Audit Review of External Business Relationships: National NeighborWorks Association (NNA)

|

|

|

- August Holmes

- 5 years ago

- Views:

Transcription

1 Internal Audit NeighborWorks America Audit Review of External Business Relationships: National NeighborWorks Association (NNA) Project Number: NWA.CORP.NNA.2017

2 Audit Review of External Business Relationships: National NeighborWorks Association. Table of Contents Function Responsibility and Internal Control Assessment... 3 Executive Summary of Observations, Recommendations and Management Responses... 4 RISK Rating Legend Background Objective Scope Methodology Observations and Recommendations Conclusion Page 1 of 13

3 July 11, 2017 To: Subject: NeighborWorks America Audit Committee External Business Relationships: National NeighborWorks Association Enclosed is our report for the audit review of the National NeighborWorks Association (NNA). Please contact me with any questions you might have. Thank you. Frederick Udochi Chief Audit Executive Attachment cc: J. Bryson R. Bond T. Chabolla R. Simmons Page 2 of 13

4 Function Responsibility and Internal Control Assessment Audit Review of External Business Relationships: National NeighborWorks Association Business Function Responsibility Report Date Period Covered Public Policy & Legislative Affairs July 11, through 2015 Assessment of Internal Control Structure Effectiveness and Efficiency of Operations (b) (5) Reliability of Financial Reporting Not Applicable Compliance with Applicable Laws and Regulations Not Applicable This report was conducted in accordance with the International Standards for the Professional Practice of Internal Auditing. 1 Legend for Assessment of Internal Control Structure: 1. Generally Effective: The level and quality of the process is satisfactory. Some areas still need improvement. 2. Inadequate: Level and quality of the process is insufficient for the processes or functions examined, and require improvement in several areas. 3. Significant Weakness: Level and quality of internal controls for the processes and functions reviewed are very low. Significant internal control improvements need to be made. Page 3 of 13

5

6

7

8

9

10

11 RISK Rating Legend Risk Rating: HIGH A serious weakness which significantly impacts the Corporation from achieving its corporate objectives, financial results, statutory obligations or that may otherwise impair the Corporation s reputation. Risk Rating: Moderate A control weakness which could potentially undermine the effectiveness of the existing system of internal controls and/or operational efficiency, integrity of reporting and should therefore be addressed. Risk Rating: Low A weakness identified which does not seriously detract from the system of internal control and or operational effectiveness/efficiency, integrity of reporting but which should nonetheless be addressed by management. Management Responses to The Audit Review of: External Business Relationships National NeighborWorks Association # Of Responses Response Recommendation # 2 Agreement with the recommendation(s) 2 Disagreement with the recommendation(s) Page 10 of 13

12 Background Internal audit routinely carries out audit reviews of the Corporation s external business relationships (EBR s) and as part of that practice the National NeighborWorks Association (NNA) was scheduled for a review this fiscal year. NeighborWorks America provides funding to the NNA Fund, a section 501 (c) 3 organization, in the form of grants annually and the NNA Fund makes contributions to the National Neighborhood Housing Network Corporation, d/b/a National NeighborWorks Association (NNA), a section 501 (c)(6) organization. The NNA Fund has been legally determined to be able to sub-grant funds it has received from NeighborWorks America to NNA as long as those funds are not used for lobbying, satisfies the specific grant rules and that the amount of the grant is less than NNA s non-lobbying budget if any in existence. NNA is classified as a 501(c) (6) organization, it is not subject to the same lobbying restrictions as a 501(c) (3). 501(c)(6) organizations may issue advocacy (that does not constitute political campaign intervention) and engage in lobbying without jeopardizing its tax exempt status provided that such activities are related to the organization s exempt purpose. The NNA Fund and NNA both reported on their Forms 990 that their organizations have not engaged in direct or indirect political campaign activities. NeighborWorks America is a 501(c) (3) public charity and as such, is subject to restrictions on its lobbying and political campaign activities. These restrictions provide that no substantial part of the activities of the organization may constitute carrying on propaganda or otherwise attempting to influence legislation. There is also language in NeighborWorks enabling legislation that restricts the corporation from contributing to, or otherwise supporting, any political party or candidate for elective office. As a result it is of importance to ensure that funds provided by NeighborWorks are not in any way used to for restricted purposes. Objective The objective of this review was to obtain reasonable assurance: o That funds provided to The NNA Fund were used only for their intended purpose as prescribed by NeighborWorks America. o That funds contributed to National NeighborWorks Association (NNA) were also not used for any restricted purposes. Scope Internal Audit conducted a review of the grants awarded to The NNA Fund during fiscal years 2013, 2014, and 2015 and the related expenditures of National NeighborWorks Association (NNA). This review was essentially limited to a financial review based on audited financial statements in question and request for documentation to verify the use of grant funds provided by NeighborWorks America. Page 11 of 13

