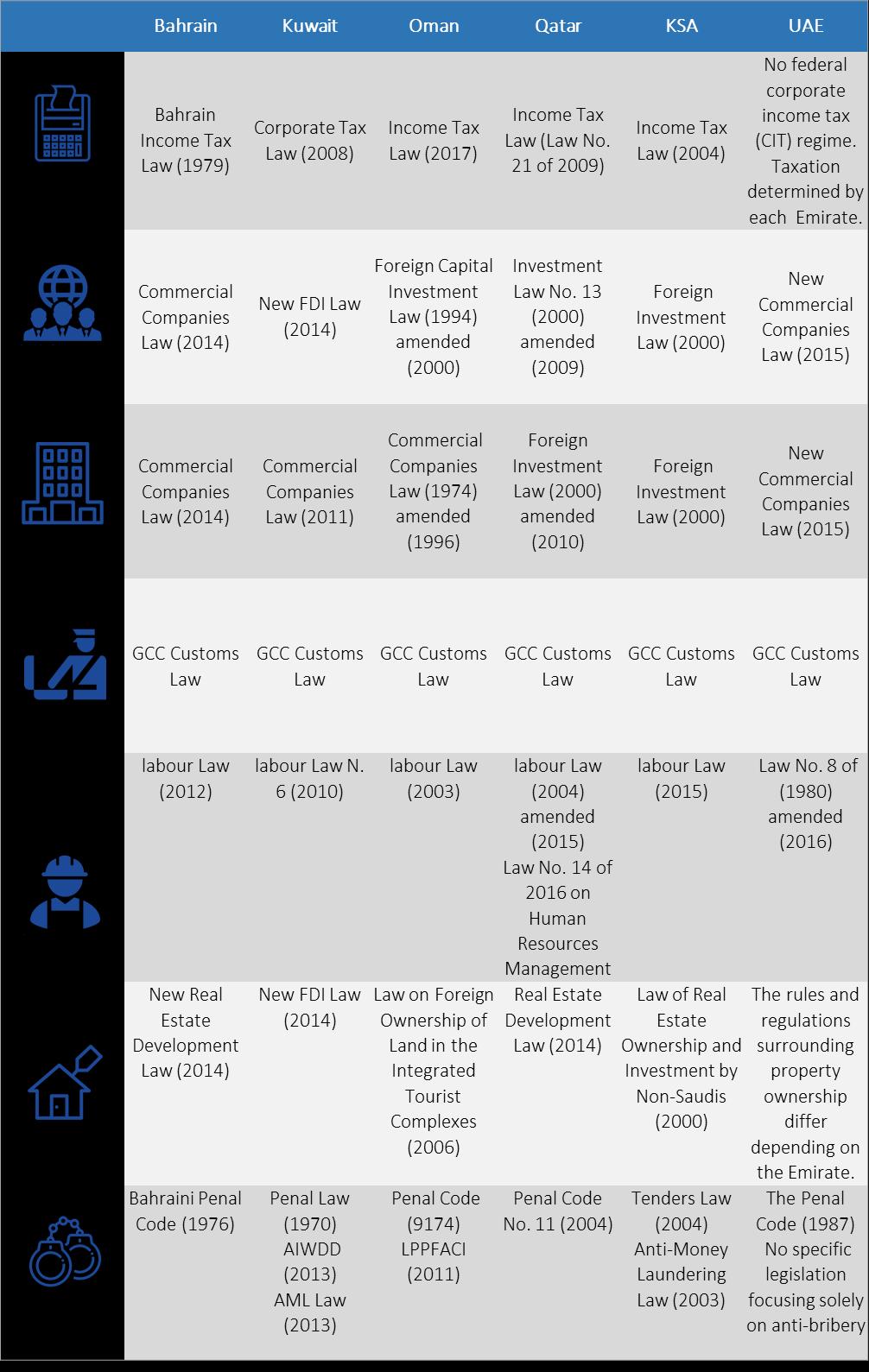

36 Section 2: Regional Analysis Comparison of FDI-related legislation across GCC countries, including EU companies views This section seeks to provide a comparative overview of the key FDI-related regulations in each GCC country. The topics were selected based on their relevance for EU companies in the GCC region (as indicated during the interviews) and on the availability of complete and reliable information. The main sources used in this section were the investment laws and business regulations themselves (when available in English); tax and legal guides from specialised advisory firms; analysts assessments from economic reports and investment guides. The comparative section on regulatory frameworks also includes a paragraph on investors assessments on each topic as provided during the interviews. 32