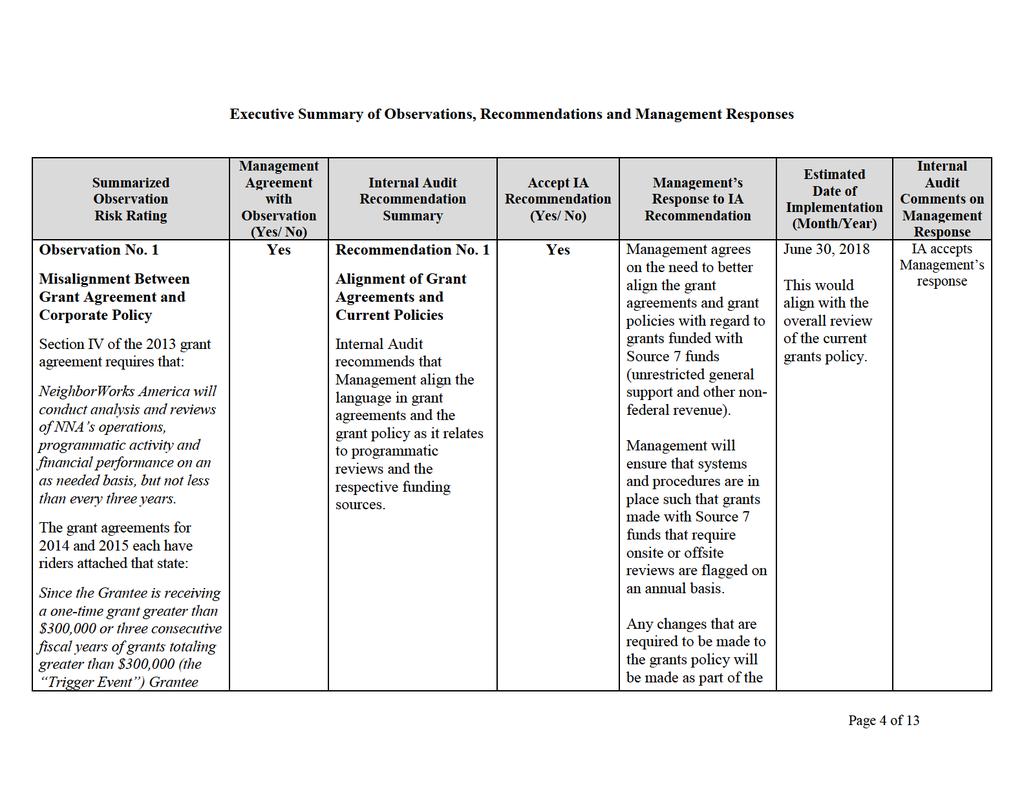

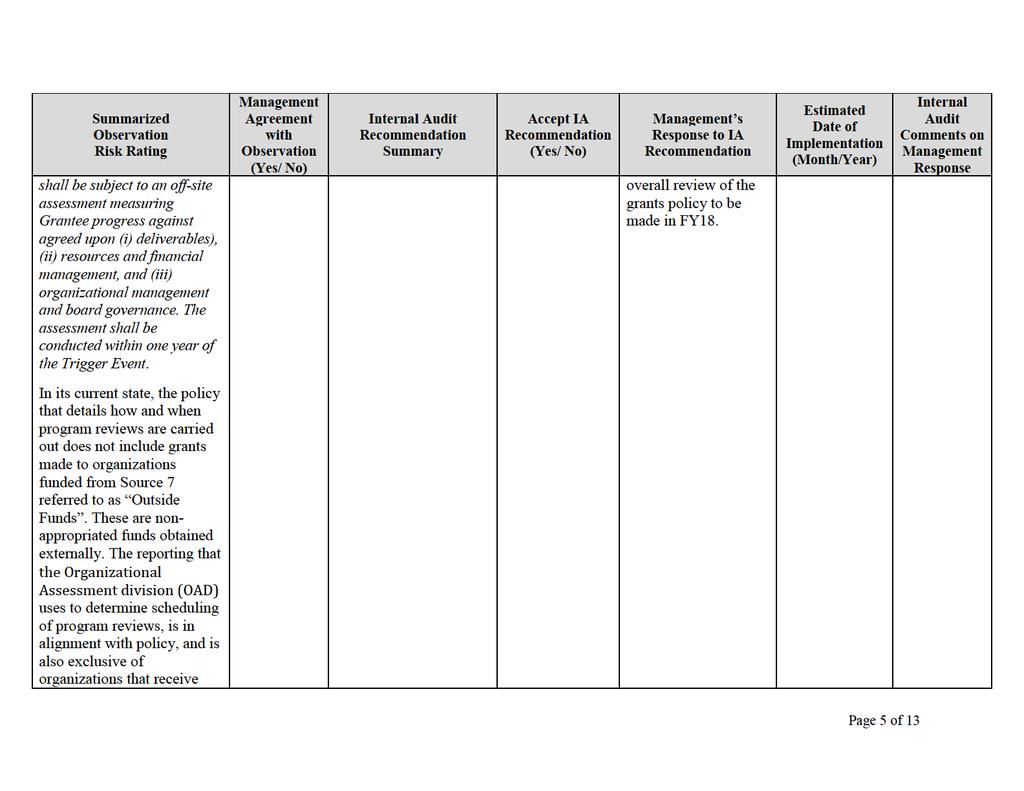

13 Methodology The observations and recommendations contained in a prior FY2008 report were reviewed as part of the review approach. For the years , Internal Audit requested and reviewed Form 990 for both the NNA Fund and NNA, the request for funding and the corresponding proposed budget that was submitted as a part of the application process, Grant Agreements, NNA and NNA Fund combined audited financial statements, Use and Accomplishment Letters, and the Use of Funds Spreadsheets. Two memos that were written detailing the relationship between NNA and the NNA Fund were also obtained and reviewed. For each fiscal year being reviewed, a sample of expenses was selected for detailed testing and then compared to supporting documentation to determine if the expenditures were in compliance with the grant agreements. Below are the observations and recommendations that resulted from the testing performed. Observations and Recommendations Observation 1 Misalignment between Grant Agreement and Corporate Policy Section IV of the 2013 grant agreement requires that: NeighborWorks America will conduct analysis and reviews of NNA s operations, programmatic activity and financial performance on an as needed basis, but not less than every three years. The grant agreements for 2014 and 2015 each have riders attached that state: Since the Grantee is receiving a one-time grant greater than $300,000 or three consecutive fiscal years of grants totaling greater than $300,000 (the Trigger Event ) Grantee shall be subject to an off-site assessment measuring Grantee progress against agreed upon (i) deliverables), (ii) resources and financial management, and (iii) organizational management and board governance. The assessment shall be conducted within one year of the Trigger Event. In its current state, the policy that details how and when program reviews are carried out does not include grants made to organizations funded from Source 7 referred to as Outside Funds. These are non-appropriated funds obtained externally. The reporting that the Organizational Assessment division (OAD) uses to determine scheduling of program reviews, is in alignment with policy, and is also exclusive of organizations that receive source 7 funds. This may have been a contributing factor as to why the misalignment was not previously identified. Internal Audit confirmed that The NNA Fund grants are budgeted to and paid out of Source 7 Funds. The misalignment between the grant agreements and the corporate policy increases the risk of the program reviews not being completed. Recommendation 1 Alignment of Grant Agreements and Current Policies Internal Audit recommends that Management align the language in grant agreements and the grant policy as it relates to programmatic reviews and the respective funding sources. Observation 2 Lack of Substantive Program Reviews The lack of program reviews had also been noted in a prior FY 2008 internal audit report. While it was observed that financial analysis was completed for each year in review, Internal Audit was Page 12 of 13

14 unable to obtain evidence that a program/off-site review was performed per the requirement. The financial analysis includes a review of several factors including financial statement presentation; auditor communications; assets and liabilities; revenues and expenses; and liquidity, leverage, and cash flow. The purpose of the financial analysis is to make a determination about risk which is outlined in the conclusion of the financial analysis. Program reviews also look to make a determination about risk, however the scope is expanded beyond the financial statements and consider four areas of operation which include production and program services; resource management; financial management; and organizational management and board governance. The PROMPT Assessment tool is used in the program reviews and is designed to assess both organizational capacity and organizational risk. It was noted that the primary focus of the Off- Site PRO Assessment tool is organizational risk, however, capacity is still a consideration. NNA is classified as a 501(c) (6) organization and is not subject to the same lobbying restrictions as NeighborWorks America. Program reviews would allow NeighborWorks to actively monitor the risk associated with the external business relationship between NeighborWorks America, NNA, and The NNA Fund. Failure to effectively monitor and manage these business relationships could result in harm to NeighborWorks reputation, additional scrutiny, and/or a decrease in core appropriations. Recommendation 2 Conduct Programs Reviews for the NNA Fund and Any Other Sub Grantee Internal Audit recommends that upon the receipt of audited financial statements from The NNA Fund and NNA, the Organizational Assessment division (OAD) should schedule a program review for The NNA Fund and NNA. This could be undertaken either as an off-site or on-site review and implement plans to place such reviews on a scheduled term in accordance with the grant agreement. Conclusion The audit review of the External Business Relationship National NeighborWorks Association, found that funds granted to the NNA Funds appear to be used for their intended purpose as prescribed by NeighborWorks America. Internal Audit did not note any irregularities in its review of the documentation that was provided as it related to expenses, the financial statements, or the 990 forms. Inconsistencies between the grant agreement and policy with regard to the programmatic reviews were identified. Specifically, the grant agreements for the NNA Fund, an organization that receives outside funds, contained language that required program reviews while the policy governing program reviews does not include organizations that receive nonappropriated funds. It was also noted that no programmatic reviews have occurred despite previous audit finding recommending that these reviews occur. Our interactions with The COO, PPLA, OAD, and NNA were collaborative and productive. We would like to extend our thanks to all involved for their cooperation and assistance during this review. Page 13 of 13

Internal Audit Department NeighborWorks America. Audit Review of External Business Relationships - Community Housing Capital

Internal Audit Department NeighborWorks America Audit Review of External Business Relationships - Community Housing Capital Project Number: NWA.EBRCHC.2012 Audit Review of External Business Relationships

Internal Audit Department NeighborWorks America Audit Review of External Business Relationships - Community Housing Capital Project Number: NWA.EBRCHC.2012 Audit Review of External Business Relationships

Office of the Register of Wills Anne Arundel County, Maryland

Audit Report Office of the Register of Wills Anne Arundel County, Maryland August 2007 OFFICE OF LEGISLATIVE AUDITS DEPARTMENT OF LEGISLATIVE SERVICES MARYLAND GENERAL ASSEMBLY This report and any related

Audit Report Office of the Register of Wills Anne Arundel County, Maryland August 2007 OFFICE OF LEGISLATIVE AUDITS DEPARTMENT OF LEGISLATIVE SERVICES MARYLAND GENERAL ASSEMBLY This report and any related

Office of the Clerk of Circuit Court Carroll County, Maryland

Audit Report Office of the Clerk of Circuit Court Carroll County, Maryland May 2008 OFFICE OF LEGISLATIVE AUDITS DEPARTMENT OF LEGISLATIVE SERVICES MARYLAND GENERAL ASSEMBLY This report and any related

Audit Report Office of the Clerk of Circuit Court Carroll County, Maryland May 2008 OFFICE OF LEGISLATIVE AUDITS DEPARTMENT OF LEGISLATIVE SERVICES MARYLAND GENERAL ASSEMBLY This report and any related

The Legal Aspects of Philanthropic & Nonprofit Advocacy in the Trump Era

The Legal Aspects of Philanthropic & Nonprofit Advocacy in the Trump Era Advocacy Organizational leaders should consider whether advocacy would be a highly effective and efficient strategy in advancing

The Legal Aspects of Philanthropic & Nonprofit Advocacy in the Trump Era Advocacy Organizational leaders should consider whether advocacy would be a highly effective and efficient strategy in advancing

Office of the Clerk of Circuit Court Talbot County, Maryland

Audit Report Office of the Clerk of Circuit Court Talbot County, Maryland July 2018 OFFICE OF LEGISLATIVE AUDITS DEPARTMENT OF LEGISLATIVE SERVICES MARYLAND GENERAL ASSEMBLY For further information concerning

Audit Report Office of the Clerk of Circuit Court Talbot County, Maryland July 2018 OFFICE OF LEGISLATIVE AUDITS DEPARTMENT OF LEGISLATIVE SERVICES MARYLAND GENERAL ASSEMBLY For further information concerning

STATE OF NORTH CAROLINA OFFICE OF THE STATE AUDITOR BETH A. WOOD, CPA

STATE OF NORTH CAROLINA OFFICE OF THE STATE AUDITOR BETH A. WOOD, CPA DURHAM COUNTY CLERK OF SUPERIOR COURT DURHAM, NORTH CAROLINA FINANCIAL RELATED AUDIT MAY 2018 STATE OF NORTH CAROLINA Office of the

STATE OF NORTH CAROLINA OFFICE OF THE STATE AUDITOR BETH A. WOOD, CPA DURHAM COUNTY CLERK OF SUPERIOR COURT DURHAM, NORTH CAROLINA FINANCIAL RELATED AUDIT MAY 2018 STATE OF NORTH CAROLINA Office of the

Office of the Clerk of Circuit Court Calvert County, Maryland

Audit Report Office of the Clerk of Circuit Court Calvert County, Maryland July 2018 OFFICE OF LEGISLATIVE AUDITS DEPARTMENT OF LEGISLATIVE SERVICES MARYLAND GENERAL ASSEMBLY For further information concerning

Audit Report Office of the Clerk of Circuit Court Calvert County, Maryland July 2018 OFFICE OF LEGISLATIVE AUDITS DEPARTMENT OF LEGISLATIVE SERVICES MARYLAND GENERAL ASSEMBLY For further information concerning

INTERNAL AUDIT DIVISION REPORT 2017/149

INTERNAL AUDIT DIVISION REPORT 2017/149 Audit of the regional operations for South Caucasus in Georgia for the Office of the United Nations High Commissioner for Refugees There was a need to address control

INTERNAL AUDIT DIVISION REPORT 2017/149 Audit of the regional operations for South Caucasus in Georgia for the Office of the United Nations High Commissioner for Refugees There was a need to address control

Office of the Register of Wills Montgomery County, Maryland

Audit Report Office of the Register of Wills Montgomery County, Maryland September 2012 OFFICE OF LEGISLATIVE AUDITS DEPARTMENT OF LEGISLATIVE SERVICES MARYLAND GENERAL ASSEMBLY This report and any related

Audit Report Office of the Register of Wills Montgomery County, Maryland September 2012 OFFICE OF LEGISLATIVE AUDITS DEPARTMENT OF LEGISLATIVE SERVICES MARYLAND GENERAL ASSEMBLY This report and any related

Approved-4 August 2015

Approved-4 August 2015 Governance of the Public Utility District NO.1 of Jefferson ( JPUD ) Commission PUD #1 of Jefferson County 310 Four Corners Road, Port Townsend, WA 98368 360.385.5800 Contents GOVERNANCE

Approved-4 August 2015 Governance of the Public Utility District NO.1 of Jefferson ( JPUD ) Commission PUD #1 of Jefferson County 310 Four Corners Road, Port Townsend, WA 98368 360.385.5800 Contents GOVERNANCE

STATE OF NORTH CAROLINA

STATE OF NORTH CAROLINA BEAUFORT COUNTY CLERK OF SUPERIOR COURT WASHINGTON, NORTH CAROLINA FINANCIAL RELATED AUDIT SEPTEMBER 2014 OFFICE OF THE STATE AUDITOR BETH A. WOOD, CPA STATE AUDITOR Beth A. Wood,

STATE OF NORTH CAROLINA BEAUFORT COUNTY CLERK OF SUPERIOR COURT WASHINGTON, NORTH CAROLINA FINANCIAL RELATED AUDIT SEPTEMBER 2014 OFFICE OF THE STATE AUDITOR BETH A. WOOD, CPA STATE AUDITOR Beth A. Wood,

Office of the Register of Wills Calvert County, Maryland

Audit Report Office of the Register of Wills Calvert County, Maryland May 2003 This report and any related follow-up correspondence are available to the public. Alternate formats may also be requested

Audit Report Office of the Register of Wills Calvert County, Maryland May 2003 This report and any related follow-up correspondence are available to the public. Alternate formats may also be requested

STATE OF NORTH CAROLINA OFFICE OF THE STATE AUDITOR BETH A. WOOD, CPA IREDELL COUNTY CLERK OF SUPERIOR COURT

STATE OF NORTH CAROLINA OFFICE OF THE STATE AUDITOR BETH A. WOOD, CPA IREDELL COUNTY CLERK OF SUPERIOR COURT STATESVILLE, NORTH CAROLINA FINANCIAL RELATED AUDIT JUNE 2018 STATE OF NORTH CAROLINA Office

STATE OF NORTH CAROLINA OFFICE OF THE STATE AUDITOR BETH A. WOOD, CPA IREDELL COUNTY CLERK OF SUPERIOR COURT STATESVILLE, NORTH CAROLINA FINANCIAL RELATED AUDIT JUNE 2018 STATE OF NORTH CAROLINA Office

GRASSROOTS SCIENCE PROGRAM

APRIL 2016 GRASSROOTS SCIENCE PROGRAM State Authorization: Session Law 2015-241, House Bill 97, Section 15.18 An act to make base budget appropriations for Current Operations of State Departments, Institutions,

APRIL 2016 GRASSROOTS SCIENCE PROGRAM State Authorization: Session Law 2015-241, House Bill 97, Section 15.18 An act to make base budget appropriations for Current Operations of State Departments, Institutions,

BYLAWS OF THE GLOBAL FUND TO FIGHT AIDS, TUBERCULOSIS & MALARIA 1

BYLAWS OF THE GLOBAL FUND TO FIGHT AIDS, TUBERCULOSIS & MALARIA 1 1 Approved by the Board on 28 January 2016 (GF/B34/EDP07) and amended by the Board on 14 November 2017 (GF/B38/DP05). Article 1. Structure

BYLAWS OF THE GLOBAL FUND TO FIGHT AIDS, TUBERCULOSIS & MALARIA 1 1 Approved by the Board on 28 January 2016 (GF/B34/EDP07) and amended by the Board on 14 November 2017 (GF/B38/DP05). Article 1. Structure

Definition of Officers Definition of Committees Executive Committee Financial Checklist

Definition of Officers Definition of Committees Executive Committee Financial Checklist The Internal Auditors and individuals associated with the Pasadena Independent School District are not an authority

Definition of Officers Definition of Committees Executive Committee Financial Checklist The Internal Auditors and individuals associated with the Pasadena Independent School District are not an authority

STATE OF NORTH CAROLINA OFFICE OF THE STATE AUDITOR BETH A. WOOD, CPA

CurrituckCurrituck STATE OF NORTH CAROLINA OFFICE OF THE STATE AUDITOR BETH A. WOOD, CPA CURRITUCK COUNTY CLERK OF SUPERIOR COURT CURRITUCK, NORTH CAROLINA FINANCIAL RELATED AUDIT JUNE 2018 STATE OF NORTH

CurrituckCurrituck STATE OF NORTH CAROLINA OFFICE OF THE STATE AUDITOR BETH A. WOOD, CPA CURRITUCK COUNTY CLERK OF SUPERIOR COURT CURRITUCK, NORTH CAROLINA FINANCIAL RELATED AUDIT JUNE 2018 STATE OF NORTH

STATE OF NORTH CAROLINA

STATE OF NORTH CAROLINA BURKE COUNTY CLERK OF SUPERIOR COURT FINANCIAL RELATED AUDIT APRIL 2013 OFFICE OF THE STATE AUDITOR BETH A. WOOD, CPA STATE AUDITOR BURKE COUNTY CLERK OF SUPERIOR COURT MORGANTON,

STATE OF NORTH CAROLINA BURKE COUNTY CLERK OF SUPERIOR COURT FINANCIAL RELATED AUDIT APRIL 2013 OFFICE OF THE STATE AUDITOR BETH A. WOOD, CPA STATE AUDITOR BURKE COUNTY CLERK OF SUPERIOR COURT MORGANTON,

Administrative Guidelines for the Establishment and Operation of University of California Foreign Affiliate Organizations

Administrative Guidelines for the Establishment and Operation of University of California Foreign Affiliate Organizations August 15, 2005 I. Policy A University of California Foreign Affiliate is a University-sanctioned

Administrative Guidelines for the Establishment and Operation of University of California Foreign Affiliate Organizations August 15, 2005 I. Policy A University of California Foreign Affiliate is a University-sanctioned

External Audit Report. The University of Texas at Austin s Center for Transportation Research TxDOT Compliance Division

External Audit Report The University of Texas at Austin s Center for Transportation Research TxDOT Compliance Division Objective and Scope To determine whether costs reimbursed for selected TxDOT research

External Audit Report The University of Texas at Austin s Center for Transportation Research TxDOT Compliance Division Objective and Scope To determine whether costs reimbursed for selected TxDOT research

STATE OF NORTH CAROLINA OFFICE OF THE STATE AUDITOR BETH A. WOOD, CPA

STATE OF NORTH CAROLINA OFFICE OF THE STATE AUDITOR BETH A. WOOD, CPA TRANSYLVANIA COUNTY CLERK OF SUPERIOR COURT BREVARD, NORTH CAROLINA FINANCIAL RELATED AUDIT JUNE 2018 STATE OF NORTH CAROLINA Office

STATE OF NORTH CAROLINA OFFICE OF THE STATE AUDITOR BETH A. WOOD, CPA TRANSYLVANIA COUNTY CLERK OF SUPERIOR COURT BREVARD, NORTH CAROLINA FINANCIAL RELATED AUDIT JUNE 2018 STATE OF NORTH CAROLINA Office

STATE OF NORTH CAROLINA OFFICE OF THE STATE AUDITOR BETH A. WOOD, CPA

STATE OF NORTH CAROLINA OFFICE OF THE STATE AUDITOR BETH A. WOOD, CPA PERSON COUNTY CLERK OF SUPERIOR COURT ROXBORO, NORTH CAROLINA FINANCIAL RELATED AUDIT JUNE 2017 STATE OF NORTH CAROLINA Office of the

STATE OF NORTH CAROLINA OFFICE OF THE STATE AUDITOR BETH A. WOOD, CPA PERSON COUNTY CLERK OF SUPERIOR COURT ROXBORO, NORTH CAROLINA FINANCIAL RELATED AUDIT JUNE 2017 STATE OF NORTH CAROLINA Office of the

R565, Audit Committees 1

R565, Audit Committees 1 R565-1. Purpose: To provide for the functions and responsibilities of Audit Committees within the Utah System of Higher Education (System). R565-2. References 2.1. Utah Code 53B-6-102

R565, Audit Committees 1 R565-1. Purpose: To provide for the functions and responsibilities of Audit Committees within the Utah System of Higher Education (System). R565-2. References 2.1. Utah Code 53B-6-102

August 16, 2007 FS 07-06

STATE OF CALIFORNIA DIANE WOODRUFF, CHANCELLOR (INTERIM) CALIFORNIA COMMUNITY COLLEGES SYSTEM OFFICE 1102 Q STREET SACRAMENTO, CA 95814-6511 (916) 445-8752 HTTP://WWW.CCCCO.EDU August 16, 2007 FS 07-06