37 33

38 Corporate income tax In general, the GCC region has a flexible tax regime on corporate income. Bahrain and Kuwait have the lowest corporate income taxes. In Kuwait, the KSA and Oman, tax holidays and incentives are used to attract businesses to the region. The UAE is virtually tax-free, except for the oil and gas and financial services sectors where formal taxation is applied. In Qatar, a 10% flat rate income tax is levied on businesses that are not wholly owned by GCC nationals, whereas nationals are expected to make the zakat contribution. 9 Finally, tax regulations across GCC countries may vary by company size and sector of activity. The oil and gas industry for example, can be subject to specific income taxes. The favourable tax regime in the GCC is an important factor of consideration for the EU companies in the region. The interviewed companies indicate that introduction of further corporate or income taxes (after the VAT tax is in place) would represent a barrier for future investments in the GCC. Earlier this year, the Unified Agreement for VAT was published in the KSA s official gazette, providing a framework for the operation of VAT across the GCC region. 10 By July 2017, the KSA and the UAE ratified the agreement and published their national implementation acts. As a result, the GCC Agreement entered into force. The agreement allows for a basic VAT rate of five percent as well as for certain supplies of goods and services to be zero-rated or VAT-exempt. Each member state must translate the framework into its own local law and implement the VAT principles. The UAE and the KSA have confirmed their intention to collect VAT from January In contrast, local GCC companies are expected to make zakat (Islamic alms duty) contributions. Only in the KSA is the payment of zakat institutionalised by the government. 10 PWC (2017). GCC: The Unified Agreement for Value Added Tax (VAT) across the GCC Region has been published in the official gazette of the KSA May 08, Available at: 11 KPMG (2017). The text of the GCC unified agreement for value added tax (VAT) has been published (in Arabic) by the Kingdom of Saudi Arabia. Available at: 34

39 Foreign ownership In recent years, more GCC countries have allowed certain companies to operate with 100% foreign ownership - the exception being Oman and the UAE. In the UAE, foreign ownership is only allowed for companies operating in the free zones; Oman does not allow foreign companies to operate with 100% foreign ownership with exceptions in certain sectors and for other GCC nationals. 12 In Bahrain and the KSA the limits to 100% foreign ownership only apply to companies operating in sectors that are listed on the respective Ministry of Industry and SAGIA s negative list, including oil exploration real estate and production of military equipment. 13 In Kuwait, the new FDI Law allows companies to have full foreign ownership outside of free zones. In Qatar, a new draft law was presented in 2016 permitting 100% foreign ownership in all sectors, provided the non-qatari has a Qatari services agent, but it has yet to be enacted. 14 EU companies in the region welcome the possibility to operate with 100% ownership, however, several interviewed companies stress that difficulties in operating without a local partner in some GCC countries remains a barrier for investments. 12 In Qatar the exempt sectors are, subject to special government approval; agriculture, banking, business consultancy and technical services, cultural services, development and exploitation of natural resources, distribution services, education, energy, entertainment services, health, industry, information and communication services, insurance, sports services and tourism. See US Department of Commerce (2017). Qatar 1-Openness to and Restriction on Foreign Investment. Available at: 13 SAGIA. List of businesses prohibited for foreign investments. Available at: mitted.pdf 14 Qatar Tribune New law allows 100 % non-qatari investment in all sectors. Available at : 35

40 Business structures As highlighted in the above table, there are several kinds of business structures that foreign companies can use in the GCC countries. However, in the interviews, the companies report difficulties navigating the bureaucratic system in some countries. They highlight the importance of strategically choosing a business structure in this region to ease the bureaucratic procedures. Customs duty A five percent regional custom tariff is applied by all countries in the region, with a few exceptions for certain products. Bahrain and Qatar apply higher tariffs on alcoholic beverages and tobacco products. The KSA also applies higher tariffs for certain products that compete with its local industries, while weapons, alcohol, narcotics, pork, pornographic materials, distillery equipment and certain sculptures are completely banned. In Oman and the UAE, goods imported into free zones are exempted from custom duties. The level of customs duties in the GCC region is an overall positive element for the EU companies operating there, however, product registration and regulatory frameworks for imported goods remain a challenge for companies shipping products to the GCC region. 36

41 Labour All GCC countries have implemented regulation that seeks to increase the level of participation of nationals in their private sector workforce. In Bahrain, Kuwait, Oman, the KSA and the UAE the percentage of employed locals varies by company size and sector of operation, as can be seen in the table above. In the case of Kuwait, the quota for employment of nationals in the tourism, construction, electricity and gas and transportation sectors is specified per job position. In Qatar, priority in employment is given to Qatari nationals. Qatari nationals seeking jobs can register with the Labour Ministry for potential job placements. Specific sectors, including banking, may be subject to quota requirements to employ Qatari nationals and some organizations have self-imposed quotas. In contrast, employers seeking to hire non-qataris from abroad must first obtain permission from the government. The new Labour Law of Qatar aims to balance the rights of employers and employees, offering hiring priority to Qatari nationals and specifying several employee obligations for companies. The employment of Qatari nationals is one of the criteria considered when tax exemptions are granted. The requirements for national participation are one of the top four most adverse elements affecting EU companies investment decisions. At the same time, EU companies do not perceive the mandatory minimum employment of local workers only as a barrier to investment in the region. Instead, many of the survey respondents acknowledge its importance for national development in the GCC countries and for creating a long-term solution to the current shortage of specialised workers in certain sectors. 37

42 Real estate As shown in the above table, foreign companies operating in Bahrain, Qatar, the KSA and the UAE are only allowed to develop real estate for commercial activities under certain conditions. Companies in possession of a development license in those countries may develop properties in pre-defined Investment Areas. In Kuwait and Oman, real estate development for commercial activities is off-limits to foreign investors. As an exception, GCC nationals and entities fully owned by GCC nationals can own real estate and land in Kuwait. In Oman, corporate entities may only hold real estate for its operations, such as administrative offices or warehousing. Interviewed companies engaged in real estate development projects in the region argue that the restrictions to own land in certain countries is not a barrier to investments. Instead, the designated Investment Areas for foreign companies are often ideal for the development of infrastructure and real estate projects. 38

43 Anti-bribery and corruption The different pieces of legislation listed above have stringent anti-bribery and corruption regulations by defining bribery in the context of the public sector and establishing the punishment for corrupt practices. Moreover, certain GCC countries have created additional mechanisms and enforcement measures. For example, the KSA s National Anti-Corruption Commission, or Nazaha, is mandated to combat administrative and financial corruption. However, despite such efforts, the culture of patronage and wasta (simply defined as favouritism, or an attempt to use the influence of relatives or acquaintances to achieve certain objectives), continues to exist to varying degrees in certain GCC countries according to the interviewed companies. Hence, companies also report a growing tendency to prioritise the quality of a product and the terms under which it is offered over connections. This is particularly the case for companies operating in highly specialised segments, including in construction and engineering sectors where the culture of patronage has previously been particularly pronounced. 39