STATE OF CALIFORNIA DIANE WOODRUFF, CHANCELLOR (INTERIM) CALIFORNIA COMMUNITY COLLEGES SYSTEM OFFICE 1102 Q STREET SACRAMENTO, CA 95814-6511 (916) 445-8752 HTTP://WWW.CCCCO.EDU August 16, 2007 FS 07-06

Maryland Department of Planning

Audit Report Maryland Department of Planning April 2017 OFFICE OF LEGISLATIVE AUDITS DEPARTMENT OF LEGISLATIVE SERVICES MARYLAND GENERAL ASSEMBLY For further information concerning this report contact:

Audit Report Maryland Department of Planning April 2017 OFFICE OF LEGISLATIVE AUDITS DEPARTMENT OF LEGISLATIVE SERVICES MARYLAND GENERAL ASSEMBLY For further information concerning this report contact:

Office of the Clerk of Circuit Court Baltimore County, Maryland

Audit Report Office of the Clerk of Circuit Court Baltimore County, Maryland May 2008 OFFICE OF LEGISLATIVE AUDITS DEPARTMENT OF LEGISLATIVE SERVICES MARYLAND GENERAL ASSEMBLY This report and any related

Audit Report Office of the Clerk of Circuit Court Baltimore County, Maryland May 2008 OFFICE OF LEGISLATIVE AUDITS DEPARTMENT OF LEGISLATIVE SERVICES MARYLAND GENERAL ASSEMBLY This report and any related

Office of the Register of Wills Frederick County, Maryland

Audit Report Office of the Register of Wills Frederick County, Maryland October 2010 OFFICE OF LEGISLATIVE AUDITS DEPARTMENT OF LEGISLATIVE SERVICES MARYLAND GENERAL ASSEMBLY This report and any related

Audit Report Office of the Register of Wills Frederick County, Maryland October 2010 OFFICE OF LEGISLATIVE AUDITS DEPARTMENT OF LEGISLATIVE SERVICES MARYLAND GENERAL ASSEMBLY This report and any related

STATE OF NORTH CAROLINA

STATE OF NORTH CAROLINA FORSYTH COUNTY CLERK OF SUPERIOR COURT WINSTON-SALEM, NORTH CAROLINA FINANCIAL RELATED AUDIT SEPTEMBER 2014 OFFICE OF THE STATE AUDITOR BETH A. WOOD, CPA STATE AUDITOR STATE OF

STATE OF NORTH CAROLINA FORSYTH COUNTY CLERK OF SUPERIOR COURT WINSTON-SALEM, NORTH CAROLINA FINANCIAL RELATED AUDIT SEPTEMBER 2014 OFFICE OF THE STATE AUDITOR BETH A. WOOD, CPA STATE AUDITOR STATE OF

Office of the Clerk of Circuit Court Baltimore County, Maryland

Audit Report Office of the Clerk of Circuit Court Baltimore County, Maryland October 2011 OFFICE OF LEGISLATIVE AUDITS DEPARTMENT OF LEGISLATIVE SERVICES MARYLAND GENERAL ASSEMBLY This report and any related

Audit Report Office of the Clerk of Circuit Court Baltimore County, Maryland October 2011 OFFICE OF LEGISLATIVE AUDITS DEPARTMENT OF LEGISLATIVE SERVICES MARYLAND GENERAL ASSEMBLY This report and any related

MERCER AREA SCHOOL DISTRICT

No. 626 MERCER AREA SCHOOL DISTRICT SECTION: TITLE: ADOPTED: REVISED: FINANCES FEDERAL FISCAL COMPLIANCE 626. FEDERAL FISCAL COMPLIANCE 1. Authority Part 200 The Board shall ensure federal funds received

No. 626 MERCER AREA SCHOOL DISTRICT SECTION: TITLE: ADOPTED: REVISED: FINANCES FEDERAL FISCAL COMPLIANCE 626. FEDERAL FISCAL COMPLIANCE 1. Authority Part 200 The Board shall ensure federal funds received

Corrective Action Plans Drafting 101. Intro. Agenda

Corrective Action Plans Drafting 101 Bonnie Little Graham, Esq. bgraham@bruman.com Jenny Segal, Esq. jsegal@bruman.com Fall Forum 2013 Intro [N]ewly purchased items of equipment were not consistently entered

Corrective Action Plans Drafting 101 Bonnie Little Graham, Esq. bgraham@bruman.com Jenny Segal, Esq. jsegal@bruman.com Fall Forum 2013 Intro [N]ewly purchased items of equipment were not consistently entered

TEXAS MEDICAL BOARD Austin, Texas ANNUAL INTERNAL AUDIT REPORT. Fiscal Year 2017

Austin, Texas ANNUAL INTERNAL AUDIT REPORT Austin, Texas TABLE OF CONTENTS Page Internal Auditor s... 1 Introduction... 2 Internal Audit Objectives.... 3 I. Compliance with Texas Government Code 2102:

Austin, Texas ANNUAL INTERNAL AUDIT REPORT Austin, Texas TABLE OF CONTENTS Page Internal Auditor s... 1 Introduction... 2 Internal Audit Objectives.... 3 I. Compliance with Texas Government Code 2102:

Tennessee Association of Alcohol, Drug & other Addiction Services

Tennessee Association of Alcohol, Drug & other Addiction Services ARTICLE I By-Laws As amended August 9, 2012 SECTION 1. Name The name of the organization shall be presently known as the Tennessee Association

Tennessee Association of Alcohol, Drug & other Addiction Services ARTICLE I By-Laws As amended August 9, 2012 SECTION 1. Name The name of the organization shall be presently known as the Tennessee Association

AMENDED BYLAWS OF THE SOUTH CAROLINA BLUEGRASS AND TRADITIONAL MUSIC ASSOCIATION

AMENDED BYLAWS OF THE SOUTH CAROLINA BLUEGRASS AND TRADITIONAL MUSIC ASSOCIATION ARTICLE I Name The name of the organization shall be THE SOUTH CAROLINA BLUEGRASS AND TRADITIONAL MUSIC ASSOCIATION herein

AMENDED BYLAWS OF THE SOUTH CAROLINA BLUEGRASS AND TRADITIONAL MUSIC ASSOCIATION ARTICLE I Name The name of the organization shall be THE SOUTH CAROLINA BLUEGRASS AND TRADITIONAL MUSIC ASSOCIATION herein

RALPH LAUREN CORPORATION CORPORATE GOVERNANCE POLICIES OF THE BOARD OF DIRECTORS. (As Amended as of February 7, 2018)

") RALPH LAUREN CORPORATION CORPORATE GOVERNANCE POLICIES OF THE BOARD OF DIRECTORS (As Amended as of February 7, 2018) The following principles have been approved by the Board of Directors of Ralph Lauren

RALPH LAUREN CORPORATION CORPORATE GOVERNANCE POLICIES OF THE BOARD OF DIRECTORS (As Amended as of February 7, 2018) The following principles have been approved by the Board of Directors of Ralph Lauren

CHAPTER House Bill No. 1123

CHAPTER 2006-146 House Bill No. 1123 An act relating to government accountability; creating s. 11.901, F.S., the Florida Government Accountability Act; creating s. 11.902, F.S.; providing definitions;

CHAPTER 2006-146 House Bill No. 1123 An act relating to government accountability; creating s. 11.901, F.S., the Florida Government Accountability Act; creating s. 11.902, F.S.; providing definitions;

AMENDED AND RESTATED BYLAWS THE HOPE FOUNDATION. Incorporated under the Texas Non-Profit Corporation Act ARTICLE I.

AMENDED AND RESTATED BYLAWS OF THE HOPE FOUNDATION Incorporated under the Texas Non-Profit Corporation Act ARTICLE I Name and Location Section 1. Name. The name of this Corporation is The Hope Foundation.

AMENDED AND RESTATED BYLAWS OF THE HOPE FOUNDATION Incorporated under the Texas Non-Profit Corporation Act ARTICLE I Name and Location Section 1. Name. The name of this Corporation is The Hope Foundation.