44 Cross-cutting findings on the regulatory framework in the GCC region for EU FDI The areas with the largest cross-cutting potential for improving the regulatory FDI framework fall into three general categories: 1) business structures, 2) labour regulations and 3) regional integration. 1) Several companies indicate that, while formally possible, it can be challenging to operate with 100% foreign ownership in certain countries and sectors. When it comes to the day-to-day task of winning contracts and navigating the bureaucracies to obtain permits, there seems to be more of a delay without a local partner. In response, the companies must rely on local consulting services or create joint ventures. As one large corporation operating in the KSA puts it: If you are a Saudi company and have the same or similar competencies [as a non-saudi company], you will most likely be prioritised. So, there is equal treatment in terms of legislation, but when competing, it can be a challenge. The EU companies, such as the one represented by the above voice, need to be treated equally in practice and not just on paper. 2) The need to hire a minimum percentage of national workers was not mentioned as a deterrent to investment by most of the companies contributing to this report s survey, especially the large corporations. Instead, they view it as an understandable requirement. The key to making the national worker quota a success is to structure the engagement and training of local workers in the best possible manner. We see that the locals [Saudis] are realizing that they too have to professionalise as the markets get more competitive - said one mediumsized company in the KSA. The EU companies said that the goal of such policies should be to create win-win situations, where the companies, the foreign and local employees and the host countries, all benefit. The companies suggest that this could be achieved through training centres for local workers with a focus on specific skills, as well as larger training programmes in partnership with local universities. Furthermore, they suggest that this training be complemented by international training at the companies headquarters in the EU. On the other hand, one SME in the KSA said that since the local employees know they are a necessary headcount, they do not think they need to put in the same effort. Generally, SMEs prefer that the local government provides the training, since they do not have the resources to train overseas. 3) The EU companies report challenges in adapting to the constantly changing regulatory framework in the region. One large corporation currently opening in the KSA with ambitions to expand to the UAE, Oman and Kuwait noted that, bureaucracy is a major issue and it might take us 5 years to get everything done, even though we are ready to open tomorrow. Another large corporation active in the UAE commented, It is particularly tough for firms that sell services there were a lot of papers, translations, attestations and we needed to involve the embassy and employ locals to support the process. Finally, a large corporation 40

45 active across the region mentioned that there are not even uniform rules on how to certify meat as halal. Indeed, the perceived proliferation of regulations and procedures is effectively a tax on investment and intra-gcc trade. The EU companies are enthusiastic about regional regulatory frameworks that replace overlapping procedures. They welcome the common GCC Customs Law as an example of a way to achieve such simplification and standardization of requirements. The companies are optimistic about further work in this direction with increased cooperation and dialogue between the public and private sectors. For instance, interviewed companies believe that current negotiations on a GCC regulation for toy safety and low voltage electronic products could stimulate investment and later be replicated in other product categories such as halal food. Future trends and opportunities for the FDI reform process To increase their effectiveness on FDI, GCC countries national visions and development plans need to further evolve into actionable and sequenced measures. In other words, they should be informed by and effectively address the nuts and bolts issues of running a business in the respective GCC countries. To be able to address the practical issues, the GCC governments should explore opportunities for dialogue with the private sector. The ability to comment on new laws, for example, would give businesses both notice of planned changes and the opportunity to voice any challenges that the legislation may present. Several EU companies operating across the region mention the Tamkeen programme in Bahrain as a good example of a government being proactive about understanding and addressing the private sector s needs, in this case the need for a skilled, local workforce. The Tamkeen programme co-finances the training of Bahraini nationals employed by foreign companies, leading to reductions in labour costs. Another example is a forum of exchange between GCC policymakers and the EU private sector established in May 2017 as part of the EU-GCC Dialogue on Trade and Investment. 15 A delegate from an EU Member State Commercial Office finds this Dialogue particularly useful because GCC policymakers often lack a proper dialogue with stakeholders and in general, seem focused on improving only the broader investment climate. In the future, the forum could be aligned further with the activities of the individual Member States. Next, there is large potential for deeper regional integration. For that to occur, the mandate of regional organizations, such as the Gulf Standardization Organization (GSO), would need to be strengthened. As mentioned, the overlapping and at times obscure 15 European Commission (2017). Countries and regions: Gulf region. Available at: 41