STATE OF NORTH CAROLINA OFFICE OF THE STATE AUDITOR BETH A. WOOD, CPA ROCKINGHAM COUNTY CLERK OF SUPERIOR COURT

STATE OF NORTH CAROLINA OFFICE OF THE STATE AUDITOR BETH A. WOOD, CPA ROCKINGHAM COUNTY CLERK OF SUPERIOR COURT WENTWORTH, NORTH CAROLINA FINANCIAL RELATED AUDIT JUNE 2018 STATE OF NORTH CAROLINA Office

STATE OF NORTH CAROLINA OFFICE OF THE STATE AUDITOR BETH A. WOOD, CPA ROCKINGHAM COUNTY CLERK OF SUPERIOR COURT WENTWORTH, NORTH CAROLINA FINANCIAL RELATED AUDIT JUNE 2018 STATE OF NORTH CAROLINA Office

STATE OF NEW YORK OFFICE OF THE STATE COMPTROLLER 110 STATE STREET ALBANY, NEW YORK 12236

THOMAS P. DiNAPOLI COMPTROLLER STATE OF NEW YORK OFFICE OF THE STATE COMPTROLLER 110 STATE STREET ALBANY, NEW YORK 12236 GABRIEL F. DEYO DEPUTY COMPTROLLER DIVISION OF LOCAL GOVERNMENT AND SCHOOL ACCOUNTABILITY

THOMAS P. DiNAPOLI COMPTROLLER STATE OF NEW YORK OFFICE OF THE STATE COMPTROLLER 110 STATE STREET ALBANY, NEW YORK 12236 GABRIEL F. DEYO DEPUTY COMPTROLLER DIVISION OF LOCAL GOVERNMENT AND SCHOOL ACCOUNTABILITY

STATE OF NORTH CAROLINA OFFICE OF THE STATE AUDITOR BETH A. WOOD, CPA

STATE OF NORTH CAROLINA OFFICE OF THE STATE AUDITOR BETH A. WOOD, CPA JACKSON COUNTY CLERK OF SUPERIOR COURT SYLVA, NORTH CAROLINA FINANCIAL RELATED AUDIT JUNE 2018 STATE OF NORTH CAROLINA Office of the

STATE OF NORTH CAROLINA OFFICE OF THE STATE AUDITOR BETH A. WOOD, CPA JACKSON COUNTY CLERK OF SUPERIOR COURT SYLVA, NORTH CAROLINA FINANCIAL RELATED AUDIT JUNE 2018 STATE OF NORTH CAROLINA Office of the

Bylaws of The Tall Bearded Iris Society

Bylaws of The Tall Bearded Iris Society Approved by the Membership 6/1/2016 Article I - Name BYLAWS The name of this, not for profit, organization shall be THE TALL BEARDED IRIS SOCIETY, hereinafter referred

Bylaws of The Tall Bearded Iris Society Approved by the Membership 6/1/2016 Article I - Name BYLAWS The name of this, not for profit, organization shall be THE TALL BEARDED IRIS SOCIETY, hereinafter referred

GRS : Accounting Records

Issued to: All Agencies GRS-1000.1002: Accounting Records Last Revised: 1/26/2011 Vermont State Archives and Records Administration Vermont Office of the Secretary of State www.vermont-archives.org/records/schedules

Issued to: All Agencies GRS-1000.1002: Accounting Records Last Revised: 1/26/2011 Vermont State Archives and Records Administration Vermont Office of the Secretary of State www.vermont-archives.org/records/schedules

STATE OF NORTH CAROLINA OFFICE OF THE STATE AUDITOR BETH A. WOOD, CPA FORSYTH COUNTY CLERK OF SUPERIOR COURT

STATE OF NORTH CAROLINA OFFICE OF THE STATE AUDITOR BETH A. WOOD, CPA FORSYTH COUNTY CLERK OF SUPERIOR COURT WINSTON-SALEM, NORTH CAROLINA FINANCIAL RELATED AUDIT JUNE 2018 STATE OF NORTH CAROLINA Office

STATE OF NORTH CAROLINA OFFICE OF THE STATE AUDITOR BETH A. WOOD, CPA FORSYTH COUNTY CLERK OF SUPERIOR COURT WINSTON-SALEM, NORTH CAROLINA FINANCIAL RELATED AUDIT JUNE 2018 STATE OF NORTH CAROLINA Office

STATE OF NORTH CAROLINA OFFICE OF THE STATE AUDITOR BETH A. WOOD, CPA

STATE OF NORTH CAROLINA OFFICE OF THE STATE AUDITOR BETH A. WOOD, CPA BURKE COUNTY CLERK OF SUPERIOR COURT MORGANTON, NORTH CAROLINA FINANCIAL RELATED AUDIT JUNE 2017 STATE OF NORTH CAROLINA Office of

STATE OF NORTH CAROLINA OFFICE OF THE STATE AUDITOR BETH A. WOOD, CPA BURKE COUNTY CLERK OF SUPERIOR COURT MORGANTON, NORTH CAROLINA FINANCIAL RELATED AUDIT JUNE 2017 STATE OF NORTH CAROLINA Office of

Bylaws Template. Part one: Mandatory Inclusions for Compliance with YWCA USA. Part two: Guide for YWCA Local Association Bylaws

Bylaws Template Part one: Mandatory Inclusions for Compliance with YWCA USA Part two: Guide for YWCA Local Association Bylaws These guidelines are provided solely as a resource to local associations. Each

Bylaws Template Part one: Mandatory Inclusions for Compliance with YWCA USA Part two: Guide for YWCA Local Association Bylaws These guidelines are provided solely as a resource to local associations. Each

THE GLOBAL FUND TO FIGHT AIDS, TUBERCULOSIS & MALARIA BY LAWS

THE GLOBAL FUND TO FIGHT AIDS, TUBERCULOSIS & MALARIA BY LAWS As Amended 21 November 2014 Article 1. Structure (the Global Fund ) is a multistakeholder international financing institution duly formed as

THE GLOBAL FUND TO FIGHT AIDS, TUBERCULOSIS & MALARIA BY LAWS As Amended 21 November 2014 Article 1. Structure (the Global Fund ) is a multistakeholder international financing institution duly formed as

SAMUEL H. COOPER CLERK OF THE CIRCUIT COURT FOR THE COUNTY OF ACCOMACK

SAMUEL H. COOPER CLERK OF THE CIRCUIT COURT FOR THE COUNTY OF ACCOMACK FOR THE PERIOD JANUARY 1, 2017 THROUGH JUNE 30, 2018 Auditor of Public Accounts Martha S. Mavredes, CPA www.apa.virginia.gov (804)

SAMUEL H. COOPER CLERK OF THE CIRCUIT COURT FOR THE COUNTY OF ACCOMACK FOR THE PERIOD JANUARY 1, 2017 THROUGH JUNE 30, 2018 Auditor of Public Accounts Martha S. Mavredes, CPA www.apa.virginia.gov (804)

Office of the Clerk of Circuit Court Garrett County, Maryland

Audit Report Office of the Clerk of Circuit Court Garrett County, Maryland June 2010 OFFICE OF LEGISLATIVE AUDITS DEPARTMENT OF LEGISLATIVE SERVICES MARYLAND GENERAL ASSEMBLY This report and any related

Audit Report Office of the Clerk of Circuit Court Garrett County, Maryland June 2010 OFFICE OF LEGISLATIVE AUDITS DEPARTMENT OF LEGISLATIVE SERVICES MARYLAND GENERAL ASSEMBLY This report and any related

REPORTING BY PUBLIC ENTITIES ACT 93 OF 1992 (Prior to repeal by Act 1 of 1999)

") REPORTING BY PUBLIC ENTITIES ACT 93 OF 1992 (Prior to repeal by Act 1 of 1999) [ASSENTED TO 18 JUNE 1992] [DATE OF COMMENCEMENT: 1 AUGUST 1992] (Afrikaans text signed by the State President) as amended

REPORTING BY PUBLIC ENTITIES ACT 93 OF 1992 (Prior to repeal by Act 1 of 1999) [ASSENTED TO 18 JUNE 1992] [DATE OF COMMENCEMENT: 1 AUGUST 1992] (Afrikaans text signed by the State President) as amended

Office of Administrative Hearings

Audit Report Office of Administrative Hearings March 2006 OFFICE OF LEGISLATIVE AUDITS DEPARTMENT OF LEGISLATIVE SERVICES MARYLAND GENERAL ASSEMBLY This report and any related follow-up correspondence

Audit Report Office of Administrative Hearings March 2006 OFFICE OF LEGISLATIVE AUDITS DEPARTMENT OF LEGISLATIVE SERVICES MARYLAND GENERAL ASSEMBLY This report and any related follow-up correspondence

STATE OF NORTH CAROLINA

STATE OF NORTH CAROLINA ONSLOW COUNTY CLERK OF SUPERIOR COURT JACKSONVILLE, NORTH CAROLINA FINANCIAL RELATED AUDIT NOVEMBER 2014 OFFICE OF THE STATE AUDITOR BETH A. WOOD, CPA STATE AUDITOR STATE OF NORTH

STATE OF NORTH CAROLINA ONSLOW COUNTY CLERK OF SUPERIOR COURT JACKSONVILLE, NORTH CAROLINA FINANCIAL RELATED AUDIT NOVEMBER 2014 OFFICE OF THE STATE AUDITOR BETH A. WOOD, CPA STATE AUDITOR STATE OF NORTH

Bylaws of the Young Women s Christian Association of the United States of America, Inc.