46 regulations have the same effect as taxes on investment. The interviewed companies argue that the GSO does not currently have the authority to ensure that joint decisions are implemented at a national level, which indicates that national governments are not willing to compromise their sovereignty. Thus, the EU companies must contend with the challenges of non-streamlined regulations for at least the short to medium-term. 42

47 Section 3: GCC Country Profiles Bahrain Key facts Indicator Figure Year Surface area (sq. km) Population (projected, 000) Pop. density (per sq. km) GDP per capita (current prices, USD) International migrant stock ( 000 /% of total) 704 / 51% mid-2015 Signed BITs (# of countries) Doing Business Doing Business Source: UN DATA (World Statistics Pocketbook United Nations Statistics Division) & UNCTAD Investment Policy Hub, World Bank A brief introduction to the economy of Bahrain Having been the first Gulf country to discover oil in 1932, Bahrain also built the region s first petroleum refinery in This eventually came to source most of its inputs of oil from the KSA. Today oil revenues only comprise 20% of GDP and the main drivers of Bahrain s economic growth are services and government investment in construction and infrastructure, backed by capital from the GCC Development Fund among others. Current projects in the pipeline include the expansion of Bahrain International Airport, the construction of a new port and the construction of the new King Hamad Causeway that links Bahrain with the KSA. 43

48 Source: UNCTAD STAT database & Trading Economics (based on data from the Central Bank of Bahrain). Economic growth slowed to 2% in 2016 while the government debt continued to rise, exceeding the 60% proposed as the limit in a potential GCC currency union. For this reason, Bahrain is the most vulnerable GCC country due to its limited savings. 16 In response, the government has set itself the goal of balancing its budget by 2021, introducing measures such as VAT from 2018 and a reduction of the amount of subsidies and numbers of government ministries. Bahrain has already initiated an ambitious reform programme with the launch of its Vision 2030 in This is a comprehensive economic vision, providing a clear direction for the continued development of Bahrain s economy. It focuses on shaping the vision of the government, society and the economy based on three guiding principles: sustainability, fairness and competitiveness GLOBAL COMPETITIVENESS INDEX Health & Education (Positive) Tech Readiness (Positive) Market efficiency (Positive) Market size (Negative) Macro Environment (Negative) Innovation (Negative) 2017 INDEX OF ECONOMIC FREEDOM Tax Policy (Positive) Trade Freedom (Positive) Monetary Stability (Positive) Fiscal Health (Negative) Judicial Effectiveness (Negative) Government Integrity (Negative) CREDIT RATINGS S&P: BB- (2017) Fitch: BB+ (2017) Moody s: B1 (2017) 16 IMF (2017). IMF Staff Completes 2017 Article IV Mission to Bahrain. Available at: article-iv-mission 44

49 Economic Vision 2030 Bahrain s Economic Vision 2030, launched in October 2008 by King Hamad bin Isa Al Khalifa, was one of the first long-term national plans launched in the GCC region. The objective of the vision is to shift from an economy built on oil wealth to a productive, globally competitive economy, shaped by the government and driven by a pioneering private sector. An economy that raises a broad middle class of Bahrainis who enjoy good living standards through increased productivity and high wage jobs. 17 As stated, the Vision focuses on promoting the role of the private sector and securing quality jobs for Bahrain s fast growing young population, including through FDI. The Vision has three thematic priorities: Economy Stimulate growth by enhancing private sector productivity and skills Stimulate diversification by encouraging investment in high-potential sectors Transform and create a favourable environment for entrepreneurship and innovation Government Develop high quality policies within the areas of economy, finance, healthcare, education, environment, security and social justice Support Public Private Partnerships to reduce costs and increase service quality Reduce government size and cost to increase productivity and efficiency Cut inefficient spending and subsidies to ensure fiscal stability Attract public and private funds to invest in infrastructure and services Social Encourage private philanthropy Equip local workers with applied and advanced skills National Development Strategy To achieve the wider Economic Vision 2030, Bahrain has developed a series of short-term strategic plans, most recently the National Development Strategy for The National Development Strategy is regularly updated with specific milestones for the public and private 17 Bahrain Economic Vision 2030 is available at: Vision-2030-May-2013.pdf 45