Bylaws of the Young Women s Christian Association of the United States of America, Inc. Effective on June 15, 2002; as amended April 29, 2006; as amended May 3, 2009; as amended April 8, 2011; as amended

Bylaws of the Young Women s Christian Association of the United States of America, Inc. Effective on June 15, 2002; as amended April 29, 2006; as amended May 3, 2009; as amended April 8, 2011; as amended

Office of the Clerk of Circuit Court Charles County, Maryland

Audit Report Office of the Clerk of Circuit Court Charles County, Maryland December 2009 OFFICE OF LEGISLATIVE AUDITS DEPARTMENT OF LEGISLATIVE SERVICES MARYLAND GENERAL ASSEMBLY This report and any related

Audit Report Office of the Clerk of Circuit Court Charles County, Maryland December 2009 OFFICE OF LEGISLATIVE AUDITS DEPARTMENT OF LEGISLATIVE SERVICES MARYLAND GENERAL ASSEMBLY This report and any related

CHARLES L. FRALEY, III CLERK OF THE CIRCUIT COURT OF THE COUNTY OF GILES REPORT ON AUDIT

CHARLES L. FRALEY, III CLERK OF THE CIRCUIT COURT OF THE COUNTY OF GILES REPORT ON AUDIT FOR THE PERIOD OCTOBER 1, 2008 THROUGH DECEMBER 31, 2009 T A B L E O F C O N T E N T S Pages AUDIT LETTER 1 COMMENTS

CHARLES L. FRALEY, III CLERK OF THE CIRCUIT COURT OF THE COUNTY OF GILES REPORT ON AUDIT FOR THE PERIOD OCTOBER 1, 2008 THROUGH DECEMBER 31, 2009 T A B L E O F C O N T E N T S Pages AUDIT LETTER 1 COMMENTS

STATE OF NORTH CAROLINA OFFICE OF THE STATE AUDITOR BETH A. WOOD, CPA WARREN COUNTY CLERK OF SUPERIOR COURT

STATE OF NORTH CAROLINA OFFICE OF THE STATE AUDITOR BETH A. WOOD, CPA WARREN COUNTY CLERK OF SUPERIOR COURT WARRENTON, NORTH CAROLINA FINANCIAL RELATED AUDIT JUNE 2018 STATE OF NORTH CAROLINA Office of

STATE OF NORTH CAROLINA OFFICE OF THE STATE AUDITOR BETH A. WOOD, CPA WARREN COUNTY CLERK OF SUPERIOR COURT WARRENTON, NORTH CAROLINA FINANCIAL RELATED AUDIT JUNE 2018 STATE OF NORTH CAROLINA Office of

Office of the Register of Wills Carroll County, Maryland

Audit Report Office of the Register of Wills Carroll County, Maryland May 2018 OFFICE OF LEGISLATIVE AUDITS DEPARTMENT OF LEGISLATIVE SERVICES MARYLAND GENERAL ASSEMBLY For further information concerning

Audit Report Office of the Register of Wills Carroll County, Maryland May 2018 OFFICE OF LEGISLATIVE AUDITS DEPARTMENT OF LEGISLATIVE SERVICES MARYLAND GENERAL ASSEMBLY For further information concerning

PARENTS, TEACHERS, AND STUDENTS (PTSA) COUNCIL OF BLOOMINGTON BYLAWS Adopted November 6, 2013 ARTICLE I - NAME

COUNCIL OF BLOOMINGTON BYLAWS Adopted November 6, 2013 ARTICLE I - NAME") PARENTS, TEACHERS, AND STUDENTS (PTSA) COUNCIL OF BLOOMINGTON BYLAWS Adopted November 6, 2013 ARTICLE I - NAME The name of this organization is the Parents, Teachers, and Students (PTSA) Council of Bloomington,

PARENTS, TEACHERS, AND STUDENTS (PTSA) COUNCIL OF BLOOMINGTON BYLAWS Adopted November 6, 2013 ARTICLE I - NAME The name of this organization is the Parents, Teachers, and Students (PTSA) Council of Bloomington,

Department of Health and Mental Hygiene Laboratories Administration

Audit Report Department of Health and Mental Hygiene Laboratories Administration March 2016 OFFICE OF LEGISLATIVE AUDITS DEPARTMENT OF LEGISLATIVE SERVICES MARYLAND GENERAL ASSEMBLY For further information

Audit Report Department of Health and Mental Hygiene Laboratories Administration March 2016 OFFICE OF LEGISLATIVE AUDITS DEPARTMENT OF LEGISLATIVE SERVICES MARYLAND GENERAL ASSEMBLY For further information

STATE OF NORTH CAROLINA

STATE OF NORTH CAROLINA ALEXANDER COUNTY CLERK OF SUPERIOR COURT TAYLORSVILLE, NORTH CAROLINA FINANCIAL RELATED AUDIT SEPTEMBER 2014 OFFICE OF THE STATE AUDITOR BETH A. WOOD, CPA STATE AUDITOR STATE OF

STATE OF NORTH CAROLINA ALEXANDER COUNTY CLERK OF SUPERIOR COURT TAYLORSVILLE, NORTH CAROLINA FINANCIAL RELATED AUDIT SEPTEMBER 2014 OFFICE OF THE STATE AUDITOR BETH A. WOOD, CPA STATE AUDITOR STATE OF

STATE OF NORTH CAROLINA OFFICE OF THE STATE AUDITOR BETH A. WOOD, CPA ANSON COUNTY CLERK OF SUPERIOR COURT

STATE OF NORTH CAROLINA OFFICE OF THE STATE AUDITOR BETH A. WOOD, CPA ANSON COUNTY CLERK OF SUPERIOR COURT WADESBORO, NORTH CAROLINA FINANCIAL RELATED AUDIT JULY 2018 STATE OF NORTH CAROLINA Office of

STATE OF NORTH CAROLINA OFFICE OF THE STATE AUDITOR BETH A. WOOD, CPA ANSON COUNTY CLERK OF SUPERIOR COURT WADESBORO, NORTH CAROLINA FINANCIAL RELATED AUDIT JULY 2018 STATE OF NORTH CAROLINA Office of

STATE OF NORTH CAROLINA OFFICE OF THE STATE AUDITOR BETH A. WOOD, CPA STANLY COUNTY CLERK OF SUPERIOR COURT

STATE OF NORTH CAROLINA OFFICE OF THE STATE AUDITOR BETH A. WOOD, CPA STANLY COUNTY CLERK OF SUPERIOR COURT ALBEMARLE, NORTH CAROLINA FINANCIAL RELATED AUDIT JUNE 2018 STATE OF NORTH CAROLINA Office of

STATE OF NORTH CAROLINA OFFICE OF THE STATE AUDITOR BETH A. WOOD, CPA STANLY COUNTY CLERK OF SUPERIOR COURT ALBEMARLE, NORTH CAROLINA FINANCIAL RELATED AUDIT JUNE 2018 STATE OF NORTH CAROLINA Office of

889 (05/04) Auditor s Guide. Province of British Columbia

Auditor s Guide. Province of British Columbia") 889 (05/04) Auditor s Guide Province of British Columbia Table of Contents Preface 3 Introduction 4 Auditor Appointment 6 Audit Requirement 8 Relevant Dates 9 Terms of Engagement 12 Accounting and Reporting

889 (05/04) Auditor s Guide Province of British Columbia Table of Contents Preface 3 Introduction 4 Auditor Appointment 6 Audit Requirement 8 Relevant Dates 9 Terms of Engagement 12 Accounting and Reporting

DEPARTMENT OF THE NAVY

SECNAV INSTRUCTION 5730.13A From: Secretary of the Navy DEPARTMENT OF THE NAVY OFFICE OF THE SECRETARY 1000 NAVY PENTAGON WASHINGTON DC 20350-1000 SECNAVINST 5730.13A N2J Subj: CONGRESSIONAL NOTIFICATION

SECNAV INSTRUCTION 5730.13A From: Secretary of the Navy DEPARTMENT OF THE NAVY OFFICE OF THE SECRETARY 1000 NAVY PENTAGON WASHINGTON DC 20350-1000 SECNAVINST 5730.13A N2J Subj: CONGRESSIONAL NOTIFICATION

LA14-24 STATE OF NEVADA. Performance Audit. Department of Public Safety Office of Director Legislative Auditor Carson City, Nevada

LA14-24 STATE OF NEVADA Performance Audit Department of Public Safety Office of Director 2014 Legislative Auditor Carson City, Nevada leg Audit Highlights Highlights of performance audit report on the

LA14-24 STATE OF NEVADA Performance Audit Department of Public Safety Office of Director 2014 Legislative Auditor Carson City, Nevada leg Audit Highlights Highlights of performance audit report on the

CHAPTER Committee Substitute for Committee Substitute for Committee Substitute for House Bill No. 1279

CHAPTER 2018-5 Committee Substitute for Committee Substitute for Committee Substitute for House Bill No. 1279 An act relating to school district accountability; amending s. 11.45, F.S.; revising the duties

CHAPTER 2018-5 Committee Substitute for Committee Substitute for Committee Substitute for House Bill No. 1279 An act relating to school district accountability; amending s. 11.45, F.S.; revising the duties

LACERA LEGISLATIVE POLICY

LACERA LEGISLATIVE POLICY Restated Board of Retirement: October 13, 2016 and Approved: Board of Investments: October 12, 2016 Table of Contents Statement of Mission and Purpose... 3 Legislative Policy

LACERA LEGISLATIVE POLICY Restated Board of Retirement: October 13, 2016 and Approved: Board of Investments: October 12, 2016 Table of Contents Statement of Mission and Purpose... 3 Legislative Policy

ON THE REGISTRATION AND OPERATION OF NON-GOVERNMENTAL ORGANIZATIONS IN KOSOVO. The Special Representative of the Secretary-General,

REGULATION NO. 1999/22 UNMIK/REG/1999/22 15 November 1999 ON THE REGISTRATION AND OPERATION OF NON-GOVERNMENTAL ORGANIZATIONS IN KOSOVO The Special Representative of the Secretary-General, Pursuant to

REGULATION NO. 1999/22 UNMIK/REG/1999/22 15 November 1999 ON THE REGISTRATION AND OPERATION OF NON-GOVERNMENTAL ORGANIZATIONS IN KOSOVO The Special Representative of the Secretary-General, Pursuant to

Property Tax Assessment Appeals Boards

Audit Report Property Tax Assessment Appeals Boards April 2007 OFFICE OF LEGISLATIVE AUDITS DEPARTMENT OF LEGISLATIVE SERVICES MARYLAND GENERAL ASSEMBLY This report and any related follow-up correspondence