50 sectors and the government has created a platform to follow up with the implementation of the strategy. 18 Based on the Strategy, the Bahrain Economic Development Board (EDB) attracts foreign investments to five priority sectors to promote economic diversification. Moreover, the Board advises investors on the Bahraini investment climate. The Bahrain Investors Center (BIC) is the one-stop-shop for licensing and registering incoming companies. Key investment sectors Financial services Manufacturing & logistics Tourism & leisure ICT Entrepreneurship FDI inflows to Bahrain FDI inflows to Bahrain (USD Billion) FDI inflows (% of GDP) % of GDP FDI inflows FDI Inflows to Bahrain (million USD, current prices) Source: UNCTAD STAT database * * Source: UNCTAD STAT database * Data is subjected to changes once the UNCTAD STAT database is updated

51 FDI inflows to Bahrain decreased sharply between 2008 and 2011 before rising again in In the two most recent years they have fallen dramatically again, including a year of net outflows in The decline in FDI inflows was initially a result of the global financial crisis, but was further exacerbated by remaining domestic constraints to FDI, namely the small market size, a relatively slow pace of privatization, a rigid labour market and political instability. Reform of FDI laws and identification of key players To counter the falling oil revenues and budget deficits, the Bahraini government has initiated fiscal consolidation while introducing new regulations to attract investors and foreign companies to the country, making all the main sectors open to full foreign ownership. The key reforms introduced in recent years are listed below. Source: OPEC (Yearly Basket Price). 47

52 KEY PLAYERS KEY REFORM INTENDED EFFECTS The Royal Family (The King) The Cabinet The Consultative Council Vision 2030 (2008) New Labour Law for the Private Sector (2012) New Commercial Companies Law (CC) (2014) Provide a clear direction for the country s development, focusing on economic diversification & productivity Align domestic legislation with signed international treaties, improve working conditions for nationals & expatriates Allow for public joint stock companies with foreign capital, reduce registration time, reorganise government agencies The Consultative Council Central Bank of Bahrain Supreme Judicial Council & Court of Cassation Central Bank of Bahrain (CBB) Central Bank of Bahrain (CBB) Manara Developments with Government support Ministry of Industry New Lease Law (2014) New Transfer System goes live (2015) Two Commercial Courts (2016) New Trust Law (2016) Protected Cells Companies Law (PCC) (2016) First phase of Gateway project (2016) Bahrain Investors Center (BIC) (2016) Ensure uniformity among all types of rental premises across the Kingdom and increase investors confidence The Near Real-Time Funds Transfer System simplifies & secures financial operations for foreign investors A new forum for dispute settlements involving foreign investors that do not meet the BCDR Court s requirements Formally recognises trusts established under and governed by the law of a foreign jurisdiction Introduction of Protected Cell Companies and Investment Limited Partnerships in the Banking and Finance Sectors Attract international investments and new companies to the country s first freehold trade zone Provide support for incoming investors and facilitate the process of registering a business 48