Audit Report Property Tax Assessment Appeals Boards April 2007 OFFICE OF LEGISLATIVE AUDITS DEPARTMENT OF LEGISLATIVE SERVICES MARYLAND GENERAL ASSEMBLY This report and any related follow-up correspondence

Bylaws of the International E-learning Association (IELA)

") Bylaws of the International E-learning Association (IELA) Article 1 Nonprofit Purposes Section 1. Specific Objectives and Purposes The International E-learning Association (IELA) s purpose will be to promote

Bylaws of the International E-learning Association (IELA) Article 1 Nonprofit Purposes Section 1. Specific Objectives and Purposes The International E-learning Association (IELA) s purpose will be to promote

FLORIDA POLYTECHNIC UNIVERSITY BOARD OF TRUSTEES

FLORIDA POLYTECHNIC UNIVERSITY BOARD OF TRUSTEES AGENDA One Poly Place 439 South Florida Avenue Lakeland, Florida 33801 October 24, 2012 8:00 a.m. 1. Call to Order Chair Robert Gidel 2. Approval of Meeting

FLORIDA POLYTECHNIC UNIVERSITY BOARD OF TRUSTEES AGENDA One Poly Place 439 South Florida Avenue Lakeland, Florida 33801 October 24, 2012 8:00 a.m. 1. Call to Order Chair Robert Gidel 2. Approval of Meeting

STATE OF NORTH CAROLINA OFFICE OF THE STATE AUDITOR BETH A. WOOD, CPA

STATE OF NORTH CAROLINA OFFICE OF THE STATE AUDITOR BETH A. WOOD, CPA YANCEY COUNTY CLERK OF SUPERIOR COURT BURNSVILLE, NORTH CAROLINA FINANCIAL RELATED AUDIT SEPTEMBER 2015 STATE OF NORTH CAROLINA Office

STATE OF NORTH CAROLINA OFFICE OF THE STATE AUDITOR BETH A. WOOD, CPA YANCEY COUNTY CLERK OF SUPERIOR COURT BURNSVILLE, NORTH CAROLINA FINANCIAL RELATED AUDIT SEPTEMBER 2015 STATE OF NORTH CAROLINA Office

Office of Inspector General Florida Independent Living Council (FILC)

") Office of Inspector General Florida Independent Living Council (FILC) Report #A-1617-030 December 2017 Executive Summary In accordance with the Department of Education s fiscal year (FY) 2016-2017 audit

Office of Inspector General Florida Independent Living Council (FILC) Report #A-1617-030 December 2017 Executive Summary In accordance with the Department of Education s fiscal year (FY) 2016-2017 audit

INTERNAL AUDIT DIVISION REPORT 2018/003

INTERNAL AUDIT DIVISION REPORT 2018/003 Audit of the operations in the Republic of the Congo for the Office of the United Nations High Commissioner for Refugees There were critical deficiencies in controls

INTERNAL AUDIT DIVISION REPORT 2018/003 Audit of the operations in the Republic of the Congo for the Office of the United Nations High Commissioner for Refugees There were critical deficiencies in controls

BYLAWS NEW YORK EHEALTH COLLABORATIVE, INC. Amended and Restated as of September 28, 2017 ARTICLE 1 GENERAL

BYLAWS OF NEW YORK EHEALTH COLLABORATIVE, INC. Amended and Restated as of September 28, 2017 ARTICLE 1 GENERAL Section 1.1 Name. The name of the Corporation shall be New York ehealth Collaborative, Inc.

BYLAWS OF NEW YORK EHEALTH COLLABORATIVE, INC. Amended and Restated as of September 28, 2017 ARTICLE 1 GENERAL Section 1.1 Name. The name of the Corporation shall be New York ehealth Collaborative, Inc.

NARUC CONSTITUTION (As amended November 14, 2018) ARTICLE I - NAME AND DEFINITIONS

ARTICLE I - NAME AND DEFINITIONS") NARUC CONSTITUTION (As amended November 14, 2018) ARTICLE I - NAME AND DEFINITIONS Section 1. The name of this Association shall be the "National Association of Regulatory Utility Commissioners. Section

NARUC CONSTITUTION (As amended November 14, 2018) ARTICLE I - NAME AND DEFINITIONS Section 1. The name of this Association shall be the "National Association of Regulatory Utility Commissioners. Section

Independent Audit & Tax Services 15-NWA-004

Independent Audit & Tax Services 15-NWA-004 Posting Date: 2/06/2015 Proposal submission deadline: 3/6/2015 8:00 PM EST Purpose of the RFP Neighborhood Reinvestment Corporation d/b/a NeighborWorks America

Independent Audit & Tax Services 15-NWA-004 Posting Date: 2/06/2015 Proposal submission deadline: 3/6/2015 8:00 PM EST Purpose of the RFP Neighborhood Reinvestment Corporation d/b/a NeighborWorks America

LIMITED-SCOPE PERFORMANCE AUDIT REPORT

LIMITED-SCOPE PERFORMANCE AUDIT REPORT Lobbying Services: Evaluating a Small Sample of Local Governments Reported Payments to Lobbyists and Associations with Lobbyists AUDIT ABSTRACT Local governments

LIMITED-SCOPE PERFORMANCE AUDIT REPORT Lobbying Services: Evaluating a Small Sample of Local Governments Reported Payments to Lobbyists and Associations with Lobbyists AUDIT ABSTRACT Local governments

STATE OF NORTH CAROLINA

STATE OF NORTH CAROLINA NORTHAMPTON COUNTY CLERK OF SUPERIOR COURT FINANCIAL RELATED AUDIT JUNE 2013 OFFICE OF THE STATE AUDITOR BETH A. WOOD, CPA STATE AUDITOR NORTHAMPTON COUNTY CLERK OF SUPERIOR COURT

STATE OF NORTH CAROLINA NORTHAMPTON COUNTY CLERK OF SUPERIOR COURT FINANCIAL RELATED AUDIT JUNE 2013 OFFICE OF THE STATE AUDITOR BETH A. WOOD, CPA STATE AUDITOR NORTHAMPTON COUNTY CLERK OF SUPERIOR COURT

STATE OF NORTH CAROLINA OFFICE OF THE STATE AUDITOR BETH A. WOOD, CPA

STATE OF NORTH CAROLINA OFFICE OF THE STATE AUDITOR BETH A. WOOD, CPA SWAIN COUNTY CLERK OF SUPERIOR COURT BRYSON CITY, NORTH CAROLINA FINANCIAL RELATED AUDIT OCTOBER 2015 STATE OF NORTH CAROLINA Office

STATE OF NORTH CAROLINA OFFICE OF THE STATE AUDITOR BETH A. WOOD, CPA SWAIN COUNTY CLERK OF SUPERIOR COURT BRYSON CITY, NORTH CAROLINA FINANCIAL RELATED AUDIT OCTOBER 2015 STATE OF NORTH CAROLINA Office

d. Pinellas County, Florida Annual Financial Report for the Fiscal Year Ended September 30, 2010.

AGENDA ITEM # 2 May 24,2011 2. REPORTS TO BE RECEIVED FOR FILING a., Clerk of the Circuit Court, Report No. 2011-03 dated April 6, 2011-2010 Annual Summary Report of Random Audits of the County's Annual

AGENDA ITEM # 2 May 24,2011 2. REPORTS TO BE RECEIVED FOR FILING a., Clerk of the Circuit Court, Report No. 2011-03 dated April 6, 2011-2010 Annual Summary Report of Random Audits of the County's Annual

REPORT 2015/111 INTERNAL AUDIT DIVISION. Audit of the operations in Algeria for the Office of the United Nations High Commissioner for Refugees

INTERNAL AUDIT DIVISION REPORT 2015/111 Audit of the operations in Algeria for the Office of the United Nations High Commissioner for Refugees Overall results relating to effective management of the operations

INTERNAL AUDIT DIVISION REPORT 2015/111 Audit of the operations in Algeria for the Office of the United Nations High Commissioner for Refugees Overall results relating to effective management of the operations

LLEZELLE DUGGER CLERK OF THE CIRCUIT COURT FOR THE CITY OF CHARLOTTESVILLE

LLEZELLE DUGGER CLERK OF THE CIRCUIT COURT FOR THE CITY OF CHARLOTTESVILLE FOR THE PERIOD APRIL 1, 2017 THROUGH MARCH 31, 2018 Auditor of Public Accounts Martha S. Mavredes, CPA www.apa.virginia.gov (804)

LLEZELLE DUGGER CLERK OF THE CIRCUIT COURT FOR THE CITY OF CHARLOTTESVILLE FOR THE PERIOD APRIL 1, 2017 THROUGH MARCH 31, 2018 Auditor of Public Accounts Martha S. Mavredes, CPA www.apa.virginia.gov (804)

DESERT VISTA HIGH SCHOOL THUNDER BOARD ASSOCIATION BYLAWS

DESERT VISTA HIGH SCHOOL THUNDER BOARD ASSOCIATION BYLAWS April 2014 BYLAWS OF DESERT VISTA HIGH SCHOOL THUNDER BOARD ASSOCIATION ARTICLE I NAME AND LOCATION Section 1 The official name of the association

DESERT VISTA HIGH SCHOOL THUNDER BOARD ASSOCIATION BYLAWS April 2014 BYLAWS OF DESERT VISTA HIGH SCHOOL THUNDER BOARD ASSOCIATION ARTICLE I NAME AND LOCATION Section 1 The official name of the association

Office of the Clerk of Circuit Court Dorchester County, Maryland

Audit Report Office of the Clerk of Circuit Court Dorchester County, Maryland July 2006 OFFICE OF LEGISLATIVE AUDITS DEPARTMENT OF LEGISLATIVE SERVICES MARYLAND GENERAL ASSEMBLY This report and any related

Audit Report Office of the Clerk of Circuit Court Dorchester County, Maryland July 2006 OFFICE OF LEGISLATIVE AUDITS DEPARTMENT OF LEGISLATIVE SERVICES MARYLAND GENERAL ASSEMBLY This report and any related

STATE OF NORTH CAROLINA OFFICE OF THE STATE AUDITOR BETH A. WOOD, CPA

STATE OF NORTH CAROLINA OFFICE OF THE STATE AUDITOR BETH A. WOOD, CPA PAMLICO COUNTY CLERK OF SUPERIOR COURT BAYBORO, NORTH CAROLINA FINANCIAL RELATED AUDIT JULY 2016 STATE OF NORTH CAROLINA Office of

STATE OF NORTH CAROLINA OFFICE OF THE STATE AUDITOR BETH A. WOOD, CPA PAMLICO COUNTY CLERK OF SUPERIOR COURT BAYBORO, NORTH CAROLINA FINANCIAL RELATED AUDIT JULY 2016 STATE OF NORTH CAROLINA Office of

RESTATED BYLAWS OF DRUPALCON, INC. (updated April 23, 2014)

") RESTATED BYLAWS OF DRUPALCON, INC. (updated April 23, 2014) MEMBERS DrupalCon, Inc. (the "Corporation") is a Washington, D.C. nonprofit, public benefit corporation, and it has no members. From time to

RESTATED BYLAWS OF DRUPALCON, INC. (updated April 23, 2014) MEMBERS DrupalCon, Inc. (the "Corporation") is a Washington, D.C. nonprofit, public benefit corporation, and it has no members. From time to

Audit Committee Guidelines

Ô«b ó a@äb rné @ flaç a@úä ãí Zamil Industrial Investment Co. Zamil Industrial Investment Co. (Zamil Industrial) Governance Charters Contents Introduction First : Audit Committee Duties and Responsibilities

Ô«b ó a@äb rné @ flaç a@úä ãí Zamil Industrial Investment Co. Zamil Industrial Investment Co. (Zamil Industrial) Governance Charters Contents Introduction First : Audit Committee Duties and Responsibilities

Burroughs Community School Parent Teacher Association BYLAWS adopted February 13, 2011 amended May 1, 2012 amended April 25, 2017

Burroughs Community School Parent Teacher Association BYLAWS adopted February 13, 2011 amended May 1, 2012 amended April 25, 2017 ARTICLE I -Name The name of this organization is the Burroughs Community

Burroughs Community School Parent Teacher Association BYLAWS adopted February 13, 2011 amended May 1, 2012 amended April 25, 2017 ARTICLE I -Name The name of this organization is the Burroughs Community

Office of the Clerk of Circuit Court Baltimore City, Maryland

Audit Report Office of the Clerk of Circuit Court Baltimore City, Maryland June 2011 OFFICE OF LEGISLATIVE AUDITS DEPARTMENT OF LEGISLATIVE SERVICES MARYLAND GENERAL ASSEMBLY This report and any related

Audit Report Office of the Clerk of Circuit Court Baltimore City, Maryland June 2011 OFFICE OF LEGISLATIVE AUDITS DEPARTMENT OF LEGISLATIVE SERVICES MARYLAND GENERAL ASSEMBLY This report and any related

STATE OF NORTH CAROLINA OFFICE OF THE STATE AUDITOR BETH A. WOOD, CPA

STATE OF NORTH CAROLINA OFFICE OF THE STATE AUDITOR BETH A. WOOD, CPA SURRY COUNTY CLERK OF SUPERIOR COURT DOBSON, NORTH CAROLINA FINANCIAL RELATED AUDIT JULY 2016 STATE OF NORTH CAROLINA Office of the

STATE OF NORTH CAROLINA OFFICE OF THE STATE AUDITOR BETH A. WOOD, CPA SURRY COUNTY CLERK OF SUPERIOR COURT DOBSON, NORTH CAROLINA FINANCIAL RELATED AUDIT JULY 2016 STATE OF NORTH CAROLINA Office of the

MS PTA LOCAL UNIT BYLAWS

MS PTA LOCAL UNIT BYLAWS ARTICLE I: NAME The name of this association is the (Name of Unit) Parent-Teacher Association (PTA/PTSA), whose address is (Mailing Address, City, State, Zip Code) It is a local

MS PTA LOCAL UNIT BYLAWS ARTICLE I: NAME The name of this association is the (Name of Unit) Parent-Teacher Association (PTA/PTSA), whose address is (Mailing Address, City, State, Zip Code) It is a local

AUDIT COMMITTEE CHARTER of the Audit Committee of New Oriental Education & Technology Group Inc.

AUDIT COMMITTEE CHARTER of the Audit Committee of New Oriental Education & Technology Group Inc. This Audit Committee Charter (the Audit Committee Charter ) was adopted by the Board of Directors (the Board

AUDIT COMMITTEE CHARTER of the Audit Committee of New Oriental Education & Technology Group Inc. This Audit Committee Charter (the Audit Committee Charter ) was adopted by the Board of Directors (the Board

BYLAWS NE 67 th Court, Suite B202, Redmond, WA

ADOPTION OF BYLAWS We, the undersigned, are all of the Directors or incorporators of this corporation, and we consent to, and hereby do, adopt the following bylaws, consisting of fourteen pages to follow,

ADOPTION OF BYLAWS We, the undersigned, are all of the Directors or incorporators of this corporation, and we consent to, and hereby do, adopt the following bylaws, consisting of fourteen pages to follow,

LOCAL UNIT BYLAWS REVISED AMENDED 2006

LOCAL UNIT BYLAWS REVISED 2001 - AMENDED 2006 Winnona Park Elementary School Name 510 Avery Street Street Address Decatur GA 30030 City State Zip Code DeKalb 11 1649 County PTA District Local Unit # Affirmation:

LOCAL UNIT BYLAWS REVISED 2001 - AMENDED 2006 Winnona Park Elementary School Name 510 Avery Street Street Address Decatur GA 30030 City State Zip Code DeKalb 11 1649 County PTA District Local Unit # Affirmation:

INTERNAL AUDIT DIVISION REPORT 2017/032. Audit of the human rights programme in the United Nations Stabilization Mission in Haiti

INTERNAL AUDIT DIVISION REPORT 2017/032 Audit of the human rights programme in the United Nations Stabilization Mission in Haiti The Mission developed and implemented a work plan for its human rights programme

INTERNAL AUDIT DIVISION REPORT 2017/032 Audit of the human rights programme in the United Nations Stabilization Mission in Haiti The Mission developed and implemented a work plan for its human rights programme

NeighborWorks America Strategic Plan

NeighborWorks America Strategic Plan 2012-2016 Now more than ever, NeighborWorks America and its network of NeighborWorks organizations across the country are needed to provide opportunities for people

NeighborWorks America Strategic Plan 2012-2016 Now more than ever, NeighborWorks America and its network of NeighborWorks organizations across the country are needed to provide opportunities for people

BOARD OF DIRECTORS BY-LAWS

SHASTA HEAD START CHILD DEVELOPMENT, INC. BOARD OF DIRECTORS BY-LAWS Article I Name The name of the Corporation is Shasta County Head Start Child Development, Inc. Article II Purpose Shasta Head Start

SHASTA HEAD START CHILD DEVELOPMENT, INC. BOARD OF DIRECTORS BY-LAWS Article I Name The name of the Corporation is Shasta County Head Start Child Development, Inc. Article II Purpose Shasta Head Start

The Bylaws of the Association for Talent Development South Florida Chapter

The Bylaws of the Association for Talent Development South Florida Chapter Table of Contents Table of Contents... 2 Article I. Name and Purpose... 4 Section A: Chapter Name... 4 Section B: Affiliation

The Bylaws of the Association for Talent Development South Florida Chapter Table of Contents Table of Contents... 2 Article I. Name and Purpose... 4 Section A: Chapter Name... 4 Section B: Affiliation

STATE OF NORTH CAROLINA

STATE OF NORTH CAROLINA HERTFORD COUNTY CLERK OF SUPERIOR COURT FISCAL CONTROL AUDIT WINTON, NORTH CAROLINA OFFICE OF THE STATE AUDITOR BETH A. WOOD, CPA STATE AUDITOR HERTFORD COUNTY CLERK OF SUPERIOR

STATE OF NORTH CAROLINA HERTFORD COUNTY CLERK OF SUPERIOR COURT FISCAL CONTROL AUDIT WINTON, NORTH CAROLINA OFFICE OF THE STATE AUDITOR BETH A. WOOD, CPA STATE AUDITOR HERTFORD COUNTY CLERK OF SUPERIOR

III. For which Fiscal Year (FY) is this recommendation being made: Estimated Start Date Estimated Completion Date

is this recommendation being made: Estimated Start Date Estimated Completion Date") 1 IPA Recommendation Form for Local Public Bodies Under the Tiered System (LPB) (Please Use your LPB s Letterhead when printing this recommendation) Complete the contract (including obtaining the IPA's

1 IPA Recommendation Form for Local Public Bodies Under the Tiered System (LPB) (Please Use your LPB s Letterhead when printing this recommendation) Complete the contract (including obtaining the IPA's