53 Brief assessment Bahrain's Economic Vision 2030 demonstrates the government s resolve to strengthen the private sector and boost the economy. However, there is still a long way to go and many challenges ahead to reach its goals and economic vision. 19 For example, there is yet no single designated authority to screen and approve FDI in Bahrain. 20 Decisions to approve or reject FDI appear to include considerations of land scarcity and national security and the government s priority to generate the maximum number of jobs for Bahraini nationals. However, no cases of rejection of FDI can be verified. 21 Moreover, the country s recent civil unrest and political instability during the Arab Spring, partially caused by unemployment and relatively slow economic growth, negatively impact perceptions of Bahrain as a FDI destination. In addition, the government s decision to boost growth through public spending has raised investors concern about the country s fiscal stability. The top priority for the Bahraini government when it comes to attracting FDI should therefore be to ensure political and fiscal sustainability, in addition to the vision 2030 and the subsequent reforms. Bilateral Investment Treaties Bahrain has signed BITs with 32 countries, including nine with EU Member States, of which seven are in force. 22 SIGNED BITs BETWEEN BAHRAIN AND EU MEMBER STATES EU country Signed In force Duration (years) Known disputes Inflow since BIT s entry into force* (USD M) BLEU Not in force 10 None - Bulgaria 2009 Not in force 10 None - Czech Republic None - 19 Bahrain Vision 2030, p.17. Available at: 20 US Department of Commerce. Bahrain s openness to FDI. Available at: 21 Bahrain Vision 2030, p.16. Available at: 22 The non-eu countries: Algeria, Belarus, Brunei Darussalam, China, Egypt, India, Iran (Islamic Republic of), Jordan, Lebanon (twice), Malaysia, Mexico, Morocco, Pakistan, Russian Federation, Singapore, Sudan, Syrian Arab Republic, Thailand, Turkey, Turkmenistan, United States of America, Uzbekistan, and Yemen 23 Belgium-Luxembourg Economic Union (BLEU) 49

54 France None 51 Germany None - Italy None 100 Netherlands None - Spain None - The UK None - Source: UNCTAD FDI/TNC database & UNCTAD Policy Hub. * No data available post PRACTICAL INFORMATION ON OPENING A BUSINESS IN BAHRAIN Agency Support Provided Website Link Contact Information Bahrain Economic Development Board Information on business opportunities, on how to set up a business and location directory/pages/international% 20offices.aspx#.WQiaToh95PY Tel: investorenquiries@ bahrainedb.com Offices in the UK, Netherlands, Germany, and France Bahrain Investors Center (BIC) Facilitation of business start-up process, from the initial application submission to the start of business operations C%20Centers/BahrainInvestors Center/Pages/index.aspx Tel: (+973) ; 50

55 Kuwait Key facts Indicator Figure Year Surface area (sq. km) Population (projected, 000) Pop. density (per sq. km) GDP per capita (current prices, USD) International migrant stock ( 000 /% of total) / 74% mid-2015 Signed BITs (# of countries) Doing Business Doing Business Source: UN DATA (World Statistics Pocketbook United Nations Statistics Division) & UNCTAD Investment Policy Hub, World Bank A brief introduction to the economy of Kuwait Kuwait has over 6% of the world s oil reserves and has for many years attracted significant levels of foreign investment in its oil industry and related industries. The oil and gas sector account for almost 60% of the country s GDP and 95% of its export revenues. 24 GCC Limit Source: UNCTAD STAT database & Trading Economics (based on data from the Central Bank of Kuwait). 24 OPEC (2016). Kuwait key facts and figures. Available at: 51

56 Kuwait has had difficulties maintaining high economic growth and budget surpluses since the recent drop in the oil prices. Kuwait s economic activity has been supported through public spending in infrastructure, which boosted investment and supported consumption. Kuwait has financed this with a combination of drawdowns from the General Reserve Fund and domestic debt issuance, which has in effect increased total government debt moderately in recent years. Kuwait's reform agenda dates to 2000, when the Kuwaiti government first initiated several measures to attract FDI and to increase the role of the private sector. Given its high reserves, reform in Kuwait is perhaps less fiscally urgent than in other GCC countries. The government is focused on addressing future challenges arising from their reliance on oil revenues through its New Kuwait 2035 plan GLOBAL COMPETITIVENESS INDEX Macro Environment (positive) Health & Education(positive) Infrastructure (positive) Bureaucracy (negative) Labour regulation (negative) Corruption (negative) 2017 INDEX OF ECONOMIC FREEDOM Trade Freedom (positive) Monetary Stability (positive) Tax Burden (positive) Rule of Law (negative) Business Freedom (negative) Labour Freedom (negative) CREDIT RATINGS Fitch: AA (2016) Moody s: Aa2 (2017) 52